There’s only one Wall Street analyst with a sell rating on Nvidia — what’s his thesis?

The poster child of the AI boom is nearing a $4 trillion market cap, and most Wall Street analysts still think there’s room for more upside. Except one.

As we’ve seen before, Wall Street analysts tend to move as a herd. Indeed, for all the constant bleating about contrarian thinking, many of the analysts at major banks and research houses tend to end up with the same conclusion about the megacap tech stocks they’re tasked with covering: that you should buy their stock.

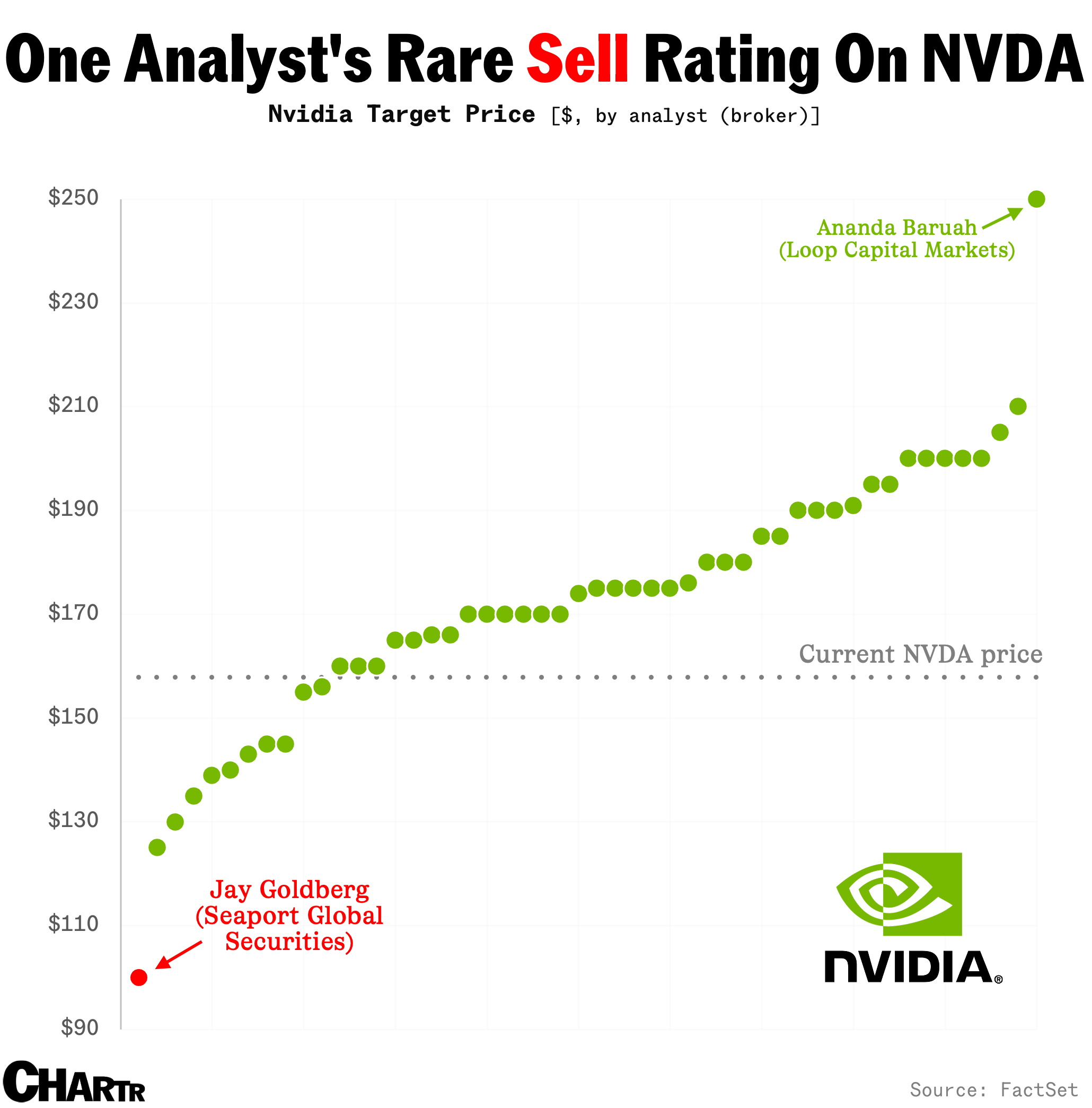

Nvidia’s coverage is no exception. According to FactSet, there’s just one analyst, Jay Goldberg of Seaport Global Securities, who is going against the grain, with an active “sell” (or equivalent) rating on the name.

Goldberg’s $100 target price on the stock market behemoth — implying 37% downside to yesterday’s close price — is predicated on a few key pillars. In a document shared with Sherwood News, Goldberg outlined the headlines of his bearish thesis:

“Nvidia is one of the leading beneficiaries of the current AI spending boom, but its prospects are well understood and largely priced into the stock.”

According to Goldberg, there are growing questions about the actual usefulness of AI, with many of Nvidia’s customers still looking for returns from their “significant investments” in AI so far. That’s likely to mean a slowing of AI budgets in 2026.

Goldberg also wrote:

“Our research indicates significant complexity required for deployments of Nvidia systems in comparison to traditional data centers — cooling, configuration and orchestration challenges throughout the supply chain.”

On top of potential supply chain issues, he also sees a chance that Nvidia’s near monopoly position in the industry could face competition in the medium term, as the company’s top customers, like Meta, Microsoft, and Amazon build on efforts to make their own chips:

“Strong momentum behind hyperscalers’ internal Nvidia alternatives — Nvidia’s largest customers are all looking to design their own chips.”

In the nearer term, cyclical issues, including production limitations for its much sought-after Blackwell line, could raise further concerns.

Of course, there are some major “risks” to the bearish case, too. Perhaps the most important of those noted by Goldberg is that some “unforeseen advances” in AI could suddenly lead to another surge in demand. That’s a possibility that Loop Capital analysts, who have the highest price target on the street ($250), clearly think is more likely than not.

With Nvidia’s stock up more than 40% since he gave his “sell” rating in April, Goldberg hasn’t convinced enough investors to come round to his way of thinking... yet.

Related reading: 73 Wall Street analysts cover Amazon, there are 72 on Meta, and 66 write about Nvidia — how many do we need?