US homeowners are more locked in than they’ve been for 40 years

With mortgage rates near 7%, buyers are holding back and sellers are staying put — leaving the housing market frozen.

American homeowners just aren’t ready to sell their properties — not this year, and certainly not at these rates.

A new Bankrate survey found that only 3% of homeowners said they’d be comfortable selling their homes in 2025 at mortgage rates of 6% or higher, a level we’ve been stuck at for almost three years.

Part of the reason, of course, is because people remember the record-low mortgage rates they used to look at during the 2010-21 era, making today’s rates seem high.

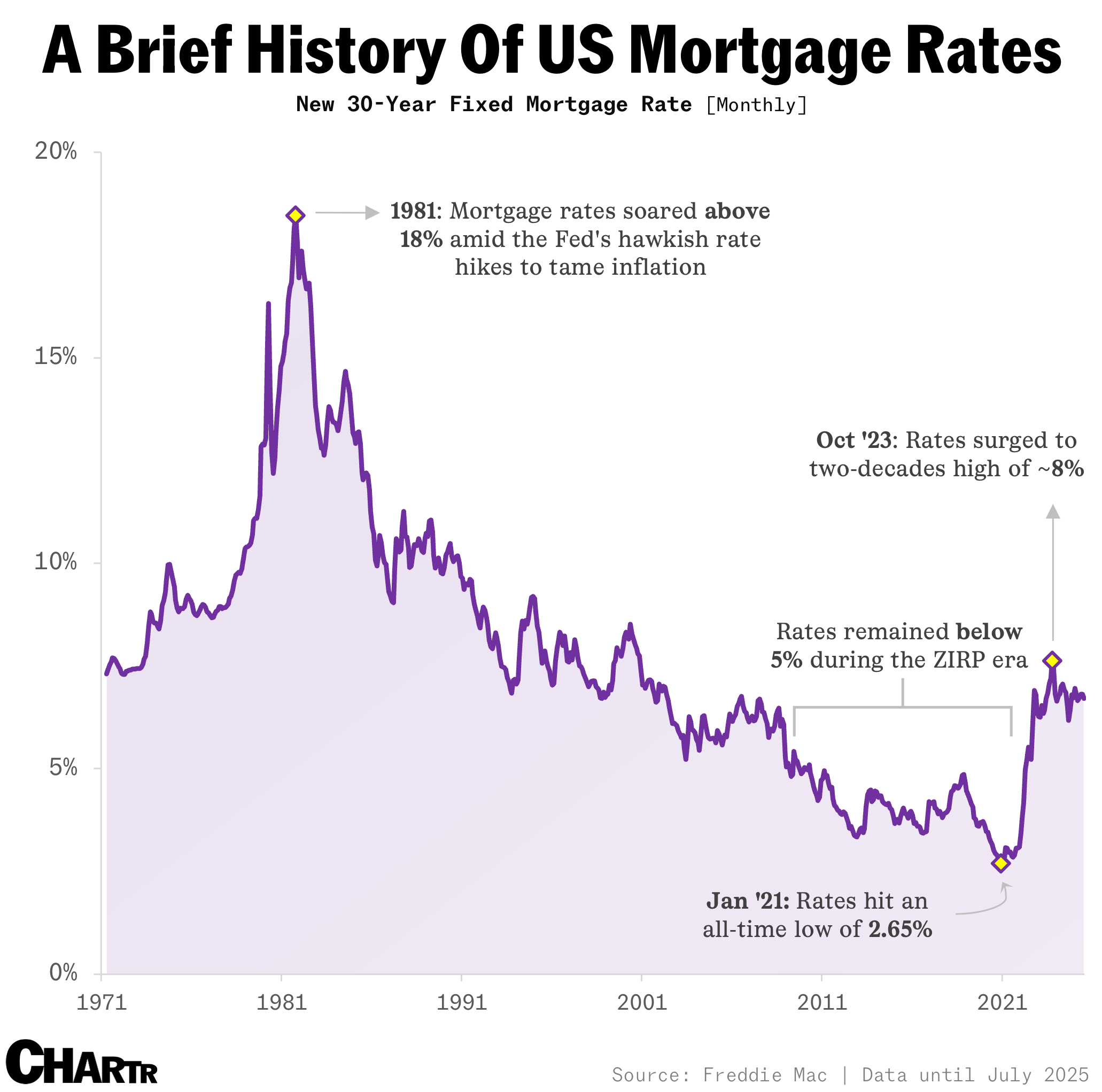

But when you zoom out even further, the ~7% we’ve been hovering at really isn’t all that extreme: mortgage rates soared into double digits in the 1980s amid the Fed's aggressive fight against inflation.

On lock

After a decade of near-zero rates, though, today’s levels still feel like a shock to the system. And clinging on to those pandemic-era bargains, many US homeowners are naturally reluctant to give them up. Per Morgan Stanley housing strategist Jim Egan, two-thirds of outstanding mortgages in the States now have a rate below 4%. Selling now would mean trading those low monthly payments for something far pricier, with today’s 30-year fixed mortgage rates sitting at 6.72%.

The result? A market freeze, as buyers wait for rates to cool while sellers remain anchored to their old mortgages. Last year, existing home sales hit their slowest pace in nearly three decades — and in June, they slipped again to a 10‑month low, stalling the normally busy spring season and dimming hopes for a 2025 recovery.

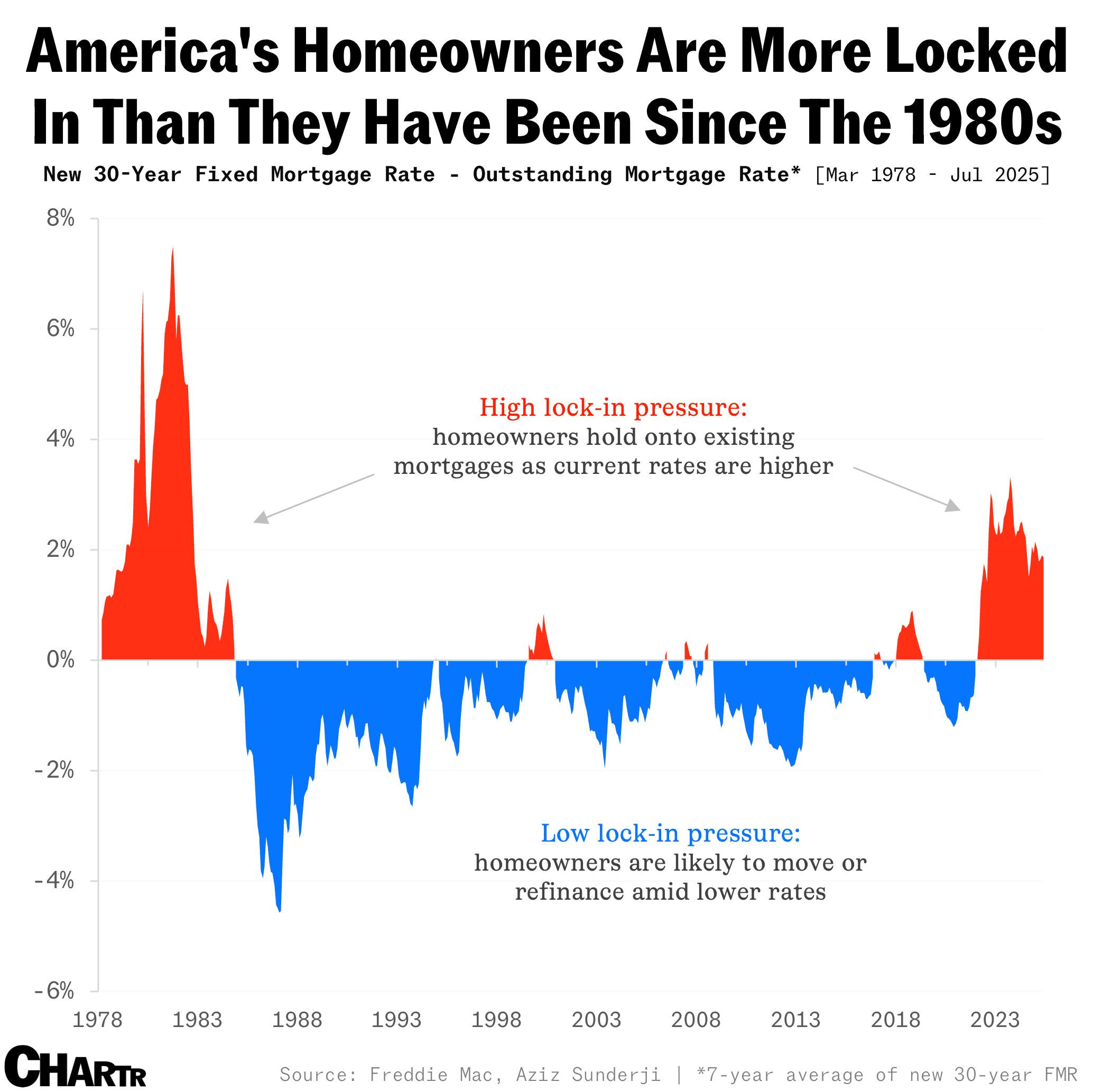

In fact, that housing gridlock is only intensifying, fueled by the worst lock-in effect in more than four decades. According to fascinating analysis from Home Economics founder Aziz Sunderji, the gap between new and existing mortgage rates has grown to about 2 percentage points — the largest since the early 1980s. The bigger the gap, the harder the decision becomes to justify moving or refinancing.

A modest silver lining, though, is that the gulf has started to show signs of shrinking — both nationally and in every state — as mortgage rates have edged slightly lower over the past year, per US News. Still, some states are feeling the squeeze more than the others.

The state with the smallest lock-in gap is Oklahoma, followed by Illinois and Maine — where lock-in gaps are less than 2 percentage points and homeowners may be more willing to give up their current loans. Meanwhile, states with the widest lock-in gaps are Colorado, Oregon, Utah, and Washington, whose existing mortgages are among the lowest in the country.

Even with smaller rate gaps, some states may still feel the sharpest pain... thanks to their sky-high home prices. In Hawaii, trading in an old loan for a new one could add as much as $1,460 to the mortgage per month, while in California, the jump is about $1,356 — a more than 60% increase in both states.