With earnings season done, we know what companies are thinking

They want to raise prices. That’s a bad sign for inflation, but also a reminder of why stocks are “the best of all the poor alternatives” for investors when prices surge.

Here’s one big takeaway from the more or less complete Q2 earnings season: Corporate America is trying to pass along rising costs from the Trump administration’s tariffs in the form of higher prices.

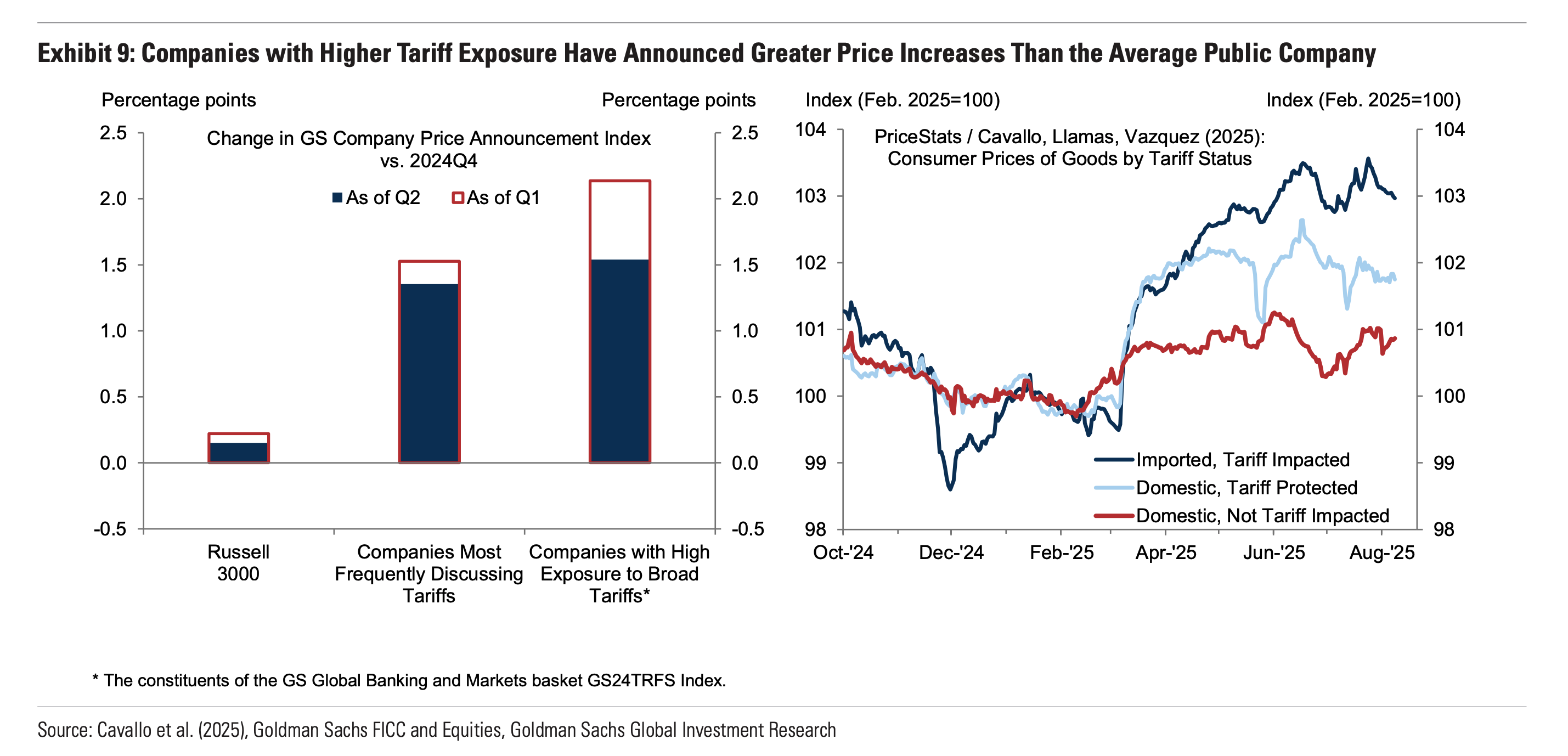

Recent notes from analysts at both Morgan Stanley and Goldman Sachs spotlighted an uptick in chatter about price hikes during the six-week flurry of quarterly reports that essentially concluded yesterday, with AI chip giant Nvidia’s numbers.

“Tariffs have begun to weigh on margins,” wrote Goldman Sachs analysts in a note published this week. “And companies are using a variety of strategies, including renegotiating contracts with suppliers and raising consumer prices, to mitigate the impact.”

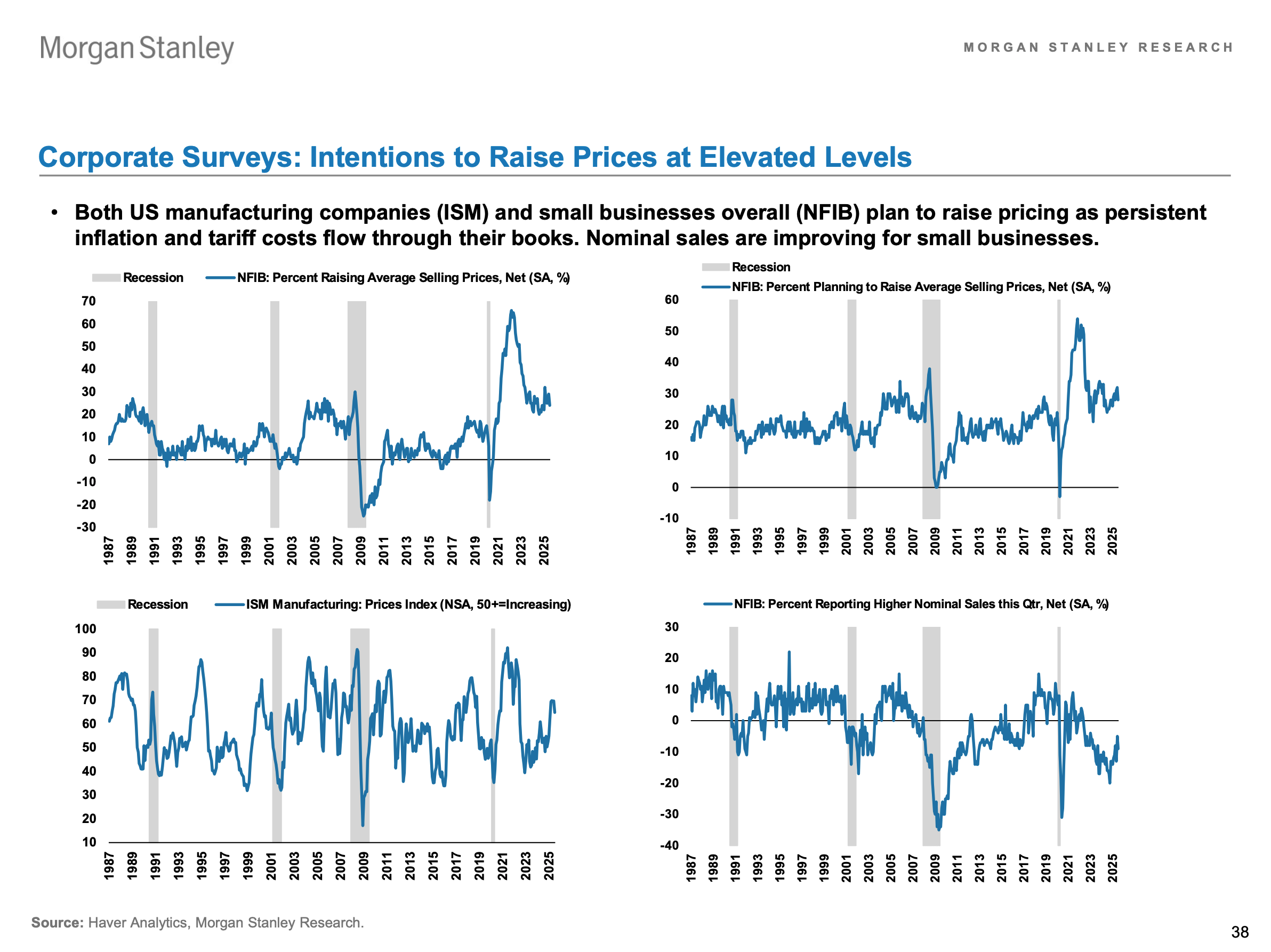

Morgan Stanley market watchers saw the same dynamic at play, writing that during earnings season companies laid out a range of options to offset or reduce the tariff-related costs.

“Corporate America is adapting on multiple fronts (pricing, supply chain, and cost control) to cushion the impact of higher import tariffs,” they wrote. “The full effect is not yet evident and we continue to expect more firmness in goods inflation.”

They also noted that several recent, forward-looking surveys of executives suggest they intend to keep the price increases coming.

As both research shops make clear, price increases aren’t the only tool that companies are using to offset the rising impact of tariffs.

But they are a prominent one, which matters.

It’s another strong piece of evidence that the near mythical tariff-related inflation that economic wonks have been warning about for months — but which has never quite materialized — actually remains a real economic risk.

Producer price index highlights more risk

That’s a similar story to the one told by the most recent report on the producer price index, which measures the prices companies pay their suppliers and is considered a proxy for inflation before it reaches consumers.

When the PPI numbers came out a couple weeks back, they showed showed much higher-than-expected annual PPI inflation of 3.3% in July.

As a result, economists have since raised their expectations for the Fed’s preferred gauge of consumer price inflation in July (due out Friday morning) to 2.9%, nearly a full point above the Fed’s target of 2%.

In short, there’s a lot of evidence out there that inflation risks are building.

At the same time, the Fed, after weeks of attacks on its long-established political independence — including the Trump administration’s current attempt to dismiss key Fed official Lisa Cook — seems all but certain to cut rates at its meeting next month anyway.

(Quick aside: the last time the Fed bowed to clear political pressure like this, it helped fuel the inflationary problems of the early 1970s.)

So, what happens to stocks if we get another inflationary flare-up?

Typically, you’d expect the Fed to start raising interest rates, which tends to provide a gut punch to equity prices. That was the story of 2022, when the S&P 500 dropped 19%.

But in President Trump’s America, with a Federal Reserve potentially taking cues from the White House, it’s less certain that the Fed’s response to high inflation will be typical.

Perhaps the Fed will allow much higher inflation than it has targeted in recent decades, leaving short-term interest rates lower than expected and inflation burning much hotter.

That’s not an ideal backdrop for investment. But in such a world, stocks still might be your best bet.

That’s because owning shares of companies that can actually raise prices provides some protection for investors, and is far better than options like owning bonds or sticking your cash in the bank, where inflation erodes its value.

As a sprightly, 47-year-old Warren Buffett told Fortune magazine back 1977, amid the raging inflation of that era: “Stocks are probably still the best of all the poor alternatives in an era of inflation.”