Google may have to sell off Chrome — but who could buy it?

Forcing a sale of Google Chrome could weaken Google’s stranglehold on search.

“Which lawyers did Microsoft use for its antitrust case in 2000” — Google execs this morning, probably.

Done searching

According to a report from Bloomberg yesterday, Department of Justice officials are planning to recommend that Amit Mehta — the US District Judge who ruled in August that Alphabet’s search giant holds an illegal monopoly over the market — force the company to sell off its Google Chrome browser, impose data-licensing requirements, and implement measures around the company’s Android operating system and burgeoning AI efforts.

Those recommendations show just how serious America’s antitrust authorities are about cracking down on Google’s dominance in the world of looking stuff up online. It’s the biggest antitrust action against Big Tech in the US since the United States vs. Microsoft Corp. case more than two decades ago (spoiler: Microsoft wasn’t broken up).

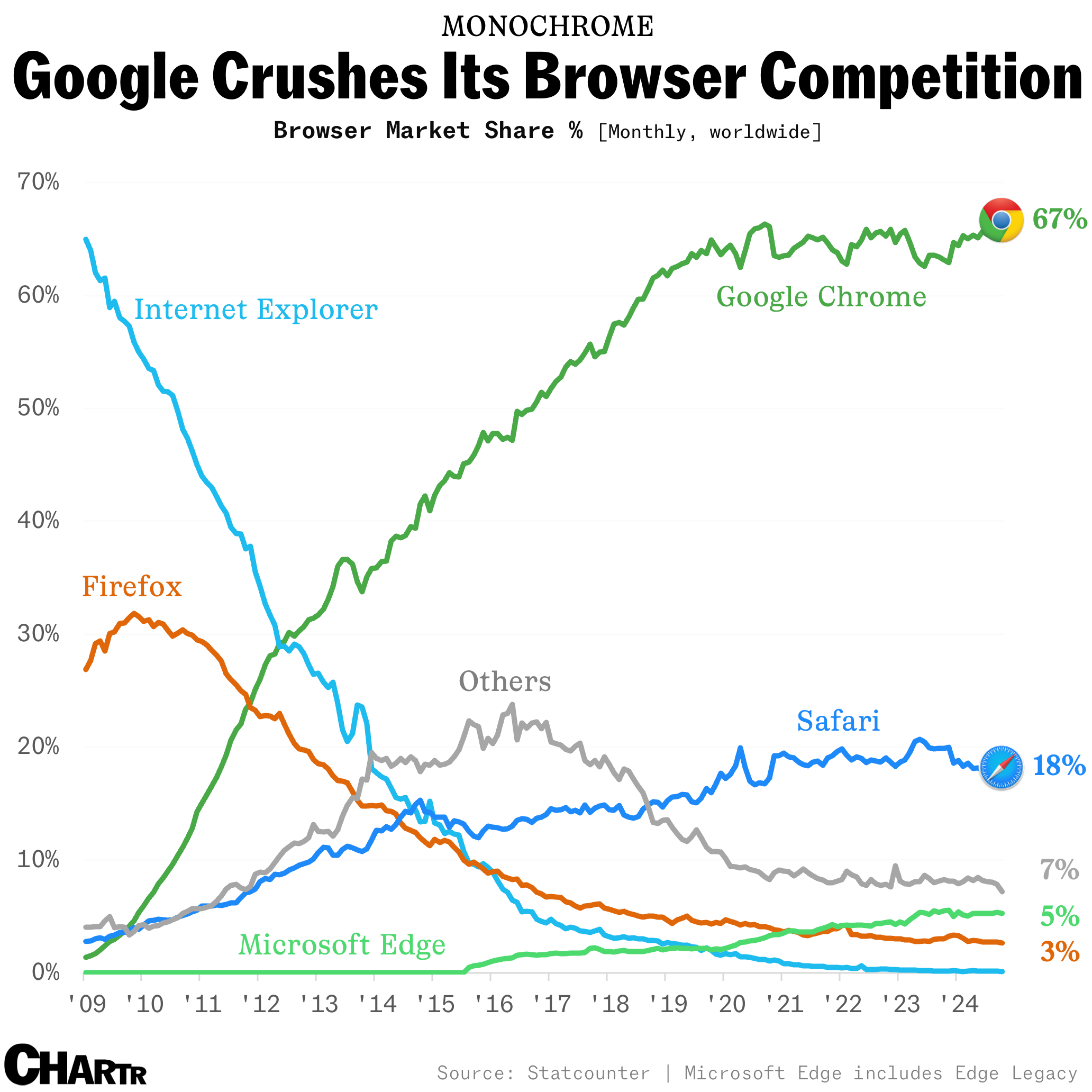

According to Statcounter, Google Chrome has a 67% share of the global web-browser market — way ahead of the next biggest competitor, Apple’s Safari, the default browser on every iPad and iPhone (unless users switch their settings). Though Chrome isn’t a huge money spinner in a direct sense, being free to download and use, it’s a phenomenal source of traffic for the search engine itself, which makes plenty of money (some $49 billion last quarter). On Chrome, users are sent straight to google.com by default when they search, and Google gets data on what logged-in users are doing, helping its targeted-advertising efforts.

Gatekeeping gateway

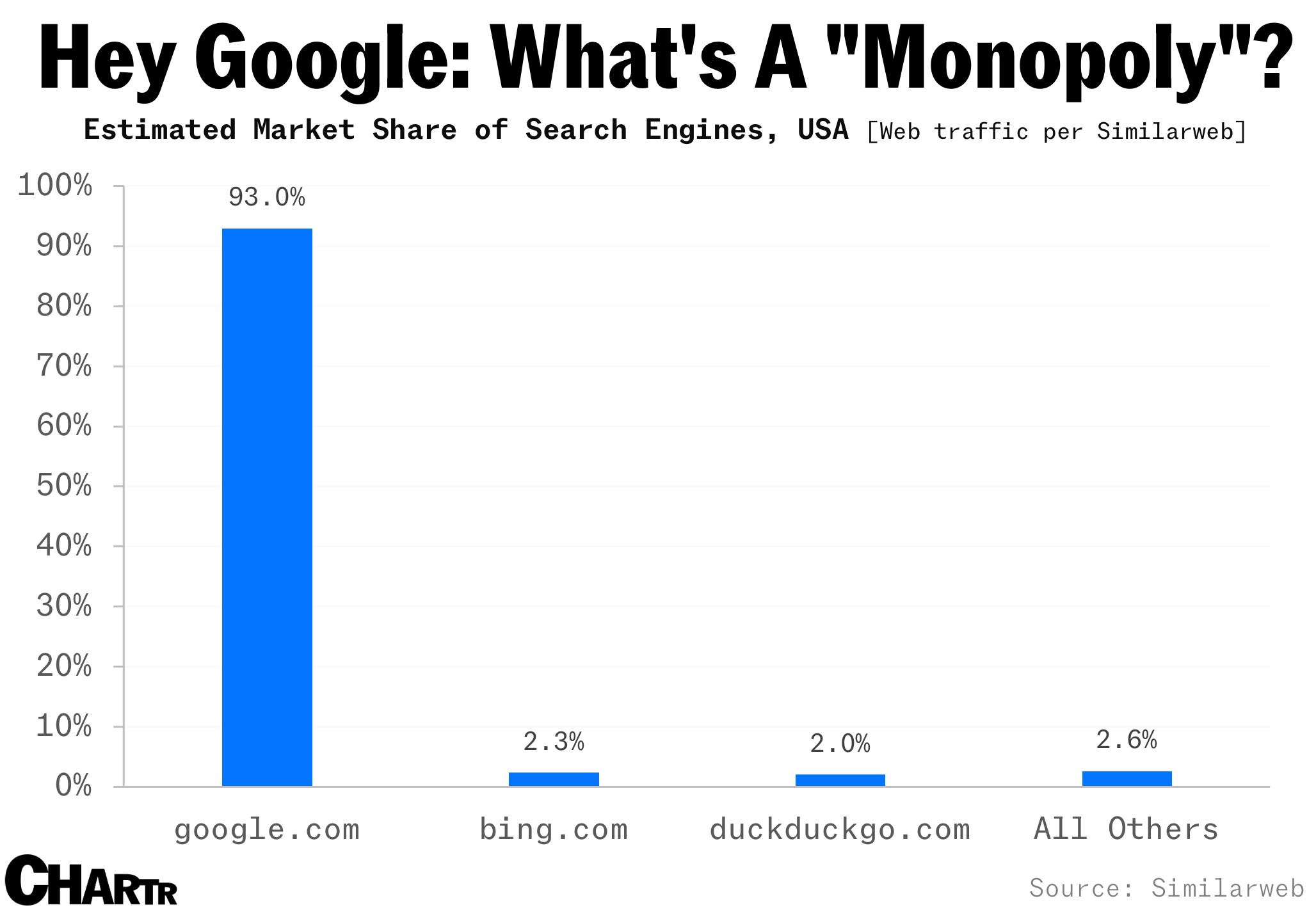

While Chrome was never really the product at the heart of the DOJ’s lawsuit, which was first launched under the Trump administration in 2020, the browser plays a massive part in the crux of the case — Google’s total domination of search. According to website-intelligence platform Similarweb, google.com has a staggering 93% share of American web searches.

That level of domination, as antitrust expert George Hay simplified for Sherwood News in the wake of the August ruling, amounts to a monopoly which Google monetizes with advertising and cements via exclusive deals with the makers of Apple and Android devices. Thanks to unsealed court documents, we know that Google paid Apple an eye-watering $20 billion in 2022 alone to be the default search engine in Apple’s Safari browser. If Chrome was owned by someone else, Google would presumably have to pay to be the default search engine in a similar fashion.

The obvious complication with forcing Alphabet to sell Google Chrome is that it’s really big. There’s not that many companies that could afford and make use of an internet browser that has hundreds of millions of users and, from the small pool of competitors that could (e.g. Amazon, Microsoft, Apple), which of them would be impervious to the same monopoly charges further down the line? While such recommendations might work in theory, breaking up Google in practice, as Rani Molla observed in August, will prove hard to do.