Steve Ballmer now richer than Bill Gates via time-honored strategy of refusing to diversify his holdings

“Diversification is for losers” - Steve Ballmer, probably

In August 2014, Microsoft’s founder, Bill Gates, was worth approximately $78 billion. Meanwhile, Microsoft’s 30th employee-turned-CEO, Steve Ballmer, who was about to be replaced by Satya Nadella, was worth $20 billion.

In July 2024, Microsoft’s founder, Bill Gates, is worth $157 billion. Meanwhile, Microsoft’s 30th employee-turned-former CEO, Steve Ballmer, is worth slightly more than $157 billion, passing the company’s founder in net worth. How? While Gates diversified his wealth across several different investments and pledged to give away billions in philanthropic donations, Ballmer continued to YOLO Microsoft stock.

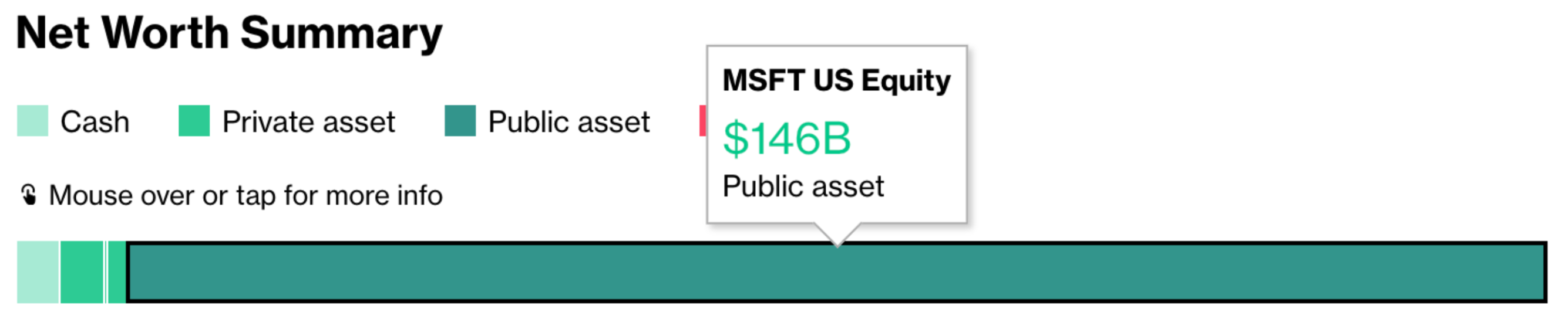

Bloomberg’s Billionaires Index tracks the portfolio’s of the world’s richest individuals, and 10 years after stepping down as CEO, more than 90% of Ballmer’s $157 billion is still invested in Microsoft stock. The rest is a few billion cash, as well as his stake in the Los Angeles Clippers and the team’s arena.

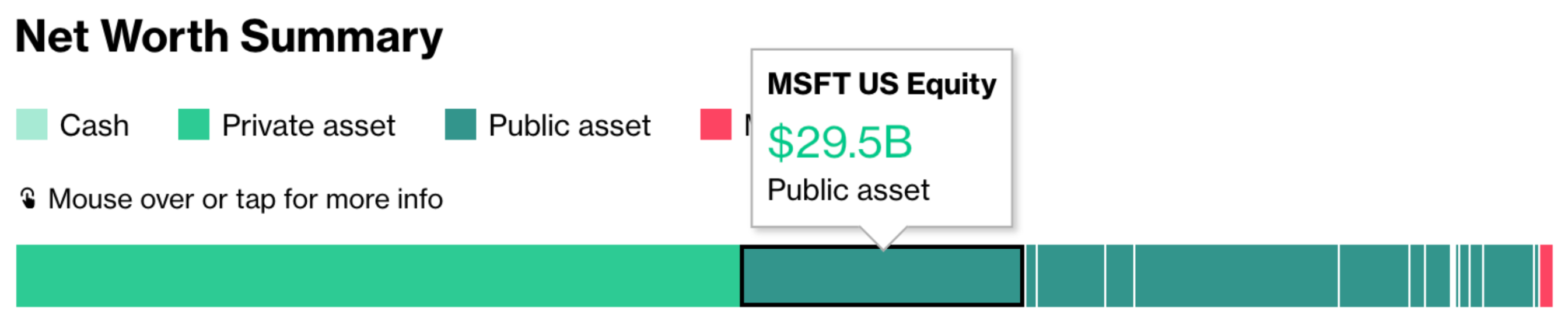

Compare this to Gates’ more diversified portfolio, which includes a $75 billion stake in his private investment firm, Cascade Investment, and just ~$30 billion in Microsoft.

I love Ballmer’s refusal to invest in anything (other than a professional basketball team, of course) except for Microsoft’s stock. He won’t even sign Bill Gates’ Giving Pledge! Most people would, from a risk management standpoint if nothing else, diversify their investments at $20 billion, especially if they had just been replaced as the CEO, right? But Ballmer went all-in on the man who replaced him, making $137 billion in the process. I guess the takeaway here is that if someone is good enough to take your job as CEO, they’re good enough to invest in.