The company Puerto Rico hired to run its indebted power plants is collapsing under its own debt

The island’s utility was $9 billion in debt. New Fortress Energy was supposed to power a turnaround but instead is struggling with its own massive $9 billion debt load.

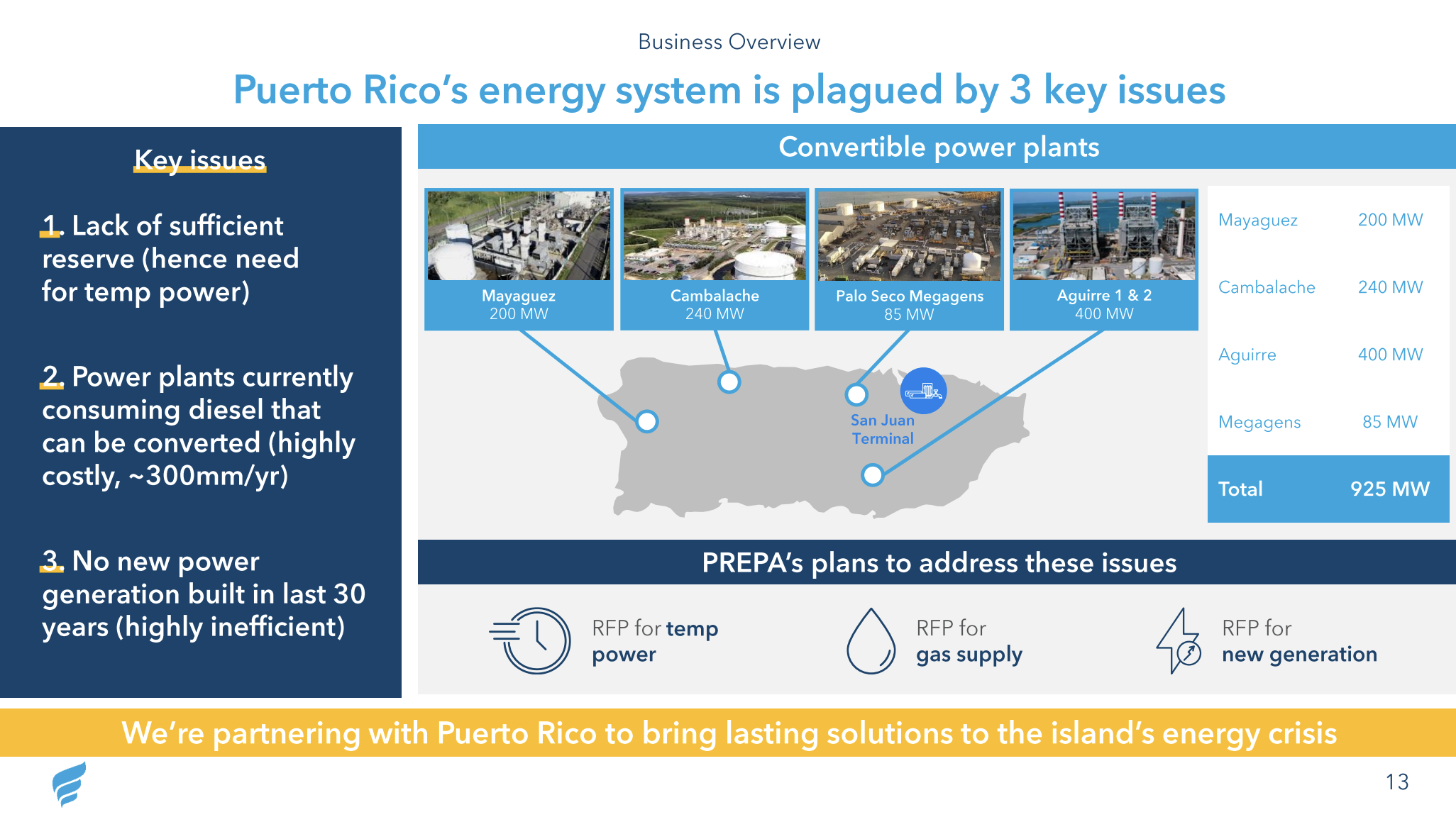

Two years ago, Puerto Rico privatized the operations of its power plants as part of a plan for the US territory’s state-owned utility to claw its way out of more than $9 billion in debt to bondholders. The grid went down and balance sheets fell into the red under the Puerto Rico Electric Power Authority’s watch, so the bankrupt Caribbean island’s White House-appointed fiscal overseers reckoned a company with shareholders would import market wisdom and financial discipline to a place credibly described as the world’s oldest colony.

The lucrative contract to run the island’s generating stations went to Genera PR, a subsidiary of New Fortress Energy. The New York-based natural gas company, cofounded and controlled by billionaire Wes Edens (who also co-owns the Milwaukee Bucks), was already selling fuel to PREPA, drawing ire from critics who cried foul over what they saw as a “rigged” deal.

Now, New Fortress Energy is heaving under the weight of its own debt load of roughly $9 billion. It was forced to sell off one of its most lucrative assets to pay back creditors, who are starting to show signs of skittishness over the company’s future. And Puerto Rico, the captive market New Fortress expected would be a steadily expanding source of revenue, just excluded the company from its latest bid for gas.

The stock price has nosedived by nearly roughly 80% since the start of the year. A surprise contract extension in Puerto Rico gave the stock a much-needed boost this week, sending shares surging nearly $4 as of Wednesday afternoon. But that was still less than one-sixth of the price last July. And last month, Fitch Ratings downgraded the equivalent of the company’s credit score to “CCC,” citing increased risk of default.

It’s been a dramatic fall. At its stock market debut in 2019, the company outlined plans to build out a complete supply chain to deliver liquefied natural gas (LNG), the fuel’s super-chilled liquid form, which makes transportation easier. That included liquefaction terminals, tanker trucks, LNG tankers, floating storage units, import terminals, and gas-fired power plants — and came with a high price tag.

In the first few years before its IPO, New Fortress Energy spent more than $306 million.

For years, the company rode the wave of the market’s excitement over LNG exports. New Fortress Energy had a unique pitch focused on proprietary technology that could be mass-produced to cool gas into its liquid form and a model for shipping the fuel via shipping containers.

“New Fortress’ business model was supposed to differentiate it by being more nimble and small,” said Daniel Sherwood, an analyst and researcher who has tracked New Fortress Energy for years. “But those business models didn’t end up taking off the way that they thought they would, certainly not at the same rate as your more traditional kind of LNG players like Cheniere.”

Between its IPO in 2019 and the first quarter of 2025, the company’s capital expenditures totaled nearly $8.4 billion. That money bought a small empire across Latin America and the Caribbean, with LNG facilities from Mexico to Jamaica to Brazil. Puerto Rico represented a crown jewel where control over the power system seemed to guarantee a growing market for gas deliveries.

Throughout that same period, however, the cumulative cash from New Fortress’ operations totaled just $1.5 billion.

“They spent $8.3 billion to generate $1.5 billion,” said Clark Williams-Derry, an oil and gas analyst at the Institute for Energy Economics and Financial Analysis, which has long criticized the company’s operations in Puerto Rico. “And it spent that while also paying out hefty dividends to its investors.”

Cancellations and delays dogged the company, meaning the revenue needed to pay off that spending failed to arrive. The company planned on constructing an LNG liquefaction facility in Pennsylvania to tap into the rich supply of gas from the Marcellus Shale. Later, New Fortress said it would send the gas by truck or rail to a port in New Jersey. As public opposition mounted, though, the company put the project on hold. The last three annual reports provided no substantive updates on the project.

New Fortress Energy had laid out plans to build up to 10 liquefaction projects over five years, but managed to complete only one small terminal in Miami by the fifth anniversary of its IPO last year.

With too little cash on hand to pay off debts, the company announced the sale of its operations in Jamaica in March. The transaction was completed in May.

“They now have more wiggle room and can meet their expenses for the next year, depending on how things go,” Williams-Derry said. “But what they sold off was some of their more profitable assets, so what’s left is less profitable.”

The sale reduced the company’s debt by a little under 3%, going from $8.9 billion to $8.7 billion — but cut quarterly revenue by 20%, according to Williams-Derry.

“It’s like selling a kidney to delay a mortgage payment by a few months,” he said.

Meanwhile, the company’s troubles in Puerto Rico have mounted. New Fortress built out an import terminal in San Juan Bay without going through the federal permitting process. The company made a novel legal argument for skipping approvals from the Federal Energy Regulatory Commission, arguing that because Puerto Rico doesn’t connect to an interstate pipeline network, it wasn’t covered under the Natural Gas Act. FERC ultimately disagreed and ordered the company to go through permitting amid mounting concerns that the facility risked an explosion or gas leak in the island’s densely populated capital city.

Under the watch of New Fortress’ Genera PR, all of the island’s power plants went offline in April, triggering an island-wide blackout.

Around that same time, Genera requested that the Puerto Rican government allow the company to cash in on the incentives in its contract, taking $118 million up-front to help pay down debts but forgoing as much as $1 billion in long-term bonuses for good performance.

“It was very unlikely they’d hit the full $1 billion payment. That was only if they knocked it out of the park every year going forward,” Williams-Derry said.

“My sense is there’s been a lot of frustration about Genera’s performance in keeping the power system going and the fact that they’ve been doing everything they can to squeeze money out of the one of the poorest places in the United States,” he added. “It always struck me that the point of New Fortress’ involvement in Puerto Rico’s electricity system was to be able to gouge Puerto Ricans for cash.”

But residents aren’t the only people potentially being ripped off, he said.

The company’s dividends paid back investors who bought shares after the IPO, and New Fortress Energy issued more stock last year.

“Those people haven’t been repaid yet,” Williams-Derry said. “If the company goes belly-up, the owners of the company on net won’t have lost money.” This, he warned, is legal but “not a good look for Wall Street.”

“It looks a little bit Ponzi-ish when the dividends are the money that’s paid in. They’ve paid back the original investors with the money they put in in the first place,” he said. “The other alternative is the investors put money back into capex and now the company has borrowed money from lenders and given it to their shareholders — borrowing from Peter to pay Paul.”

None of this “would particularly matter if this was a company that was growing, successful, generating cash, and turning itself around,” he continued. “If it was on the ascent, they’d at least have a whole lot of stuff with the potential to generate cash. But they don’t.”

When the company put out a more detailed assessment in its latest quarterly earnings this week, it said it may struggle to enter into new contracts or renew existing deals to charter tankers “on favorable terms or at all, which may result in us not being able to meet our obligations.”

Following the release, an investor note on the stock website Seeking Alpha cautioned that, while there were potential ways New Fortress Energy could turn itself around, “given the overall size of the debt load and the short-term liquidity constraints, it seems even more likely that debtors could take control of the company in restructuring, or bankruptcy proceedings could move ahead.”

In its most recent 29-page 8-K filing with the Securities and Exchange Commission, New Fortress Energy warned that it was still assessing whether it “will have sufficient liquidity to meet our obligations as they become due over the next twelve months.”

“There are inherent risks with the company’s ability to continue to implement plans in future periods that will support its liquidity positions, such as its ability to further extend the terms of vendor payments,” the filing stated.

In other words: it’s not clear whether the company will have the money to pay its bills as they come due, and time is running out.

New Fortress Energy did not respond to multiple emails requesting comment.

Alexander C. Kaufman is an award-winning journalist whose work has appeared in The Atlantic, Heatmap, Canary Media, and HuffPost, and who writes the Field Notes newsletter.