The S&P 500 inclusion effect springboard is back in a big way

That temporary price bump had cooled throughout the 2010s — now it’s heating up again, per a new Goldman Sachs report.

It’s not unusual to see shares pop when a company is set to join the S&P 500, an index now linked to a staggering $20 trillion in global assets. Just last Friday, Block soared 10% after its inclusion was announced, while Datadog spiked 15% on similar news earlier this month.

Known as the “S&P 500 Index Effect,” this short-lived bump is fueled in part by fresh demand from $13 trillion worth of passive funds and ETFs tracking the benchmark, which are required to buy shares of newly added companies.

But over the past decade, this effect had been losing steam. According to a 2023 Harvard study, the average announcement day return for S&P 500 additions dropped from 9.4% in the 1990s to just 0.8% by the late 2010s — partially because markets got better at absorbing these shocks, and traders got better at predicting inclusions.

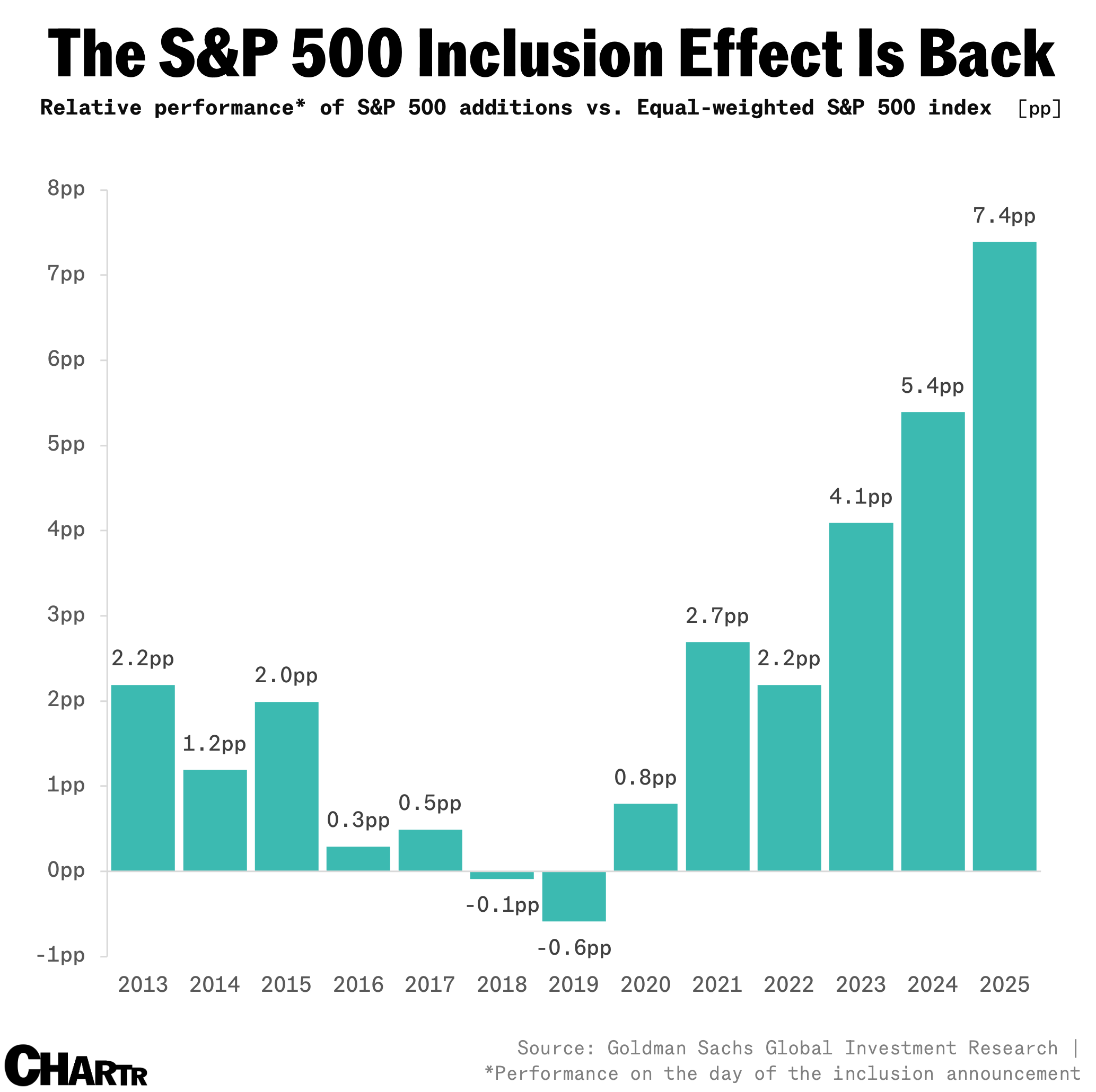

Now, though, a new Goldman Sachs analysis suggests the inclusion effect may be staging a comeback.

Since 2021, stocks newly added to the S&P 500 have outperformed the equal-weighted index by an average of 4 percentage points on the announcement day — with nearly three-quarters of those stocks beating the benchmark.

Source matters

One factor driving the revival is that fewer companies are migrating from the S&P MidCap 400 Index. Per Goldman’s estimate, stocks added from outside the S&P 400 have seen average relative gains of 5.3 pp since 2013, while those graduating from the midcap index actually dipped 0.4 pp.

Retail hype may also be adding fuel, with recent entrants like Coinbase, Super Micro Computer, Palantir, and Datadog already beloved by traders ahead of their debut — and tied to popular themes like AI or crypto.

So, which big names could be next in line for America’s flagship index?

Go Deeper: Datadog is now in the S&P 500. These big stocks still aren’t.