The real-world benefits of index options

Index options offer advantages like flexible contract sizes, no early assignment risk, cash-settlement, and special tax treatment.

If you trade equity options, you may assume that index options trade exactly the same way, but there are some crucial differences. While equity options and index options share many characteristics, index options offer some unique advantages.

We’ll walk through some of traders’ common needs and concerns, show how index options are poised to meet these needs, and dive into some real-world examples of how an index option trader and an ETF or stock option trader might experience different outcomes.

“I need affordable contract sizes”

A SPY options trader wants to make a play on the S&P 500® Index. They’re familiar with the benchmark SPX®, but as a retail trader, they’re worried that they don’t have the capital to trade index options.

Myth: Index options are too expensive.

Fact: Index options contracts come in multiple sizes.

What traders might not realize is that Cboe® offers smaller contract sizes ideal for retail traders. Cboe Mini S&P 500 Index Options (XSP®) have the same notional value as SPY: 1/10th of the S&P 500® Index. For example, if an at-the-money call expiring in two days on SPX costs $3000, the cost would only be $300 for XSP.

For traders looking for an even more affordable choice, there’s an even smaller contract size, Cboe Nanos S&P 500 Index Options (NANOS), which trades at 1/100th the size of XSP, meaning the options are 1/1000th of the cost of SPX.

“I’m worried about early assignment”

Let’s say there are two traders who want to sell a call on the S&P 500 Index. Trader A, an index option trader, sells a call on XSP, and trader B, an ETF option trader, sells a call on SPY. Trader B, the ETF trader, gets assigned early and has shares of SPY called away, but Trader A, the index option trader, never has to worry about early assignment.

Myth: My short options could get assigned at any time.

Fact: With index options, there’s never early assignment or exercise.

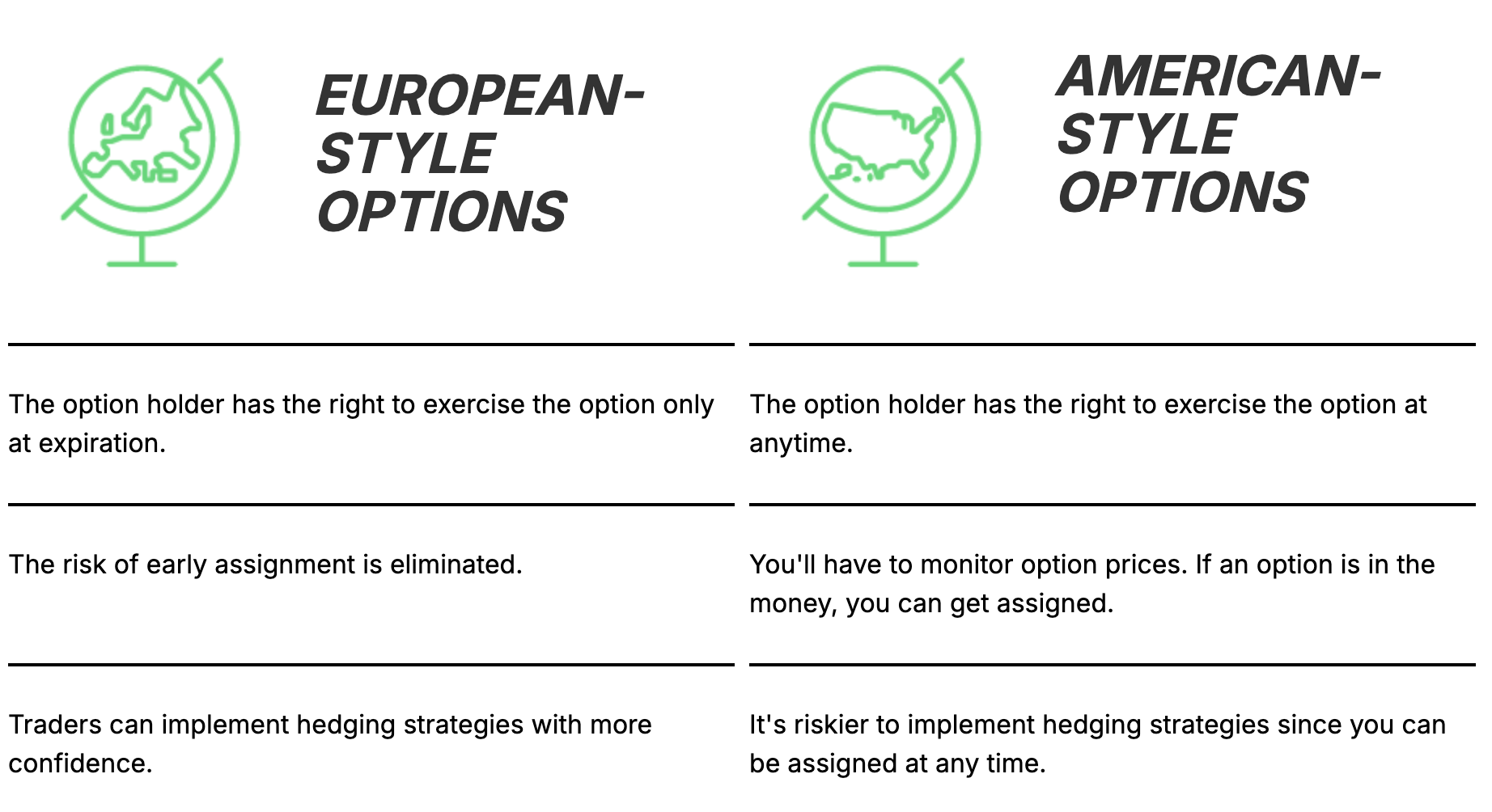

Index options trade European-style, meaning options are exercised only at expiration. Stock and ETF options trade American-style, which means that they can be exercised or assigned at any time before the expiration date.

When selling a call on an ETF or stock option, you could be forced to sell 100 shares any time before expiration, while put sellers of a stock or ETF option could be forced to buy 100 shares at any time before expiration.

For index options, however, you never have to worry about the risk of early exercise or assignment.

Case study: The added benefit of no dividend risk

Stocks and ETFs can receive dividends, whereas indices cannot. Stock or ETF call buyers could choose to exercise their option before expiration to capture the dividend. In the example where Trader B, an ETF trader, sells a call on SPY, it’s possible for Trader B to get their shares called away, or if they don’t own shares of SPY, they might even be subjected to a margin call.

Let’s say that on SPY’s ex-dividend date the call is in the money, and the call buyer chooses to exercise their option so they can own the stock and collect the dividend. This means that Trader B is obligated to sell 100 shares of SPY and pay out the dividend.

On the other hand, trader A, an index option trader, never has to worry about early assignment on XSP. Unlike SPY, XSP can only be exercised or assigned at expiration, so there’s no dividend risk with index options.

“I want to trade options without having to worry about underlying shares”

Unlike equity options, index options are cash settled, meaning profits and losses are settled as a debit or credit deposited directly into your trading account. Stock and ETF options, however, are physically settled, meaning that if an option expires in the money, shares will be delivered to or taken from your account.

Myth: I need to keep a close eye on my long options: if they expire in the money, they’ll be automatically exercised.

Fact: Index options are cash-settled: you never have to worry about managing shares.

With index options, traders don’t have to worry about pin risk or receiving or delivering shares that they don’t want to own or give up.

Case study: Physical delivery versus cash settlement

Let’s say that both the XSP index options trader and the SPY ETF options trader are bullish on the S&P 500 Index, so they buy calls at the 630 strike. On the Friday of expiration, SPY and XSP close at 635. The XSP call buyer is credited with $500 in their account, calculated as the difference between the price at expiration minus the strike times the contract multiplier, or (635-630) x 100.

However, if the SPY call buyer holds through expiration on Friday, on Monday morning, 100 shares of SPY at $630 will be delivered to their account, at a total cost of $63,000 (the strike price x the contract multiplier). Physical delivery could be less favorable if the trader does not want shares of SPY, or if they don't have enough money in their account, resulting in a margin call.

“I want to minimize taxes on my returns”

Unlike stock and ETF options, index options are classified as 1256 contracts by the IRS, which means that potential profits may qualify for 60/40 tax treatment:

60% of gains are taxed at the lower long-term capital gains rate, regardless of the holding period

The remaining 40% are taxed at the short-term rate

Myth: Equity options and index options are taxed the same way.

Fact: Index options are subject to potential special tax treatment.

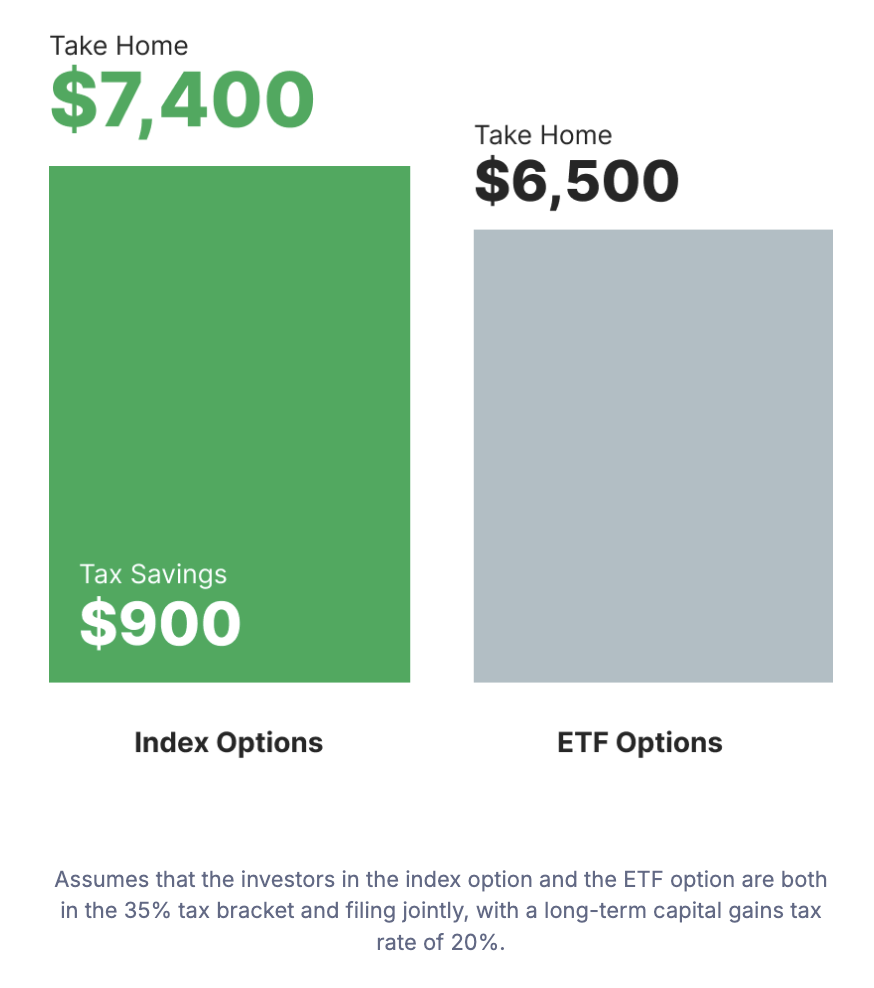

Case study: Favorable tax treatment

Let’s say that Trader A realizes a $10,000 profit on their XSP trade, and Trader B also realizes a $10,000 profit on their SPY option trade. Both traders are in the 35% tax bracket and filing jointly, with a long-term capital gains tax rate of 20%.

Trader A’s $10,000 profit from their index options trade receives 60/40 tax treatment:

$6,000 is taxed at 20% = $1,200

$4,000 is taxed at 35% = $1,400

In total, Trader A will pay $2,600 ($1,200 + $1,400) in taxes.

Trader B’s entire profit from their ETF options trade is taxed at the short-term capital gains rate of 35%, so they’ll pay $3,500 in taxes.

In total, the index options trader will save $900 in taxes.

Still unsure about trading index options?

We’ve just scratched the surface of some of the many ways index options meet retail traders’ needs. For more information, the experts at Cboe have a wealth of resources for options traders, or you can learn more about the index options the Robinhood platform offers for popular market indices like SPX, XSP, NDX, RUT®, and the Cboe Volatility Index (VIX® Index).

Advertiser’s disclosures: There are important risks associated with transacting in any of the Cboe® Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at https://www.cboe.com/us_disclaimers.