Why pension funds’ love affair with private equity is bad for the environment

Jamie Dimon highlighted that pension funds' private market investments are hindering their ESG goals.

Back in April, I highlighted some concerns I had with pension funds doubling down on private equity. My issue, at the time, was that I thought it was a risky investment. For context, funding ratios (a pension’s assets divided by its liabilities) for state and local pensions had declined from 100%+ to 78% from 2001 to 2022, despite a strong performance from the stock market over that time.

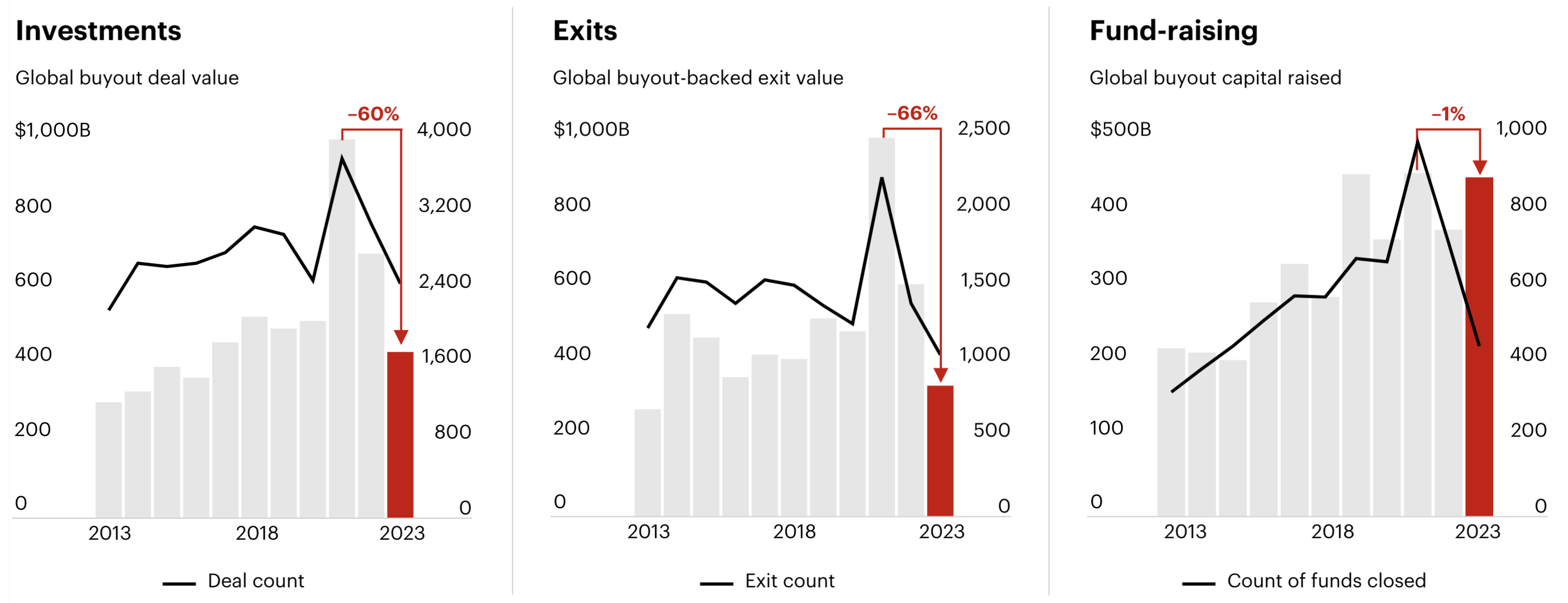

In an attempt to improve their returns, many funds turned to private equity, as it had outperformed the S&P 500 on a 20-year, 10-year, 5-year, and 3-year horizon. However, with private equity funds now distributing less to investors than they are raising through new funds, and capital being tied up in funds longer and longer, some pensions have had to sell their PE fund stakes on secondary markets at an average of 85% of their recent valuations, creating a drag on returns.

However, another consequence that I hadn’t thought of was that pension funds’ love affair with private equity could be hindering their environmental activism. On October 9, Reuters reported that JPMorgan CEO Jamie Dimon recently called out pension fund managers for increasing their allocations to private equity while simultaneously voicing environmental and social concerns:

'You call me up and talk to us about all the issues you're interested in. But when you make huge investments in the private side, you don't get that kind of transparency,’ he told a meeting of the Council of Institutional Investors in New York on Sept 10…

There could be 15,000 publicly traded companies in the U.S. rather than around 4,500 today, Dimon suggested. Instead private markets have taken up a major share of new investments without nearly as much disclosure, liquidity or research, the JPMorgan CEO said.

‘You all are huge causes of that, because you make huge investments on the private side,’ Dimon told the audience that included representatives from Democratic-leaning state and local pension systems that have taken activist stances on environmental and social issues.

Many public pension funds, such as CalPERS, have been outspoken about their environmental activism, with the US’s largest pension plan taking an activist stance against ExxonMobil in May of this year after the company filed a lawsuit to block a vote on a climate proposal.

Unlike public companies, which are beholden to more shareholder disclosures and face increased shareholder scrutiny regarding their ESG disclosures, private companies are less transparent with their operations, making it more difficult for investors to track their environmental impacts.

Given the increased transparency and increased liquidity of public markets, it seems like it would be a win-win, from both a financial and activist perspective, to allocate more capital toward public markets, not less. But considering that CalPERS voted to increase total private market allocation from 33% to 40% in March, it looks like more of the same for the near future.