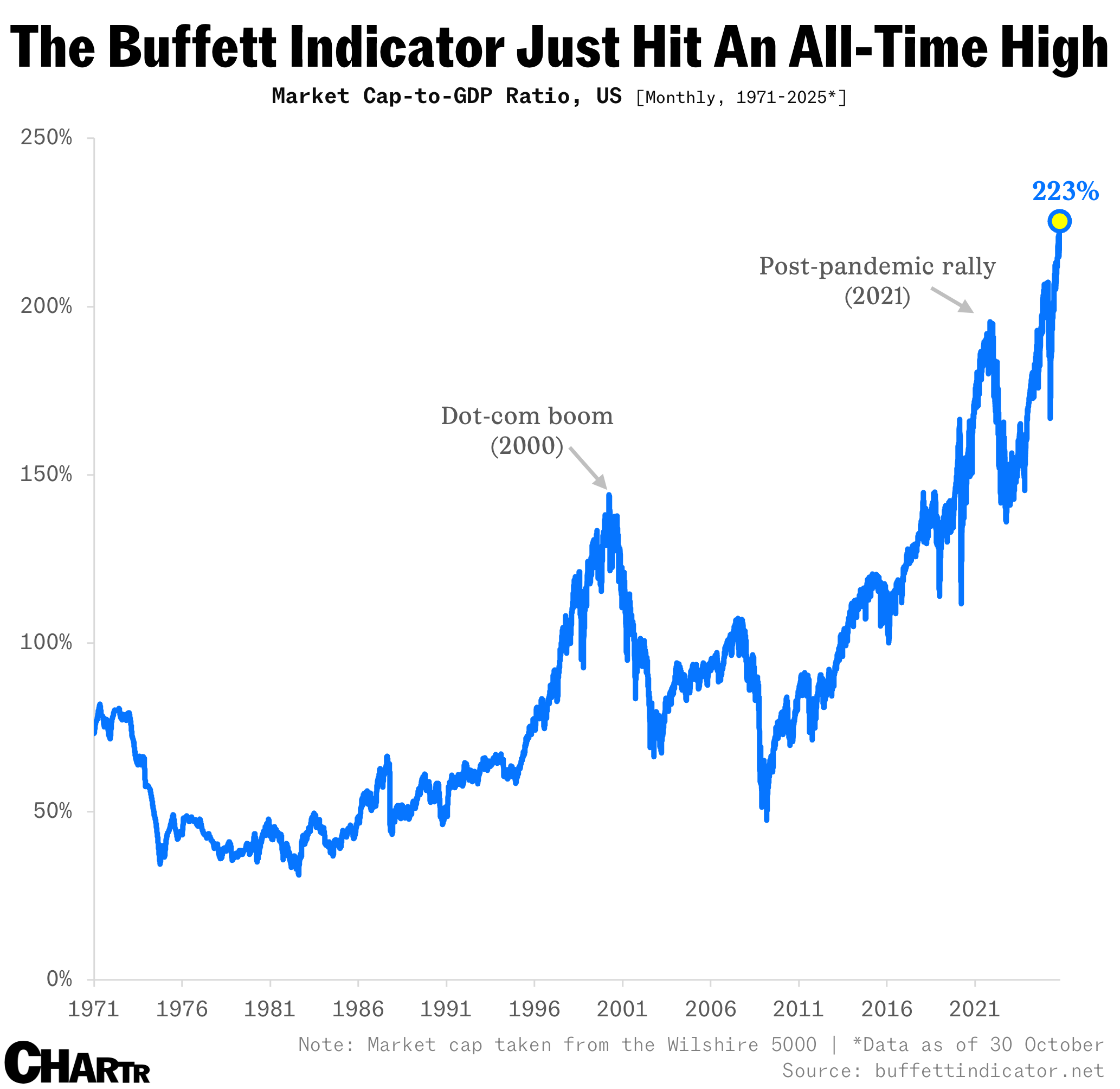

The Buffett Indicator just hit an all-time high

The simplest of all valuation metrics is flashing red; but there are reasons to ignore the alarm.

For most, comparing market caps to the GDP of a country is usually a bit of a no-no. GDP is a flow concept, economic activity over a year; market value, meanwhile, is a stock concept, just a snapshot of all the pieces of paper multiplied by their latest price.

But, as with all other disciplines, once you truly master the rules, you can break them — which is exactly what Warren Buffett did when he popularized the “Buffett Indicator,” the ratio of the total US stock market value to the country’s GDP.

Once hailed by its namesake investor as “probably the best single measure of where valuations stand,” that indicator just hit an alarm-ringing 225% — its highest level on record, adding to the growing chorus of market commentators who think we might be in for a correction.

Time to worry?

Alongside the Buffett Indicator, other metrics are flashing amber or red, too. Investors are paying record prices for every dollar of future S&P 500 revenue, and the market is increasingly concentrated in a handful of megacaps, with eight tech stocks now responsible for ~40% of the S&P 500 Index’s value.

Back in 2001, Buffett warned that the metric nearing 200% would mean “playing with fire.” But, parallel to the valid concerns, there are very legitimate reasons to ignore this particular alarm.

For starters, America’s corporate giants are simply more global than ever — which makes their value look inflated relative to a purely domestic GDP. In fact, nearly half of the Magnificent 7’s revenue comes from overseas, per Goldman Sachs.

Furthermore, today’s corporate giants have never been better at turning revenue into profit, with the S&P 500 enjoying record operating profit margins, north of 14% on a forward basis, the highest ever. That’s why profit-based valuation measures are a little less scary — and they become almost entirely unremarkable once adjusted for future growth. The market’s PEG ratio is in a very typical range, for example (though you have to believe the forecasts, of course, which is a separate discussion altogether).

With that backdrop, throw in a dash of falling interest rates, a sprinkling of finally stable inflation, and an absolute fistful of AI hopes and dreams, and you get the record stock market of 2025 — and a Buffett Indicator of 225%.