India’s Ola scooter company is too good to be Bird 2.0

An electric scooter company is poised to have the biggest Indian IPO this year, and it hopes to avoid its predecessor’s fate in the public markets.

Since 2021, when global IPOs raised $460 billion across 2,436 new public listings, investor demand for new issuances has drifted lower and lower, with 1,415 IPOs raising $184 billion in 2022, 1,351 IPOs raising $126 billion in 2023, and just 551 IPOs raising $52 billion in the first half of 2024.

Despite the global slowdown, one country has proven to be a bright spot: India. The south Asian country accounts for 27% of global IPOs by deal volume so far in 2024, up from 13% over the same period last year, and Indian companies have raised nearly $5 billion, almost doubling the amount of capital raised in India in the first half of 2023. While Indian IPOs are still smaller than their US counterparts (cold storage supplier Lineage raised $4.4 billion in its Nasdaq IPO last week, for example), India’s year-over-year IPO growth is still bucking the trend of global markets.

Earlier this week, Reuters reported that Indian e-scooter maker Ola Electric aims to raise $734 million in its upcoming IPO, which would make it the country’s largest IPO of the year. My first thought, when seeing this headline, was “here comes Bird 2.0.” Bird, the Miami-based e-scooter company, raised $883 million in equity funding since its founding in 2017, went public through a reverse merger with a SPAC at a $2.3 billion valuation in November 2021, and filed for bankruptcy just two years later.

Of course, Bird had no business being a public company. In its initial SPAC filing, it projected $401 million in revenue, $110 million in gross profits, and -$28 million in adjusted EBITDA in 2022. In reality, 2022 revenue was $245 million, gross profit was just $35 million, and the company lost $359 million.

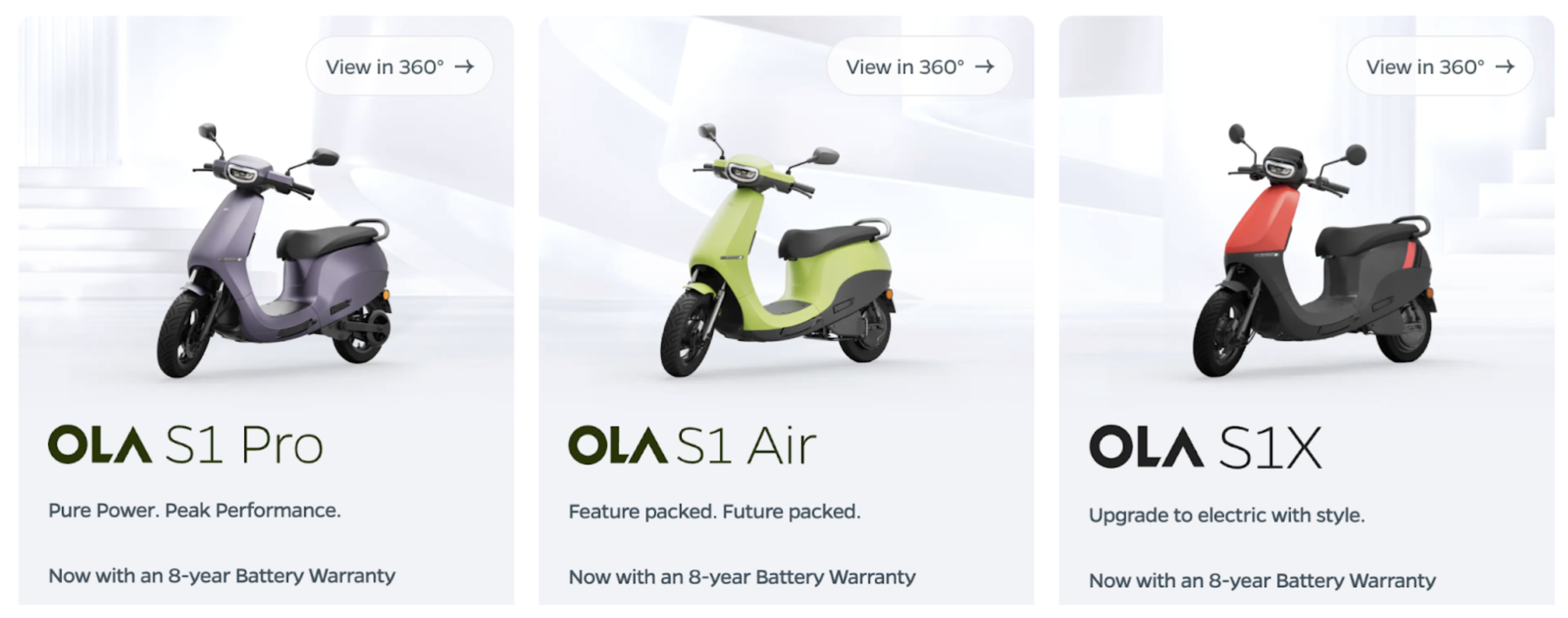

However, the Indian market is far different from the American market, and Ola’s business is far different from Bird’s. Almost 75% of all vehicles in operation in India are two-wheeled, while 93% to 99% of new vehicles registered in the United States each year between 1960 and 2020 were automobiles like cars, trucks, and vans. Ola’s “scooters” are also much different from the Bird scooters littering sidewalks around the US: they’re electric mopeds. From a product-market fit perspective, Ola has more in common with Tesla a decade ago than Bird in 2021: it’s electrifying the primary mode of transportation in its domestic market.

Ola’s business is also trending in the right direction. Revenue has increased from ~$12 million in 2021, to $54 million in 2022, to $332 million in 2023, and while it’s still not profitable, profit margins have shrunk from -157% in year-end March 2022, to -39% in the year-end March 2023, to just -14% in June 2023 quarter. While it’s still below the median profit margin of this year’s Indian IPOs (8%), Ola’s financials are trending in the right direction.

Going back to the Bird example, two reasons that Lime (a frequently compared US shared e-scooter project), has succeeded while Bird failed are:

Bird opted to buy scooters from Chinese markets, while Lime invested heavily in building its own bikes and scooters, creating a differentiated product with a longer operating life that improved unit economics.

The scooter market, like the rideshare market, quickly became winner-take-all, and Lime’s partnership with rideshare leader Uber embedded its scooters and bikes in the Uber app, giving it a competitive advantage.

Like Lime, Ola manufactures its own vehicles and many of its own components, and the e-scooter company is continuing to invest in its own battery technology. Ola also dominates the electric two-wheel vehicle market, accounting for 50% of sales in May 2024. While some investors are (rightfully) wary of “electric scooter stocks” Ola appears to be a far cry from Bird 2.0.