UBS unpacks the most controversial slide from Nvidia CEO Jensen Huang’s GTC presentation

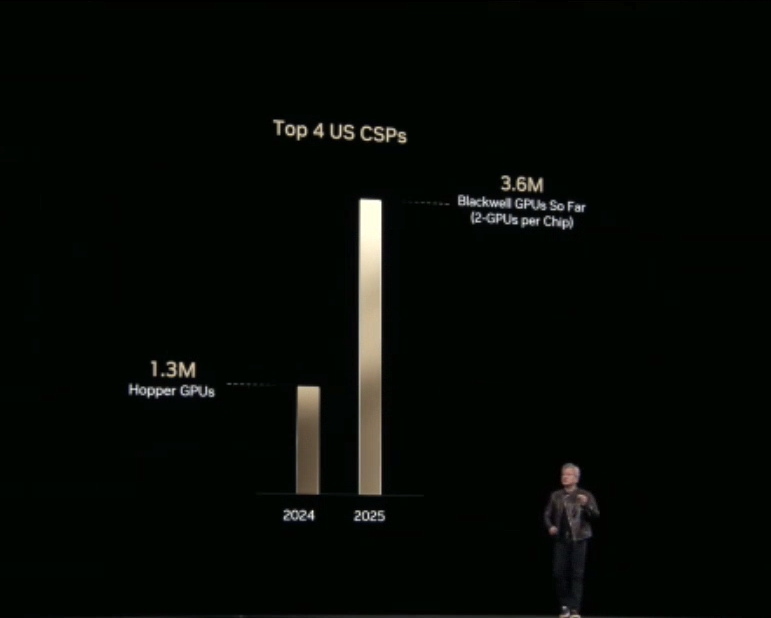

Nvidia CEO Jensen Huang didn’t move markets when he delivered his keynote address at the chip designer’s conference on Tuesday. But he did raise eyebrows, particularly with one slide that compared shipments of Nvidia’s old flagship chip (Hopper) to its Blackwell current ramp.

The chart illustrated that Blackwell demand this year from the top four cloud service providers (Microsoft, Alphabet, Amazon, and Oracle) has already far outstripped Hopper’s from last year, which was peak demand for that particular product.

“So you can kind of see that in fact AI is going through an inflection point,” Huang said in reference to the chart.

The CEO had specified that Hopper’s figures were 2024 shipments, but there was a lack of clarity on precisely what the 2025 Blackwell numbers meant.

UBS analysts led by Timothy Acuri got the lowdown on the matter.

“The slide generating the most controversy was a comparison of unit shipments to just the top 4 US CSPs for both Hopper and Blackwell, implying to us these customers were ~40% of total units last year,” he wrote in a note maintaining a buy rating and $185 price target on the stock. “In speaking to the company, the Blackwell number was meant to essentially represent shipments ‘in process’ — we think roughly equivalent to backlog and roughly looking out through CQ3 of this year.”

Putting this all together, Acuri has higher conviction in his call that the chip designer’s near-term earnings growth will be much more substantial than his peers anticipate.

“So assuming a similar mix and netting off the ~100k units that we think shipped to these customers in the month of January, this would imply total Blackwell units in the ~4.2 million range in the period from FQ1 (April) to FQ3 (Oct) of this year,” he continued. “While inexact math, this is nicely above our ~3.8 million model for Blackwell units over this period making us feel pretty good about our ~$5.30 EPS this year (Street still ~$4.50).”