Stocks are sinking today — it’s surely the GDP numbers and not the fact that it’s the last day of April

It’s definitely not investors getting a jump start on “sell in May and go away.” Right?

After weeks of good news being bad and bad news being good for the stock market, this morning appears to be one of those rare days when market participants of all levels of sophistication get to say the rarest of phrases: I know why the market is doing what it’s doing.

Indeed, the cause of today’s market malaise, with the SPDR S&P 500 Trust Index still in the red despite staging a mini midmorning rally, seems easy to diagnose. As my colleague Luke Kawa put it:

“US stocks are sliding in early trading after the Bureau of Economic Analysis reported that the advance estimate of first-quarter GDP showed a 0.3% contraction in the economy compared to Q4.”

But, to quote Michael Scott, “I’m not super-stitious but I am a little stitious.” And today’s downturn in US stock markets just happens to come on the last trading day of April, giving ammunition to the small group of investors who espouse the old stock market adage that you should “sell in May and go away.”

As someone who typically puts as much faith in stock market voodoo as I put in my own ability to time the market (none), I’m hesitant to write about seasonal patterns. Though it might only be a very distant cousin of technical strategies like the “Inverse Head and Shoulders Pattern,” the “Broadening Bottom,” or the “Quasimodo Pattern,” the notion that what month it is matters is hard to swallow. But swallow it we must, because there is a substantial body of evidence confirming the fact that stock market returns tend to lag over May and the summer period that follows.

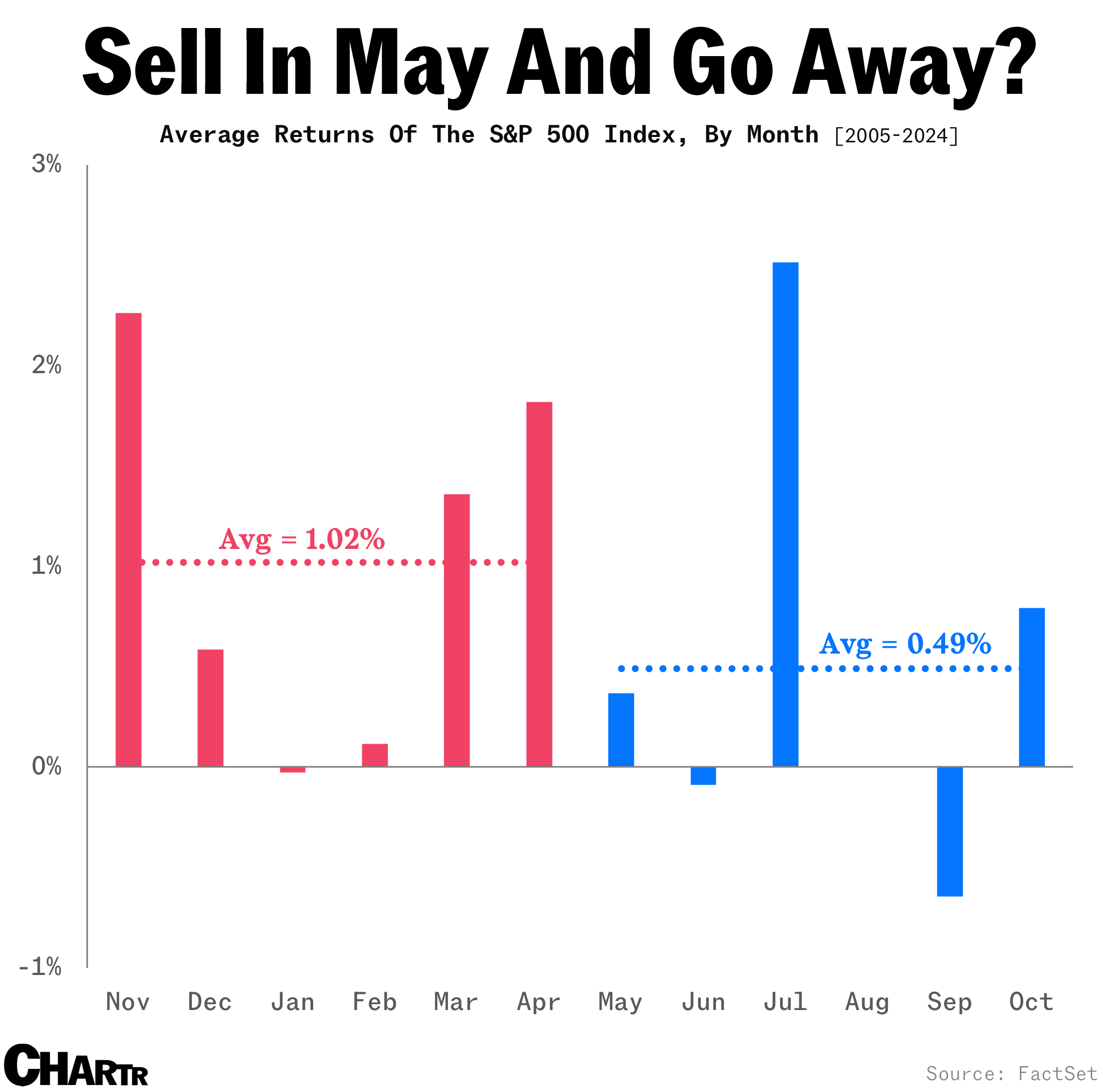

Per Fidelity’s research (emphasis ours):

“Since 1990, the S&P 500 has gained an average of about 2% from May through October. That compares with a roughly 7% average gain from November through April.”

It’s hard to tell at a glance, but even on a shorter, more modern time horizon, the monthly returns for the six-month period from the start of November to the end of April have averaged around 1%, while the May to October six-month swing has produced roughly half the returns, at 0.5%.

So, yeah, today’s downturn is almost certainly just the GDP numbers, tariff jitters, and the latest saga in the AI trade. But maybe — just maybe — there are a few folks out there hitting the sell button who are heading to a beach for the next six months. If that’s you, please get in touch.