Tech winners haven’t crushed tech losers by this much since the dot-com bubble was bursting

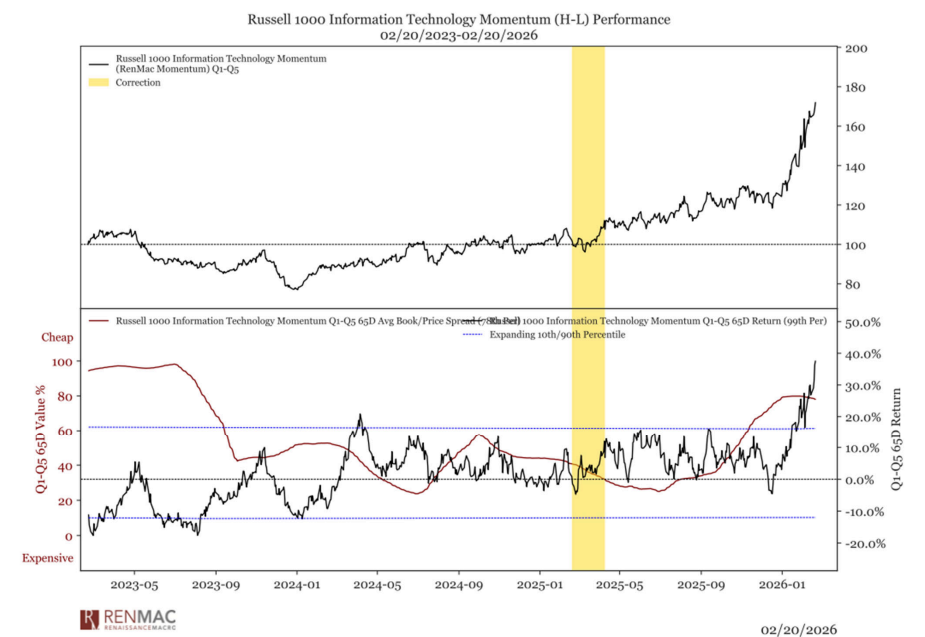

The performance gap between the tech sector’s winners and losers has reached the 100th percentile, widening to levels not seen since 2000.

That’s according to Jeff deGraaf, head of technical research at Renaissance Macro Research, who flagged in a note to clients the magnitude of this divergence in fortunes within the industry.

The story of the technology trade in 2026 was made clear on the first trading day of the year, with a record outperformance of semiconductor stocks versus their software counterparts.

Since then, software has continued to flounder as new AI tools pull the timetable for potential disruption forward and threaten to undermine the perceived safety of the software industry’s recurring revenue streams and margins. Within the hardware space, the list of winners have become even narrower, with investors focused on data center capex beneficiaries, particularly in memory and semicap equipment.

“To see similar levels of performance differential between winners and losers requires a trip back to 2000 as the dot-com bubble was bursting and the semis were holding up relative to the speculative internet related names,” deGraaf wrote. “Beware chasing good charts in technology, and at the margin, reduce exposure.”

Year to date, the best performers in the Russell 1000 Technology Index (and presumably, the best charts) include Sandisk, Western Digital, Corning, Vertiv Holdings, Micron, and Applied Materials.