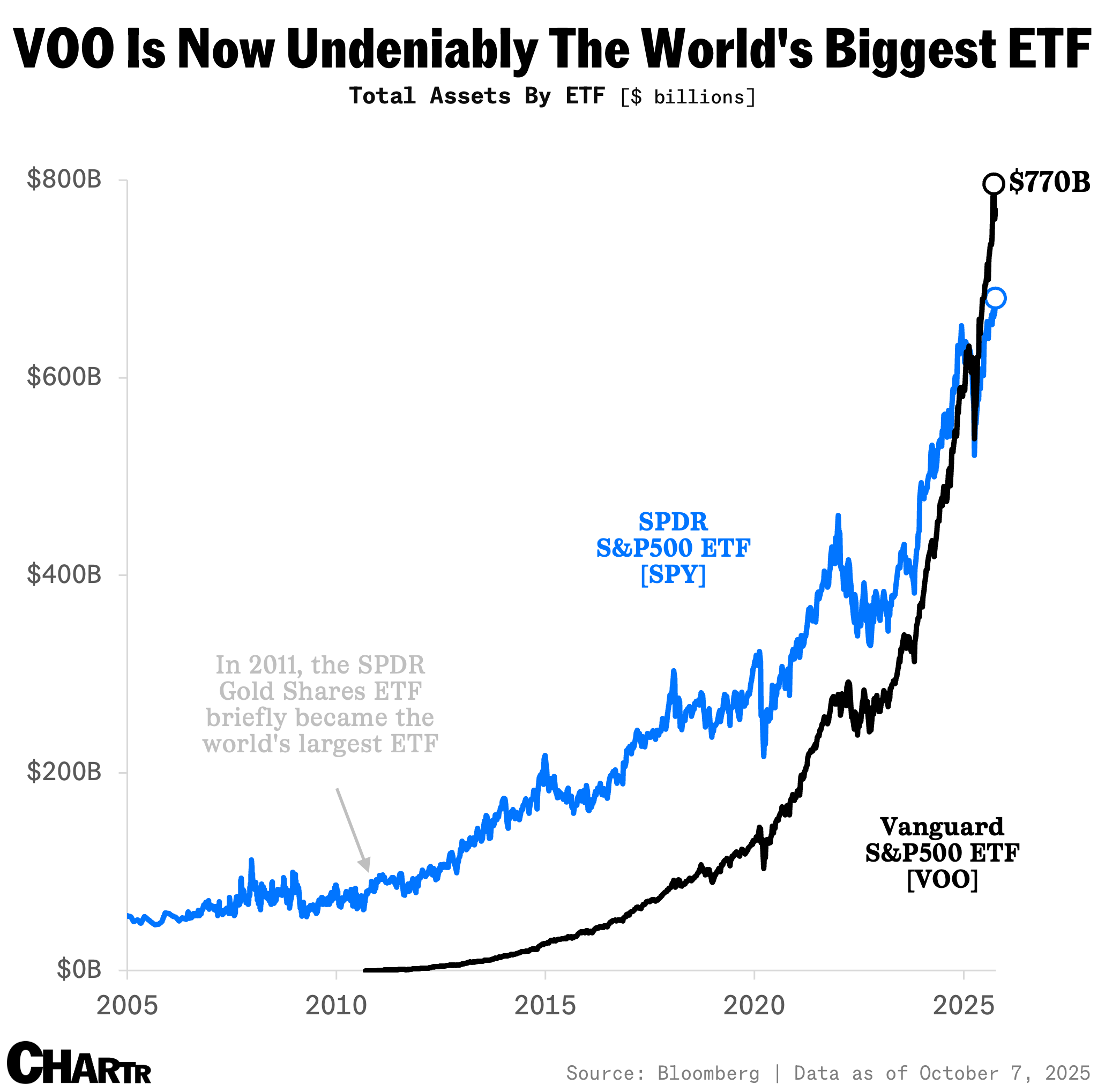

The S&P 500 ETF wars are over — VOO has won out over SPY

After more than three decades at the top, SPY has lost its crown in the S&P 500 Index wars. Now, VOO’s closest challenger is IVV.

The SPDR S&P 500 ETF (SPY) is seeing the largest annual withdrawal ever for an ETF, widening the gap even further with its now dominant rival, the Vanguard S&P 500 ETF (VOO).

According to the Financial Times, investors have pulled a record $32.7 billion from SPY so far this year, even as the S&P 500 it tracks has climbed 15% year to date.

That adds another blow to the State Street-run index fund, often synonymous with the ETF boom. Earlier this year, SPY lost its three-decade reign as the world’s largest ETF to Vanguard’s VOO — which now counts some $770 billion in assets — and soon after, it even slipped behind BlackRock’s IVV, which manages $702 billion.

At the heart of VOO’s rise is its cost advantage, charging just 0.03% in annual fees, less than a third of SPY’s 0.09%. The difference may seem trivial — roughly ~$6 a year on a $10,000 investment — but apparently, it’s a gap hard to ignore once those savings compound over the longer term.

Indeed, cost-conscious, buy-and-hold-forever retail investors are now powering the ETF market once driven by institutions and traders chasing SPY’s liquidity. Retail investors today account for three-quarters of US ETF assets, up from 56% in 2015, per data from Broadridge Global Market Intelligence.

And while VOO’s appeal lies in its simplicity, the broader ETF market is getting increasingly noisy and flashy: the US now has more ETFs than listed public companies, including a growing crop of niche products, active ETFs, and meme stock funds.

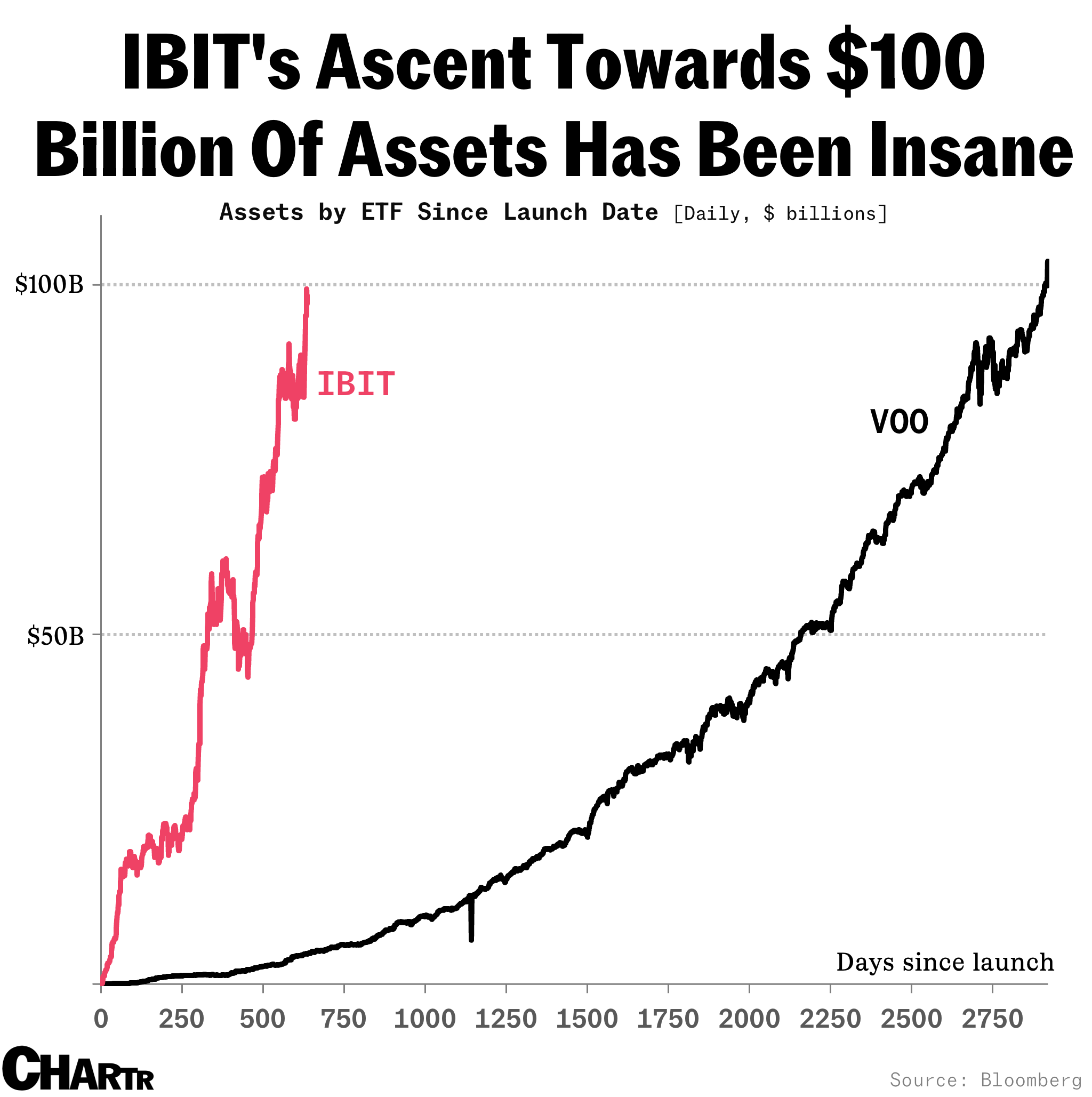

Another ETF that’s crushing it? BlackRock’s IBIT — which is making VOO’s early growth look glacial.

BlackRock’s bitcoin ETF is on the cusp of $100 billion in assets, a milestone it will have achieved in less than two years

While VOO might be the largest ETF in the world, IBIT — BlackRock’s iShares Bitcoin Trust ETF — is the fastest-growing. And the bitcoin-centered product is on the cusp of a major milestone, reporting that it now holds 802,257 BTC, putting it within a whisker of hitting $100 billion in assets (worth roughly $99 billion in good old-fashioned USD at the time of writing).

Considering that BlackRock’s iShares Bitcoin Trust launched only 636 days ago, that’s a remarkable speedrun, as individual and institutional investors have embraced cryptocurrency via the exchange-traded fund. For context, VOO took over 2,900 days to hit the same milestone (about eight years).

As noted in a great piece by Robin Wigglesworth in the Financial Times, IBIT is now a major money-spinner for one of the biggest stalwarts of TradFi. As the largest exchange-traded product in the crypto space, and with a not insignificant expense ratio of 0.25%, the ETF is pulling in somewhere in the region of $250 million of revenue for its asset manager parent company. As Wigglesworth puts it:

“Anyway, it’s heartwarming to see that one of the companies profiting the most from an anarchical, decentralised invention supposedly designed to reorder the global financial system is... BlackRock.”