The threat of AI disruption has dawned on the bond market

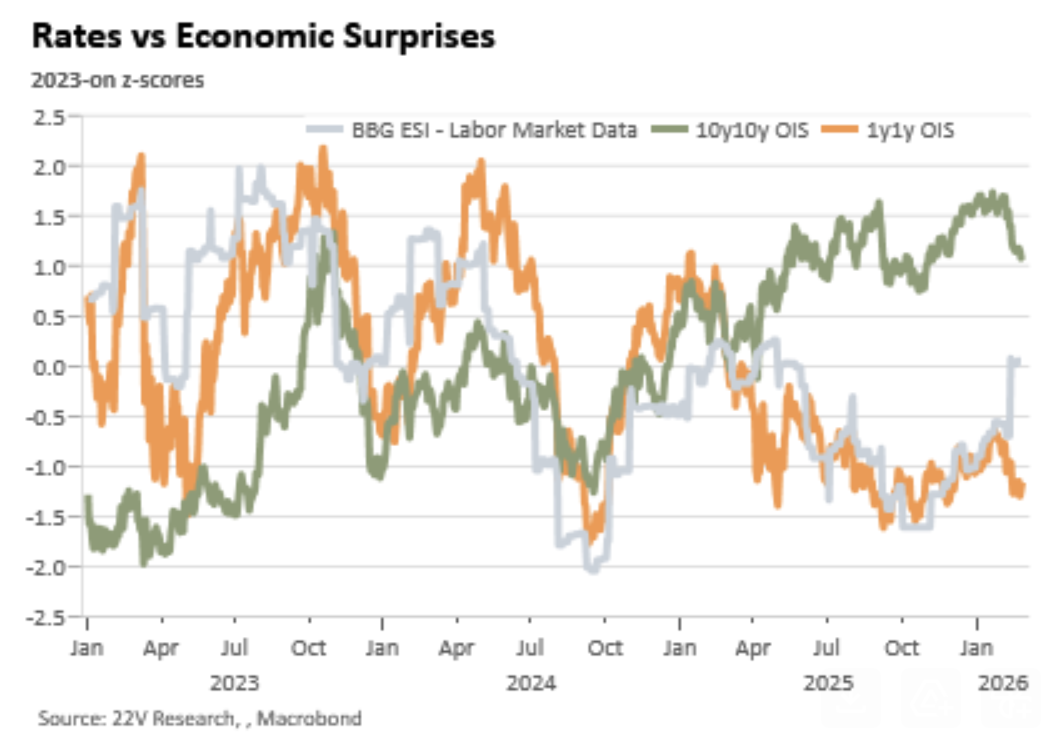

22V Research economist Peter Williams noted that medium-term rate expectations have disconnected from recent encouraging labor market data.

The stock market was ready to countenance and price in the notion of full-blown AI dystopia — if only for a day.

That was the message from this week’s Citrini Crash (potentially the Citrini Capitulation?) in software stocks.

But stocks aren’t the only asset class willing to price in the disruptive medium-term impacts from the aggressive data center build-out and potential widespread deployment of AI agents. It’s happening in the bond market, too — an asset class that encompasses a much wider set of views on economic activity than any particular sector or industry.

Peter Williams, an economist at 22V Research, wrote that short- and medium-term interest rates have been driven largely by labor market surprises over the past two years, but that this typically strong relationship has recently broken down.

“We’ve gone from the risk of a nonlinear weakening in the current labor market to the risk of a future productivity shock that is so dramatic it dislocates many formerly secure workers starting in a few years and building from there,” Williams told us.

What is happening to the job market is influencing where rates will be in the near term, but what AI might do to employment is shaping where rates might end up down the line.

That is, expectations for where interest rates will be in July have crept higher as January’s jobs report helped further diminish fears about previous rises in unemployment, but the pricing of interest rates at the end of next year has gone down amid fears that the so-called SaaS-pocalypse is also effectively a white-collar wipeout, with negative economic consequences.

“Farther out the curve where the concerns raised by the Citrini scenario, and similar AI-related cyclical and structural pessimism, more plausibly play a role fed funds expectations have moved notably lower,” Williams wrote. “It’s a rare enough combo to see markets push rates at these horizons 30-40bps in opposite directions given the usual tight links.”