Uber slides after revenue miss, despite bookings guidance that is above Wall Street’s forecast

Uber’s stock had been on a tear, rising 42% in 2025, but this morning’s earnings revealed a Q1 miss on revenue.

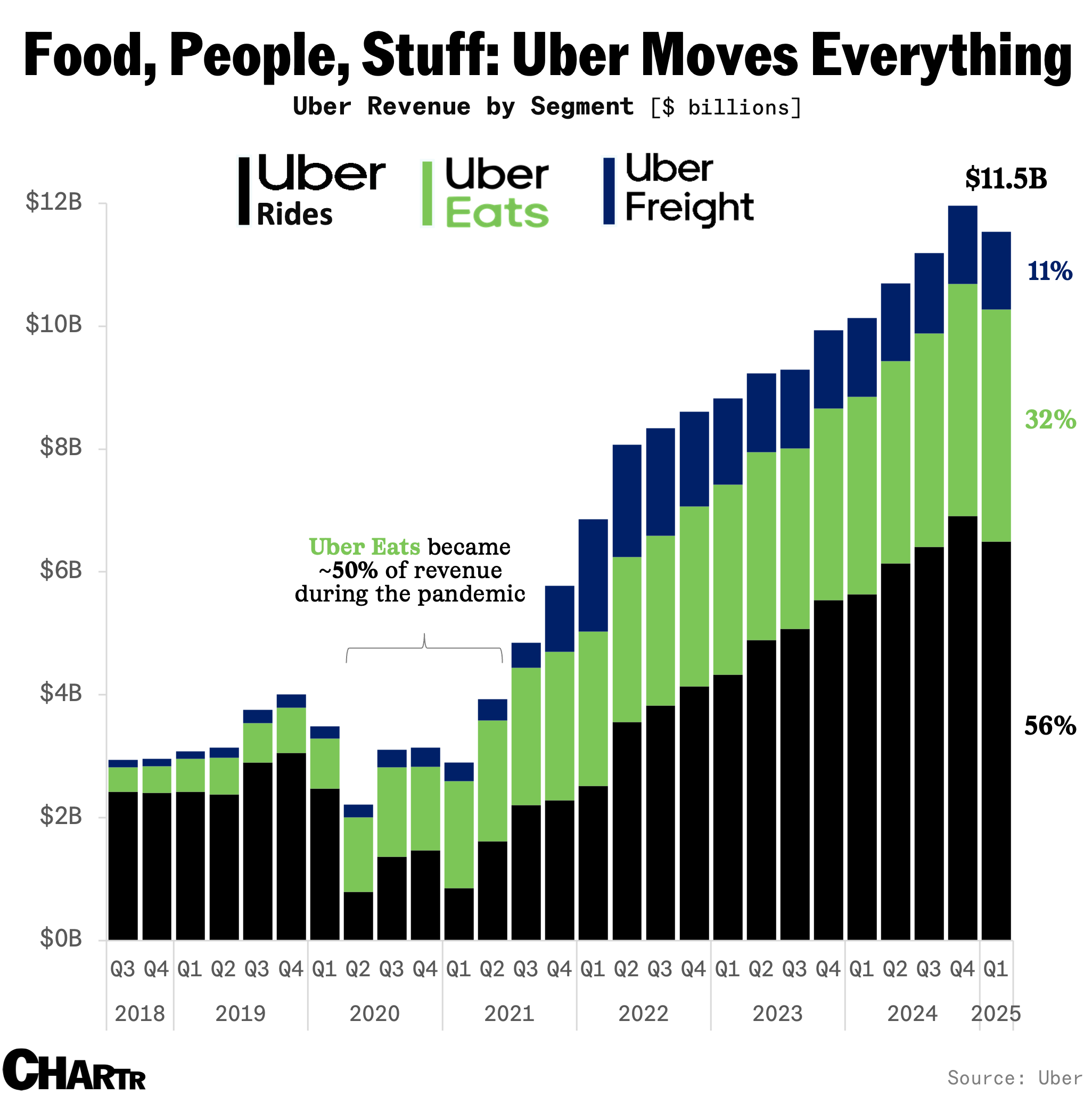

Uber dropped in premarket trading after the company’s Q1 results missed Wall Street estimates, weighed down by tepid ride-share growth. Revenue rose 14% to $11.5 billion, just shy of the $11.6 billion forecast, while operating income of $1.23 billion narrowly beat the $1.22 billion consensus, per FactSet.

Gross bookings — the total spent on rides, deliveries, and freight — climbed 18% to $42.8 billion but fell short of the $43.05 billion target. However, for Q2, Uber projects bookings of $45.75 billion to $47.25 billion, above the $45.8 billion analyst consensus compiled by FactSet.

More than half (56%) of Uber’s revenue still comes from ride-sharing — a segment hit by rising insurance costs, weaker consumer spending, and looming competition from Tesla’s robotaxi push.

To counter these headwinds, Uber is ramping up its autonomous vehicle strategy, which CEO Dara Khosrowshahi called its “single greatest opportunity ahead.” In March, Uber began offering Waymo robotaxis in Austin, where they accounted for 20% of Uber rides that month, with Khosrowshahi also stating that the company has “quickly grown to an annual run-rate of 1.5 million Mobility and Delivery AV trips on Uber's network.”

This month, it announced deals with Chinese AV firms Momenta, WeRide, and Pony.ai to expand robotaxi services across Europe and the Middle East, adding to its 15-plus AV partnerships across ride-hail, delivery, and freight.

Uber is also doubling down on delivery, now 33% of revenue, with a $700 million acquisition of Turkish platform Trendyol Go, aiming to offset cooling North American demand.

Still, with Tesla’s robotaxi launch next month, a fresh FTC probe over subscription, and consumer confidence plunging, whether Uber’s pivot to AVs will pay off remains to be seen.