Traders are bracing for the most volatile earnings season since Covid

Brace for massive swings across America’s biggest companies this reporting period.

To the surprise of no one, this earnings season will be squarely about how companies are navigating an upheaval in trade that is simultaneously not as bad as management teams would have feared a week ago, but much worse than would have been anticipated a month ago.

Confusion still reigns as to what the current realities of cross-border commerce are at this time. As such, there’s a ton of uncertainty over what this all of this means for Corporate America’s near-term future, and the fickleness of the forward outlook is very much reflected in options prices.

Here’s JPMorgan analyst Bram Kaplan:

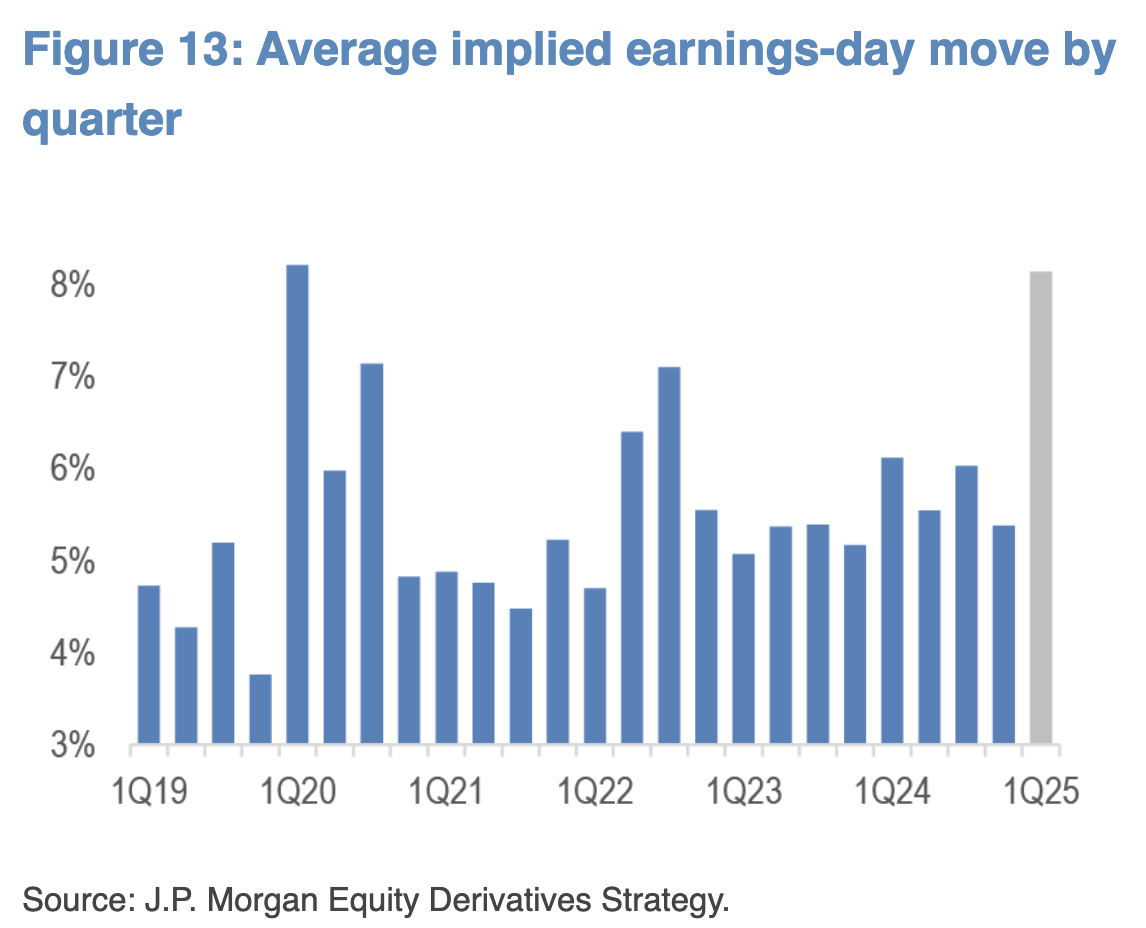

“Given the macro backdrop, unsurprisingly, the options market expects earnings volatility to be well above that delivered in recent quarters on average. The market is pricing in the highest average implied moves since 1Q20 and similar in magnitude to the start of the pandemic, as implied moves also capture some residual volatility from the recent tariff-induced market shocks. The average option implied earnings day move is 8.1% for our universe (Russell 1000 names with liquid options that have yet to report), compared to an average realized move for these names of 6.5% last quarter, and 5.9% on average over the last three years.”

Some of the single stocks with particularly richly priced earnings volatility relative to their three-year average include Eli Lilly, AMD, Apple, and Texas Instruments, according to Kaplan.