GOAL

Soccernomics

How England’s most valuable soccer team loses money

The economics of Man Utd.

There’s more cash than ever in English soccer, and one of its biggest teams is thinking about investing billions into a new stadium. The only problem? It’s started losing money.

The English Premier League has been back underway now for just over a month, meaning that many of the most fervent soccer fans and sports gambling enthusiasts in your life will have been spending their weekend mornings watching nail-biting matches between teams like Brighton & Hove Albion, Nottingham Forest, and Wolverhampton Wanderers, as well as a host of sides that don’t sound made up.

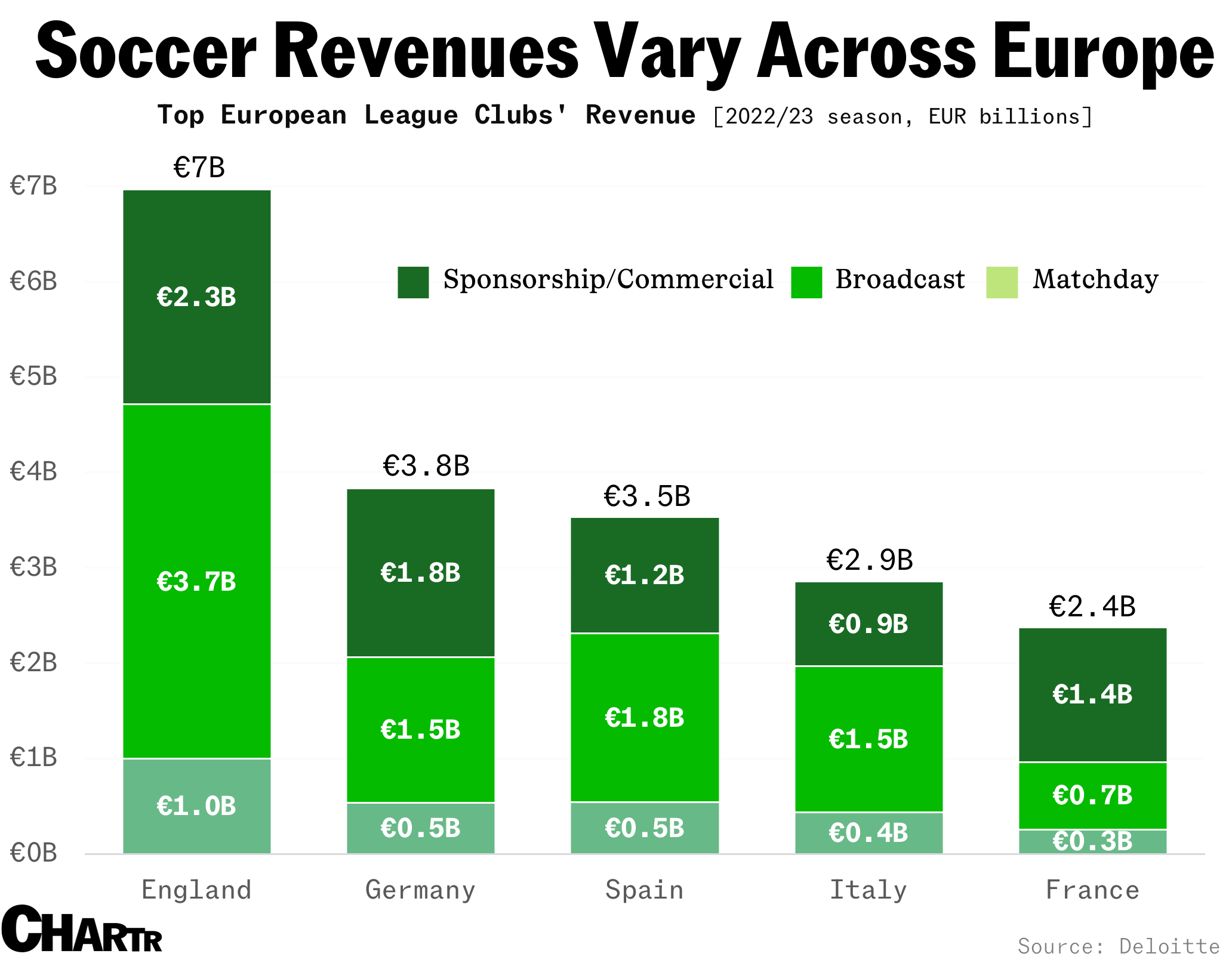

With massive global brands like Liverpool, Manchesters City and United, Arsenal, and Chelsea in amongst those provincial sounding teams, the Premier League has boomed in recent decades to become a critical cultural — and financial — UK export. Global broadcast deals see matches beamed into as many as 900 million homes across 189 countries, helping England’s top flight teams amass a whopping €7 billion ($7.8 billion) in revenue for the season ending in 2023, according to Deloitte’s latest Annual Review of Football Finance.

Moneyball

Indeed, 6 of the top 10 most valuable soccer teams in the world in 2024 are English — and top of that PL pile, according to Forbes at least, is Manchester United. The team’s success in the 1950s and 1960s cemented its legacy with an older generation of fans, but Manchester United only really became the global phenomenon that it is today thanks to the success of the men’s side from 1986-2013, when it was run by much-decorated Scottish manager, Alex Ferguson.

Given its global following (the club reportedly counts 1.1 billion fans and followers around the world, more than 3X the population of the United States), and the rising fortunes of English soccer more generally, you might expect the team to be a profit machine. Thanks to Manchester United shares trading on the New York Stock Exchange since 2012, the team’s financials are public (United remains majority-owned by the Glazer family, but some shares trade on the NYSE), and they tell a very different story.

In the red

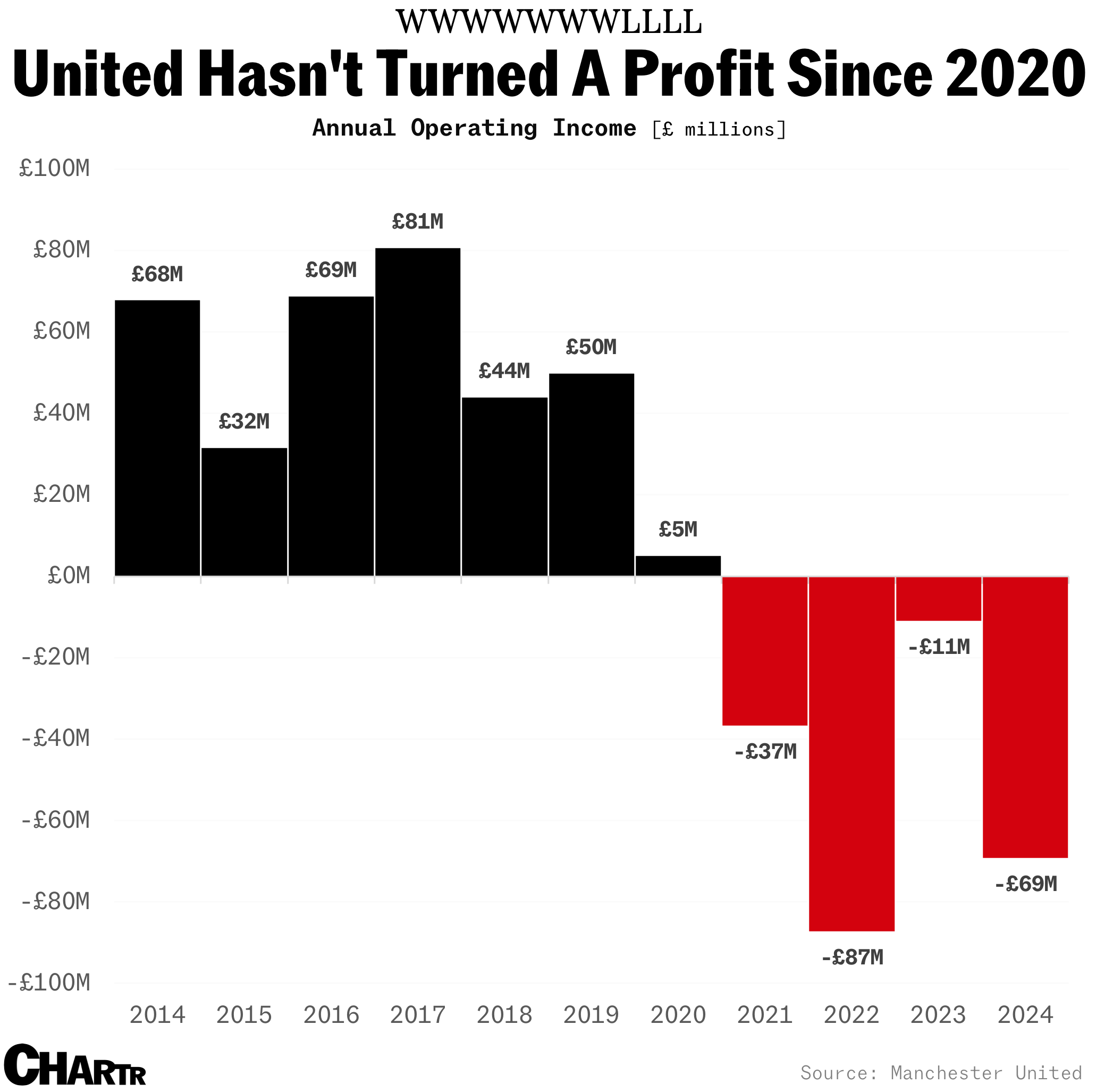

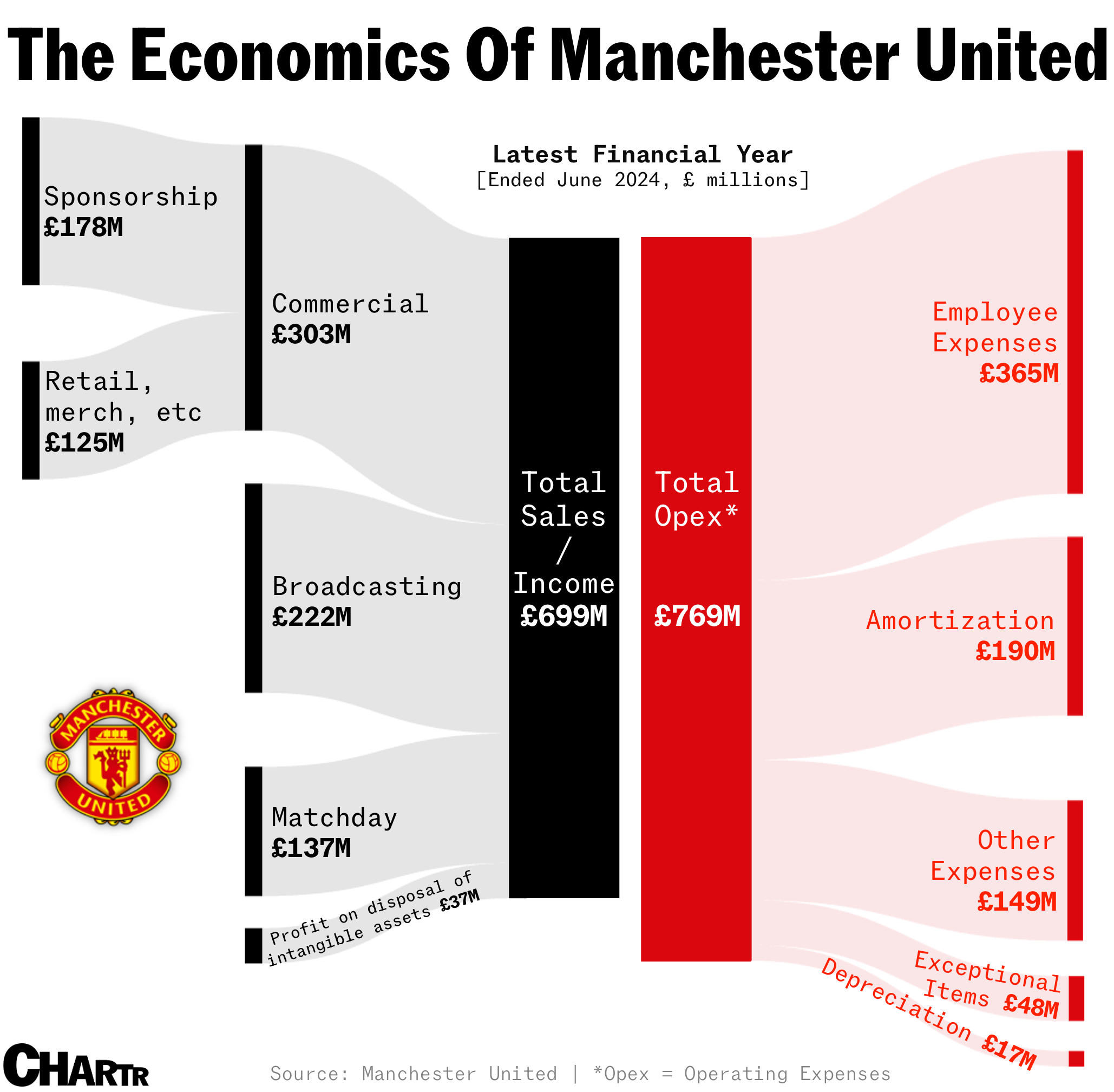

Manchester United, its $6.55 billion valuation second only to Real Madrid’s per the Forbes ranking, has posted cumulative operating losses to the tune of £205 million ($275 million) over the last 4 years, down almost £70 million in the last year alone. The bad news for any budding Ryan Reynolds types out there with a penchant for The Beautiful Game and a wad of cash to invest? Manchester United’s finances aren’t out of the ordinary for soccer teams, even at the highest level where sides can leverage multiple income streams.

The Red Devils — a puerile nickname for United that genuinely pains me to write as a Manchester City fan — made nearly £700 million (~$936 million) in revenue in the last financial year. A little over 43% of that came from its commercial division, which includes the sales of retail merchandise and apparel, as well as sponsorship, with brands paying millions to have their logos adorn the team’s jerseys, shorts, stadium, and grounds. United’s share of broadcasting deals added another £222 million to its coffers, while actual match takings contributed £137 million.

But despite all of its income, the team’s costs were still too high for it to turn a profit.

Paying players like Brazilian midfielder Casemiro ~£350,000 a week soon adds up to a mammoth wage bill for United, with employee expenses coming in at an eye-watering £365 million ($489 million) last year. And, unlike many North American sports which tend to operate in a closed-system, soccer teams don’t typically trade players, they just buy and sell them. For a franchise like Manchester United, that typically means paying up to acquire the best talent. And although it might seem oddly reductive, players are treated like assets, and almost all assets tend to depreciate over time — the team’s reported “amortization” (a handy accounting label that essentially divides the transfer fees of players over their expected tenure at the side) was £190 million last year.

New Trafford?

Manchester United’s iconic stadium, Old Trafford, is living up to the first half of its name. Indeed, the “Theater of Dreams” is 33 years older than Joe Biden, having been built in 1910. Given its advanced years, the club, and its new minority owner Jim Ratcliffe, is weighing up proposals on a redevelopment of its iconic home arena, or a new stadium altogether.

Both options are expensive. A new ground could reportedly cost the club more than £2 billion over the next 6 years, and would obviously be a significant weight on United’s sagging bottom line. How it finances such an investment, given that it’s heavily indebted (and loss-making, as we’ve seen), is a hot topic of discussion, with Manchester officials concerned that local taxpayers might end up footing some of the bill indirectly.

As mentioned, losing a lot of money in the top flight is no rare occurrence, with just 4 clubs managing to squeeze out a pre-tax profit in the 2022/23 Premier League, down from 7 the year before, according to Deloitte research. What is slightly less common is Manchester United’s status as a publicly-traded company.

Emotionally invested?

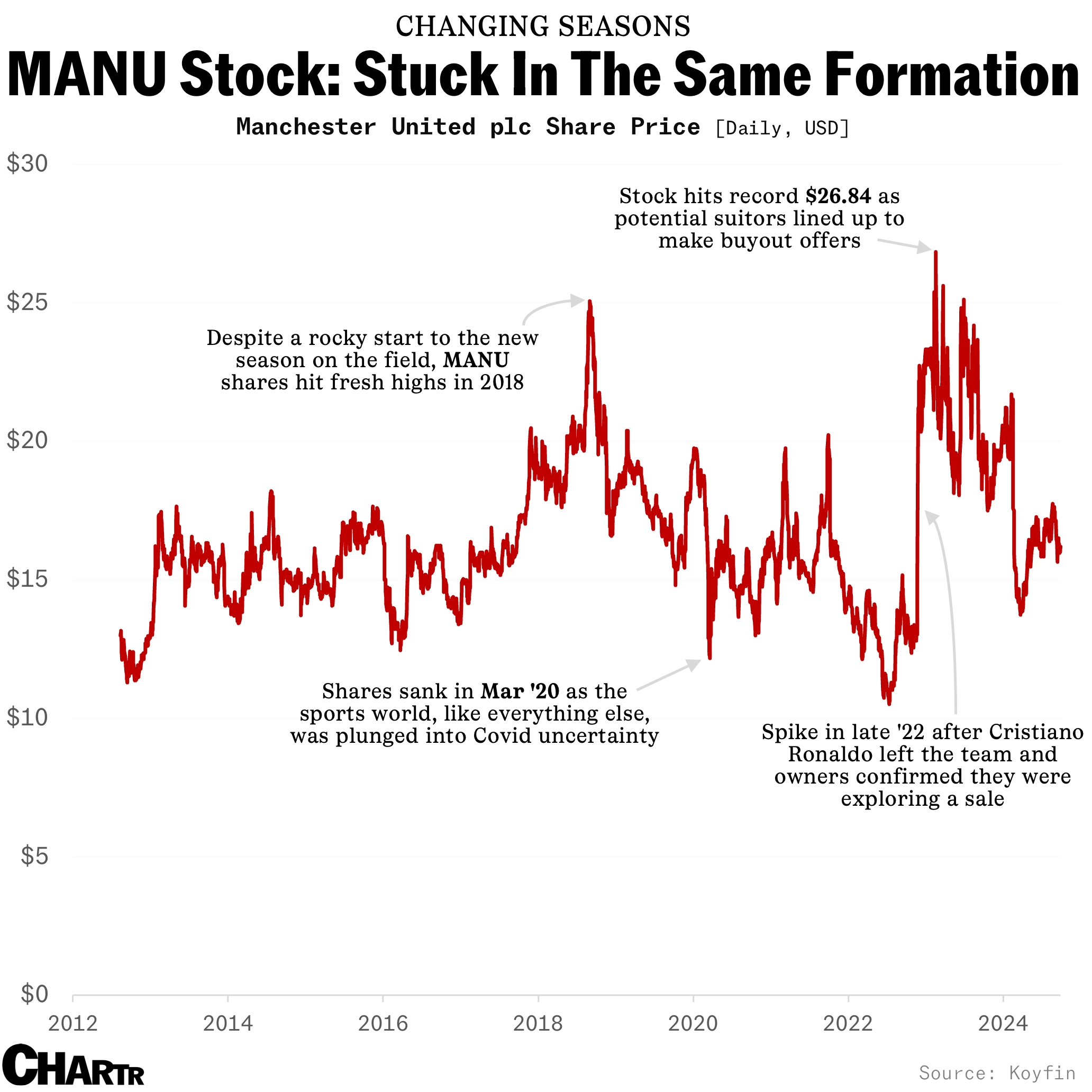

After initially being floated on the London Stock Exchange in 1991, then being taken private again by Malcolm Glazer in 2005, Manchester United was partially listed on the NYSE in August 2012, with analysts at the time wary about the stock’s long-term prospects. So far, MANU hasn’t done much to prove them wrong. Since August 2012, the soccer stock has risen just shy of 25% — in the same period, the S&P 500 Index has gained more than 300%.

The stock’s been on a bumpy ride over the last 12+ years, rising slightly on standout match results and star signings, and, predictably, slipping on heavy losses. However, the biggest movements in the Manchester United stock tend to follow its more mundane corporate newsflow, rather than any particularly exciting on-field action.

Like in the worlds of baseball, basketball, and American football, there’s a limited pool of publicly-traded soccer sides to use as comparisons, though Italy’s Juventus and Germany’s Borussia Dortmund perhaps serve as 2 of the closest parallels. Two titans of European football, Juve and Dortmund are down 76% and 60% from their respective openings, as the majority of teams on the continent struggle to stack up against their English counterparts… at least in financial terms.

A big lesson from all this? Whether you’re a billionaire would-be owner or just a regular fan, investing in your favorite team might only make sense if the thrill of following their on-field results just isn’t dramatic enough.