Weird Money: Profiting off a bankrupt stock, MrBeast’s new COO, and a GameStop short

How Yellow could become Hertz 2.0, a bankruptcy that actually winds up with shareholders getting paid

Hello hello, and welcome to Weird Money, a new column written by me, Jack Raines. A couple of times a week, I'll discuss the most interesting and, more importantly, weirdest stories I've seen in business and markets. Today is the first column in this series. I hope you enjoy!

Hertz 2.0

Normally, when a company files for bankruptcy, its stock ends up worthless because creditors are repaid first, and there is rarely any cash leftover for shareholders.

Hertz, however, was an exception to the rule. In May 2020, after Hertz filed for bankruptcy, its stock price climbed from 40 cents to $3.70, which, of course, made no sense. But one year later, Hertz reached a deal with private equity firms that would pay shareholders $8 per share, and even the traders who top-ticked the Hertz frenzy at $6.25 the year before looked like geniuses.

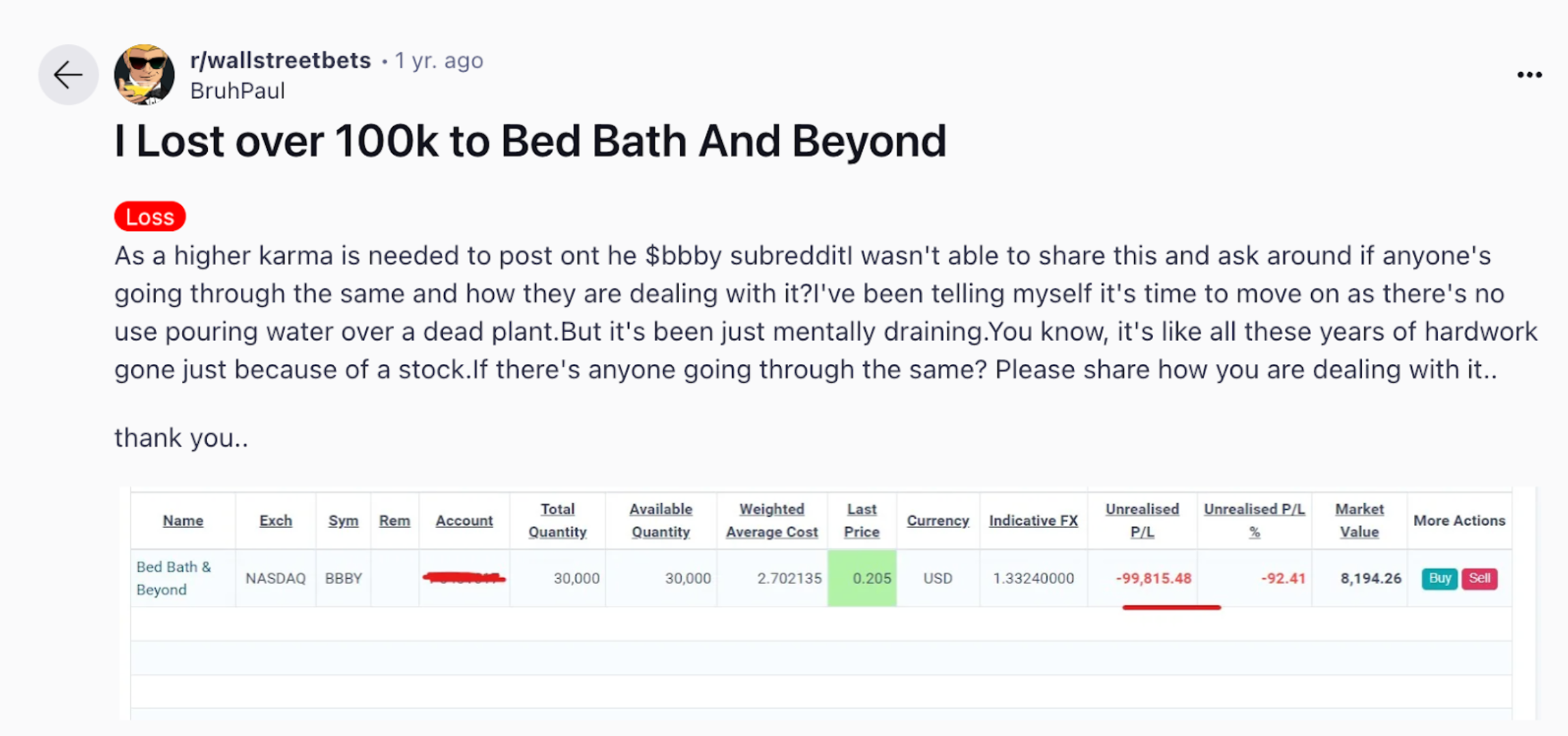

After Hertz, some investors thought,“A really good contrarian investment strategy is probably to buy bankrupt companies because you’ll make a lot of money when they turn around.” And these investors bought Bed Bath & Beyond, which, as most bankrupt stocks do, went to $0.

However, a new bankrupt stock looks like it just might be able to pay its shareholders, too: Yellow Trucking. From Bloomberg yesterday (emphasis ours):

“Defunct cargo hauler Yellow Corp. may put its remaining cargo terminals and other vacant properties into a real estate investment trust that could be used to raise money for creditors, bankruptcy advisers for the company told a judge Monday…

The goal is to find out if the company can raise more cash for creditors by keeping the properties than by liquidating them, (Chief Restructuring Officer) Doheny said. Should the company raise enough money and successfully challenge some of the $10 billion in claims it currently faces, shareholders could wind up collecting something in the case, he said. Normally shareholders are wiped out in big corporate bankruptcy cases.

One option would be to create a real estate investment trust to hold at least some of Yellow’s properties, according to court testimony. The company owns 47 locations and has long-term leases on another 78, testimony and court documents show.”

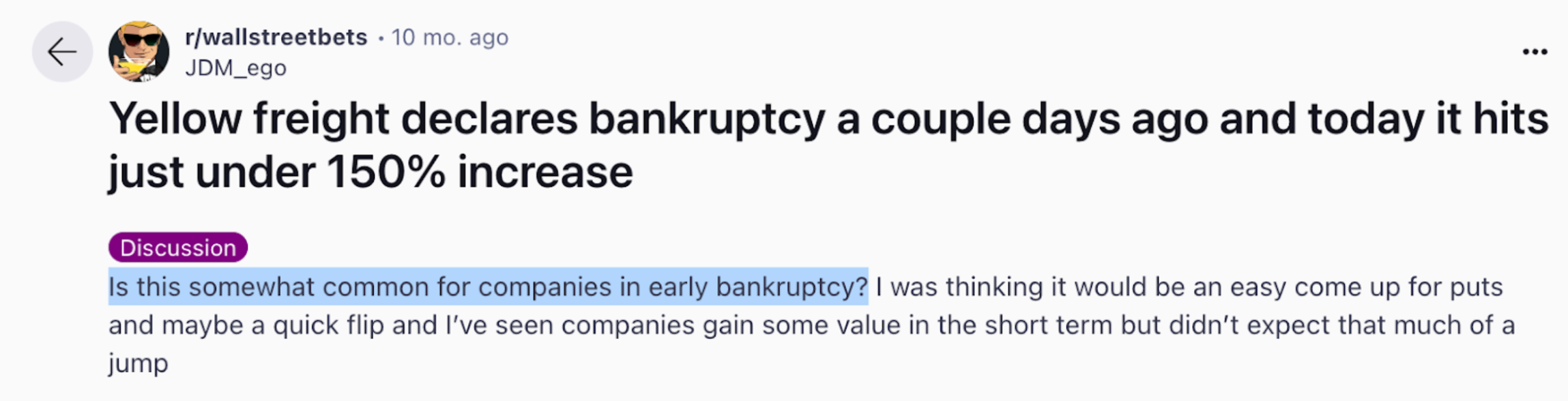

For context, Yellow, formerly one of the nation’s biggest trucking companies, filed for bankruptcy in August 2023. At the time, Yellow was drowning in debt. It had $1.2 billion in loan debt due in fall 2024, including a $700 million Cares Act loan from the federal government and a ~$500 million loan from Apollo (which was later purchased by Citadel). Yellow was also fighting with the Teamsters Union, which represented 22,000 of Yellow’s 30,000 employees, over a missed benefits payment, and the threat of a strike scared customers away, ultimately putting the nail in Yellow’s coffin. Yellow’s stock was delisted from the Nasdaq following its bankruptcy announcement, so, of course, its stock jumped 150%, with one Redditor wondering if it's normal for bankrupt stocks to go up.

At the time of bankruptcy, Yellow stated that it could sell enough real estate and equipment to cover what it owed its secured lenders, as an appraisal of Yellow’s assets showed they were worth $2.1 billion. Multiple bidders, including lender Apollo and trucking companies Jack Cooper and Estes, offered to buy the company for up to $1.5 billion. Yellow rejected the offers, preferring to sell its assets in private auctions, which turned out to be a prescient move, as it has so far sold 128 terminals for $1.88 billion. The company still owns 47 locations and has long-term leases on another 78.

Basically, Yellow sold half of its assets for far more than anyone expected, the proceeds provided plenty of capital for Yellow to repay its secured lenders, and now, demand is so hot for its properties that management is considering rolling the rest of its terminals into a REIT, turning a bankrupt trucking company into a real estate fund. While Yellow is still litigating ~$10 billion of claims, including $7.8 billion in pension fund withdrawal claims, a favorable ruling in bankruptcy court could lead to a fat payday for the investors who threw money at the delisted stock, which is up more than 1000% from its low of 69 cents.

The takeaway from this is not that investors should blindly throw their money at bankrupt stocks, but maybe if the bankrupt stock has yellow-colored vehicles, it’s worth taking a second look? Anyway, keep me posted if Spirit Airlines files for bankruptcy. (Hertz did just hire their CFO, for those curious).

YouTuber COO

If you were a Harvard MBA who had, over the course of his career, been the CEO who took Shutterfly public, served on the board of directors of at least seven publicly traded companies, founded SoftBank’s London’s office, and launched your own venture fund, what would be the next logical move to round out your career? Run for Congress? Buy a professional sports team? How about… “Work for a YouTuber?”

From The Information:

“MrBeast has a new chief operating officer for his holding company: Jeffrey Housenbold, a former SoftBank Vision Fund managing partner who backed companies including DoorDash and took Shutterfly public as CEO in 2006.

Housenbold’s background and new title indicates that MrBeast has high ambitions for his growing business empire, which includes chocolate bar company Feastables. It suggests he could even try to take individual businesses—or his entire holding company—public at some point. Housenbold helped lead the high-profile Vision Fund during a prolific investing spree responsible for some of the firm’s hits as well as misses like e-commerce site Brandless, which later shut down.”

Jeffrey Housenbold has 52 different experiences listed on his LinkedIn, including his MBA summer internship with McDonald’s in 1995, which might give him the most detailed LinkedIn page of all time, so why work for Jimmy Donaldson (aka MrBeast)? Because Donaldson has leveraged his YouTube channel to launch several business ventures, and he has big ambitions about expansion. From Housenbold’s Linkedin post announcing his new role:

Beast Industries is a multifaceted media and entertainment company founded by Jimmy Donaldson, popularly known as MrBeast, the most watched person in the world. Renowned for revolutionizing digital content creation, Beast Industries encompasses a diverse portfolio of ventures that extend far beyond its origins on YouTube. With a mission to entertain, inspire, and create significant social impact, Beast Industries operates across various domains including digital media, philanthropy, consumer products, and innovative business initiatives.

A few years ago, everyone was obsessed with the “creator economy,” and a slew of startups emerged, looking to capitalize on the influx of new creators emerging on the internet. However, it turned out that the market for serving “creators” wasn’t that big, and the real creator economy consisted of a few individuals making almost all of the money. Number one on that list? MrBeast, with the most-subscribed channel on YouTube. While YouTube is still the center of Donaldson’s business, he has parlayed his success to launch his own food company, Feastables, and sign a deal with Amazon. If Jimmy wants to take the “business” of MrBeast to the next level, it makes sense to hire a seasoned operator to run the ship.

Still, I imagine that showing up to the next Harvard Business School reunion as the COO for a YouTuber will draw some weird looks.

Andrew Left Shorted GameStop (Again)

In January 2021, Andrew Left, the founder of Citron Research, said his firm would stop publishing short-seller reports after backlash to his public skepticism about GameStop. From The Wall Street Journal, three years ago:

“For more than a decade, Mr. Left had been well known for attempting to expose fraud at larger companies, publishing lengthy reports and making significant bets that these firms’ shares would decline in value. Among his more well-known calls was a successful bet against Valeant Pharmaceuticals.

But this week, Mr. Left has been the target of ire from stock traders who have come together online to drive up shares of an unlikely momentum stock, mall retailer GameStop. Mr. Left, 50 years old, had been publishing negative reports about the firm in recent weeks.

Some of these traders have shared his personal information, hacked into Mr. Left’s social-media accounts and texted Mr. Left and his two children, using threatening, profane and personal language, according to people close to the matter.

‘The risk-reward of being a short seller is not worth it; it’s not worth it for me or my family,’ Mr. Left said in an interview.”

(For those curious, Left also lost 100% on the trade.)

But this week, the king has returned! Reuters reported yesterday that Left is back, shorting GameStop again. From the Reuters piece:

"’It's fun to go back into the fire. The market dynamics have changed and I'm not as exposed as I was,’ Left told Reuters on his current position in GameStop. ‘The first time, three and a half years ago, (GameStop) was a cultural phenomenon, and that's played out by now. The company has deteriorating financials and is a good short.’”

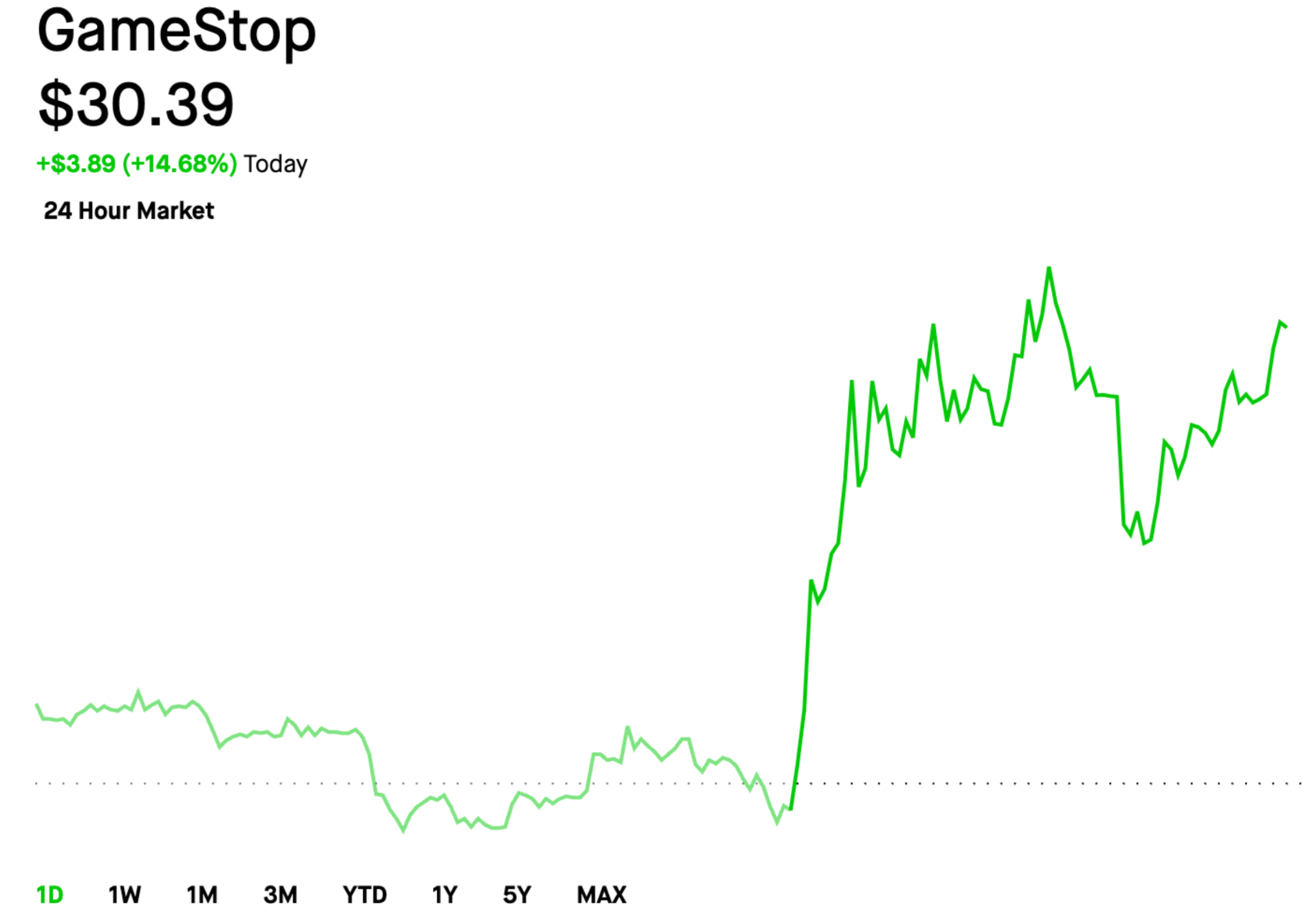

I love this story. Three years ago, a vocal short-seller with decades of experience stated that he was leaving the game for good after getting harassed by retail investors. Now? He’s back, looking for vengeance by shorting the exact same stock that took him out of the game three years ago. The best part? The day after he disclosed his short position, the stock jumped 15% once again.

Remember, markets can, and will, stay irrational longer than you can stay solvent.