The clock never stops ticking on America’s national debt problem

The Congressional Budget Office warned that the US government could run out of money as early as May — and that’s just the short-term concern.

On Tuesday, the Congressional Budget Office warned that the US government could run out of money to pay its bills in August — or even earlier, in a worst-case scenario.

How did we get here?

When the debt ceiling kicked back in at the start of 2025, following the end of a 19-month suspension, it was reset at $36.1 trillion, the amount of debt outstanding at the time.

Since then, the Treasury began relying on temporary accounting maneuvers (known as “extraordinary measures”) to keep funding the government without breaching the cap. However, even those emergency tactics will run dry by the so-called “X-date” — a date that’s difficult to pin down exactly — which the CBO estimates will likely arrive in August or September, but could come as early as late May if tax revenues come in low or spending runs high.

Unless Congress raises or suspends the ceiling again, the US would start defaulting, missing payments on obligations like Social Security or military salaries.

Zooming out

Indeed, $36 trillion is a number that’s hard to conceptualize. Put another way, Uncle Sam owes about $106,000 for every single person in the United States. Even when compared to the size of the economy itself, the US national debt burden is looking heavy.

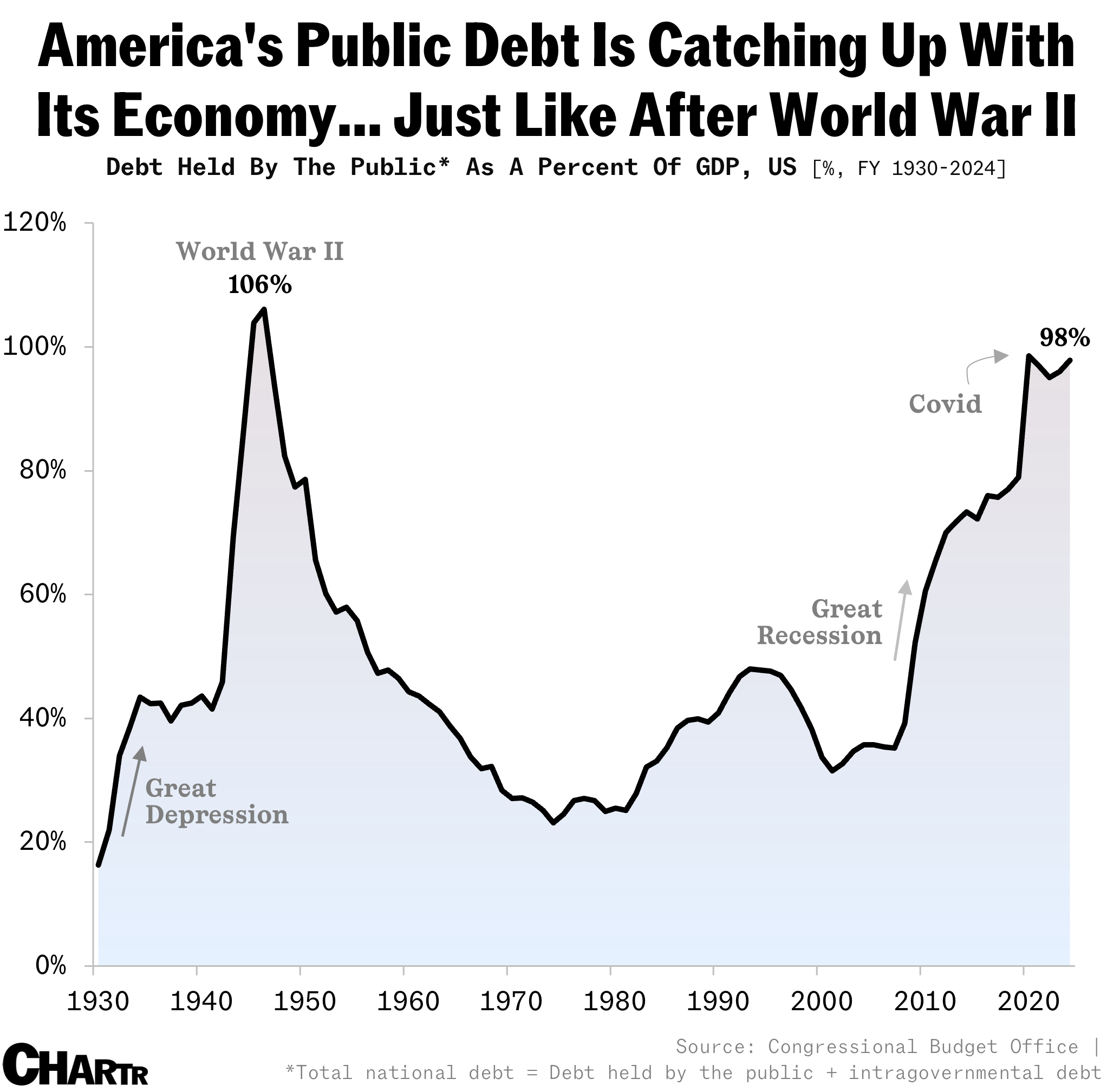

As of 2024, federal debt held by the public — about 80% of the total national debt, with the rest made up of money the government owes itself — stood at 98% of US GDP, per the CBO. The last time it came this close was just after World War II, when it peaked at 106%.

And it’s not slowing down. According to CBO’s January projection, the debt level is on track to surpass this WWII peak by 2029 and reach 119% of GDP by 2035, largely driven by ballooning interest payments and rising costs for Social Security and Medicare as the population ages.

With default risk looming and debt nearly matching the size of the economy, the fiscal fight is already underway. House Republicans want to raise the ceiling by $4 trillion through a budget bill that bypasses Democrats; Democrats say they’re open to negotiating — just not at the cost of major social programs.

In January, Treasury Secretary Scott Bessent, newly appointed under President Trump, said in his confirmation hearing that the US “is not going to default on its debt” under his watch.