Student loan delinquencies hovered near zero during Covid — but a spike may be coming

With payments due again, nearly 10 million borrowers could fall into default within months.

Federal student loan payments are officially back, and so is the pain.

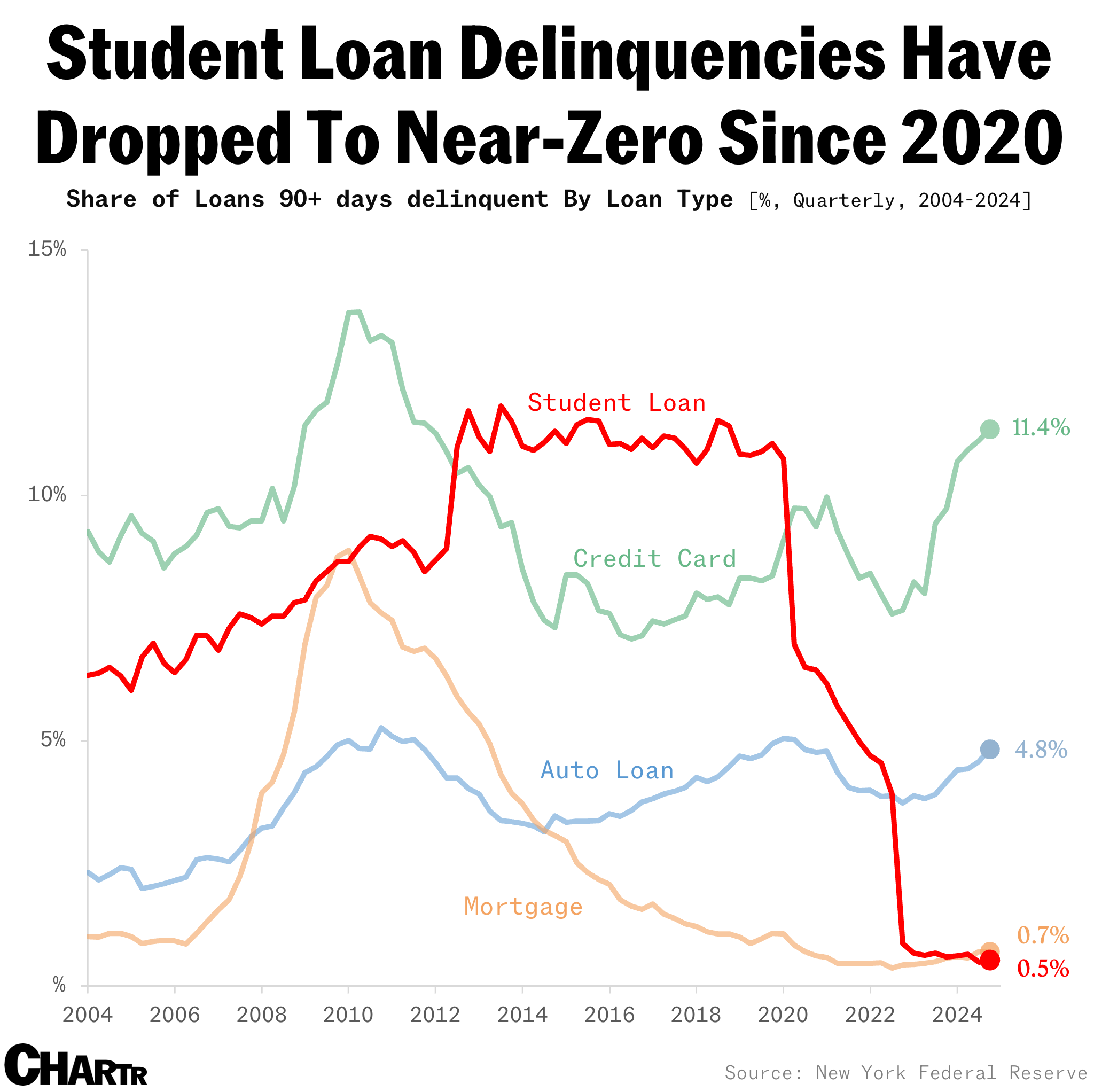

Last week, the US Department of Education resumed collections on 5.3 million borrowers in default — who could now see money taken from their paychecks or tax refunds, if they’re still behind after a 30-day warning. This ends the five-year pandemic pause, which drove the student loan delinquency rate down from 10.8% in Q1 2020 to just 0.5% in Q4 2024, per the New York Fed.

Though it’s usually hard to say with any certainty where lines on charts are heading, in this case, it’s pretty clear: that low rate is about to soar.

In February, 20.5% of student loan borrowers were seriously delinquent (90 days or more past due) — the highest on record, according to TransUnion — after the COVID-19 payment freeze officially ended in September, leaving millions with overdue balances they couldn’t keep up with. Now, the Education Department warns that nearly a quarter of the 42.7 million federal student loan borrowers could default in just a few months. Student loan balances stand at a little over $1.6 trillion, which is more than the $1.2 trillion Americans collectively owe on their credit cards.

And the financial toll of a swath of defaults could be severe: according to the New York Fed, these newly delinquent borrowers could struggle to keep up with their other bills, and they might see their credit scores drop by up to 171 points.

Adding to the situation is President Trump’s push to shut down the Education Department. In March, nearly half of its workforce was laid off, including hundreds from the Federal Student Aid office, which oversees the student loan portfolio. With fewer staff available, borrowers are finding it harder to get help.