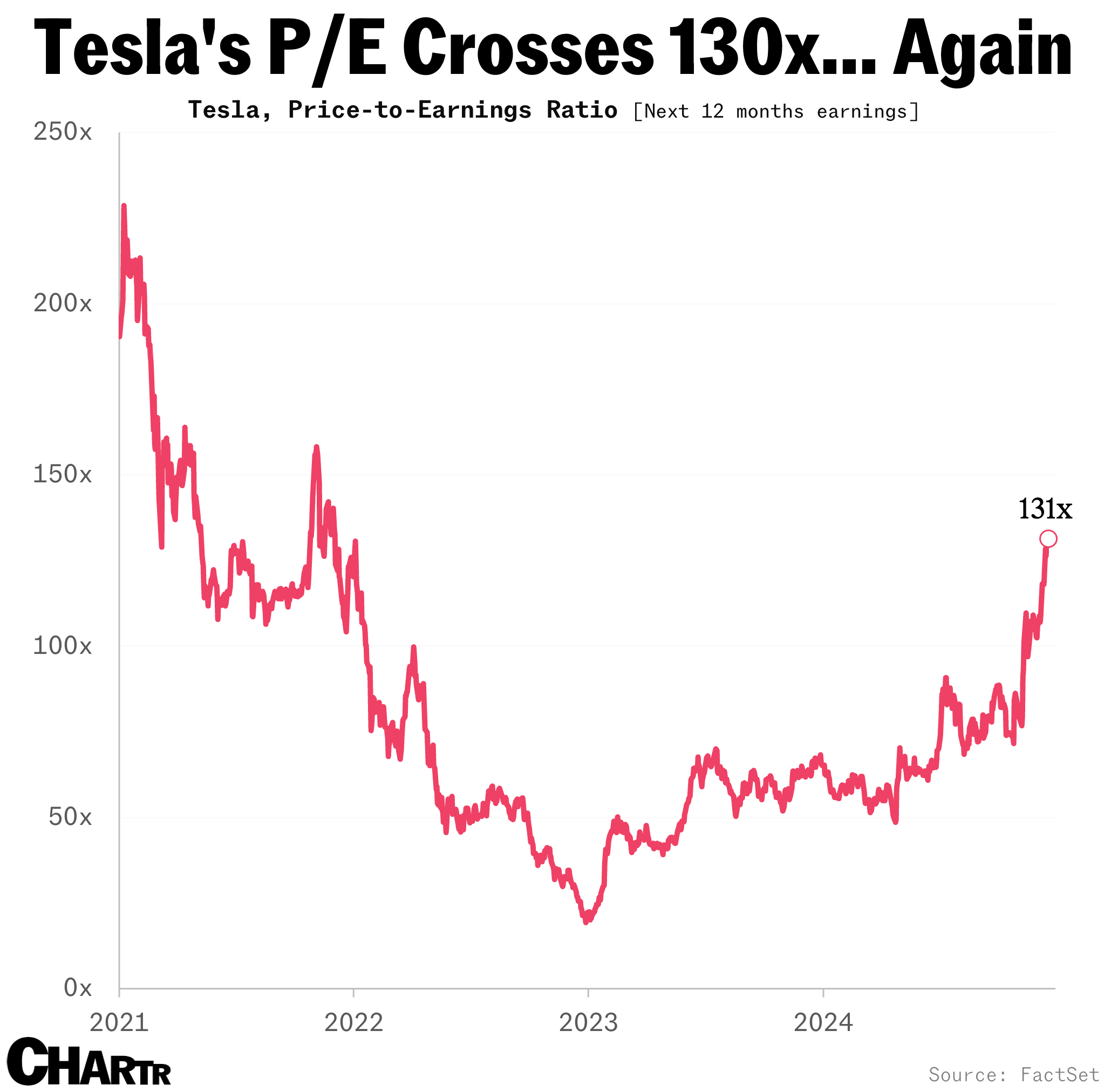

Latest rally takes Tesla’s price-to-earnings ratio over 130x

The world’s most valuable automaker has been riding a postelection wave unlike almost any other company. Since the start of November, Tesla’s stock has risen 75%, taking the company’s market cap north of $1.37 trillion at the time of writing — and making Elon Musk richer than any human being has ever been, with his own personal net worth topping $400 billion.

The enthusiasm among investors to own Tesla, which has seen vehicle-delivery growth grind to a halt this year, has stretched the company’s valuation once again. Per data from FactSet, the company’s price-to-earnings ratio (looking at earnings forecasted over the next 12 months) has hit 131x, the highest figure since late 2021, when the company was just beginning to rack up consistent profits quarter after quarter.

With equity valuations more of an art than a science, Tesla’s valuation has been hotly debated on Wall Street for more than a decade. Those arguing that Tesla is overvalued tend to point to the rest of the automotive industry, which can often trade on single-digit price-to-earnings ratios. Ford, for example, is trading on 6x P/E, and General Motors is on 5x, per FactSet. The counterargument often made is that given its leadership in electric vehicles and investment in autonomous-driving technology, Tesla shouldn’t be valued like a car company, but a tech company — a sector where investors are often happy to invest at triple-digit P/E ratios or in completely unprofitable companies, expecting innovation to drive serious profits in the future.

As we stated earlier this year, the fastest-growing part of Tesla’s business in its latest quarter was its energy-generation and storage division, where revenues rose to nearly $2.4 billion, up 52% year on year.