The same force that’s made meme stocks crazy is also keeping the stock market from going bonkers

Market volatility is getting suppressed by investors’ love of products that let them be bullish — but not too bullish — on stocks.

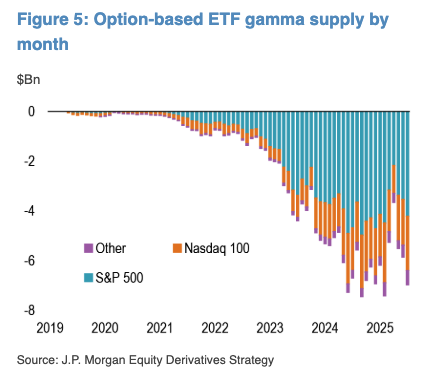

“Gamma supply from option-based ETFs has rebuilt to near-record levels due to continued product growth, declining volatility, and markets’ steady climb,” wrote JPMorgan analysts led by Bram Kaplan. “These products are a key force in the recent suppression of market volatility, in our view.”

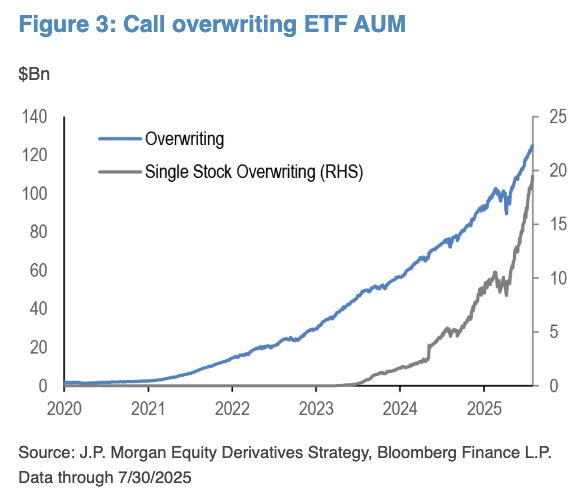

We’ve discussed gamma in the context of options-driven squeezes in single stocks like Opendoor Technologies, but the phenomenon can cut both ways. There are a ton of ETFs that operate as “overwriting funds,” which is to say they own either a broad basket of stocks like the S&P 500 or a single name, like Strategy, and also sell calls to generate income.

It’s the reverse of the call-buying situation: for names where there’s a plethora of call-selling, dealers on the other side of the trade need to sell stock to neutralize their exposure. They will then dynamically manage that exposure by doing the opposite of whatever the index (or stock) is doing.

By pushing against the prevailing action, that means they’re effectively dampening market volatility. Intuitively, option-selling produces the opposite gamma imbalance as option-buying. And assets under management in products that create this effect are soaring, in particular for single stocks where AUM has doubled in about four months, per JPM:

Kaplan says the S&P 500 flipped from a long gamma position (in which it’s tamping down on volatility) to a flat to lightly short position thanks to Friday’s drubbing. That being said...

“We expect option-based ETFs to continue to suppress volatility as long as the market is rangebound or moving higher,” he wrote. “However, they would do little to prevent a vol spike when there is an exogenous shock, since in such an event we can quickly move outside of the range where these strategies are supplying gamma, allowing volatility to surge.”

On the single-stock level, what used to be a “minimal” impact has turned “more significant” in many cases, he added.

For funds that track Strategy, this call overwriting now forces more offsetting activity from dealers than leveraged products, per Kaplan and co.

While the bitcoin treasury juggernaut has the most overwriting AUM tied to it among single stocks (about $5.9 billion), JPM flags Nvidia, Tesla, and Coinbase as the other leaders in the space. Cumulatively, those associated products still have less AUM in their overwriting funds than Strategy!