OpenAI doesn’t have the cash to pay Oracle $300 billion — raising it will test the very limits of private markets

The ChatGPT maker plans to burn though $115 billion by 2029. No company in history has ever lit that much money on fire intentionally, let alone tried funding such a splurge through private markets alone.

There’s a playbook in Silicon Valley: raise some money; build something people want; raise a lot more money; burn it in the pursuit of growth. The core of this strategy is to swap money for time by acquiring talent, companies, infrastructure, and technologies, all in the pursuit of leapfrogging your competition in the burgeoning field you’re disrupting.

Then, if you’re successful in ascending to the top: kick back, up your prices, and rake in the billions.

From Uber to Amazon, Tesla to Facebook, this game plan has worked time and time again. Jokes on late-night talk shows about companies losing money year after year, or paying a billion dollars for then boutique apps like Instagram, have become unfunny fast, as Big Tech has swallowed advertising, apparel, and everything in between.

In the last few weeks, major deals with Broadcom and Oracle have thrown into sharp relief just how insane OpenAI’s ambitions are. The Oracle deal alone is worth $300 billion over five years starting in 2027. OpenAI does not have that kind of cash.

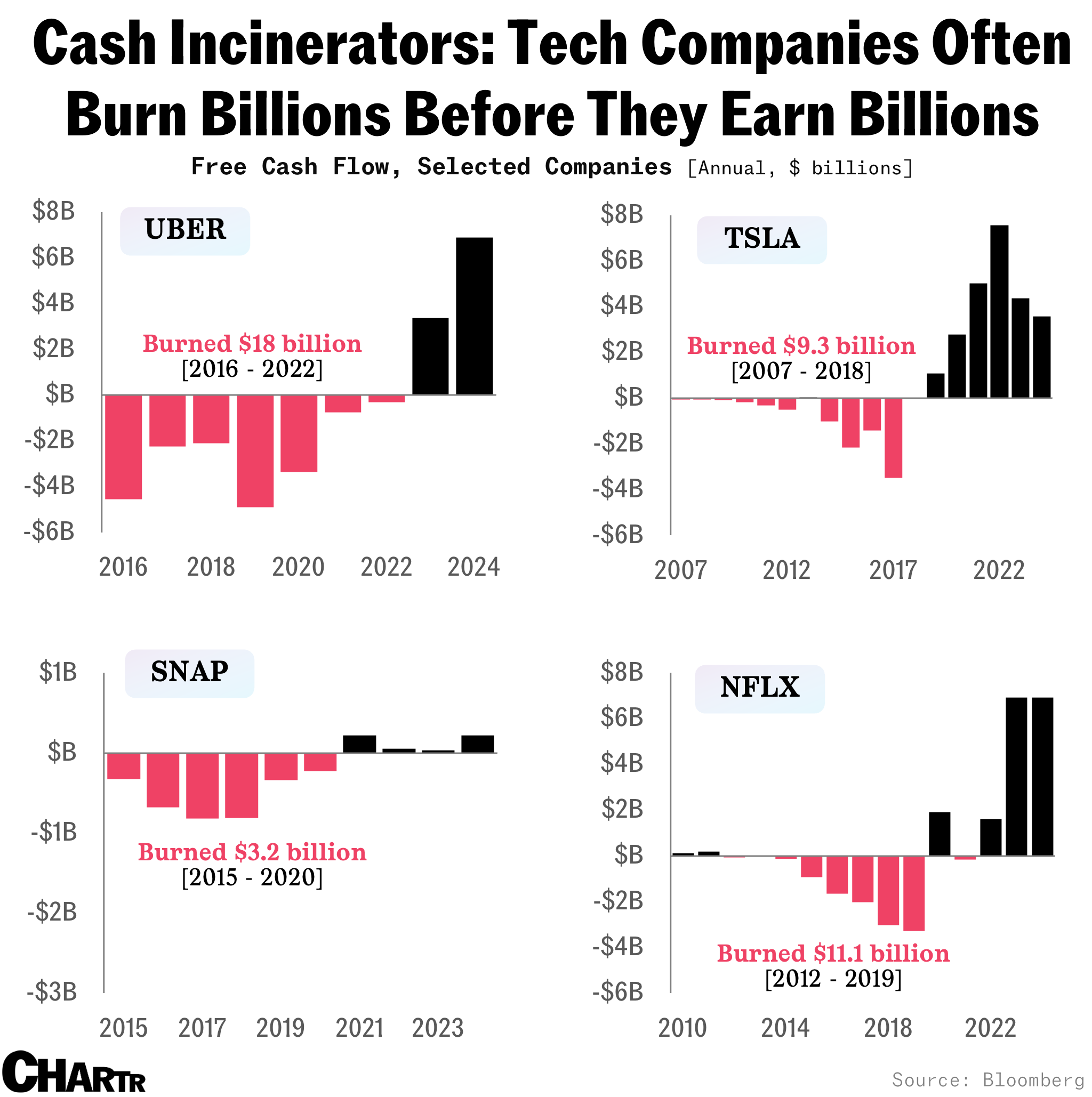

In fact, four of the tech world’s big “cash incinerators” — Uber, Tesla, Snap, and Netflix — together burned a pathetic ~$42 billion during their respective heavily cash-burning periods.

Per The Information, OpenAI is planning on burning $115 billion through 2029. Given that the company raised “only” $40 billion earlier this year — and $64 billion in its lifetime to date, per Pitchbook data — it’s fair to assume that OpenAI will have to dip into the capital markets again to raise another $50 billion to $75 billion to fund its spending splurge.

And OpenAI’s funding needs might not stop there — after that monstrous 2029 spending figure is reached, the company could still be on the hook for hundreds of billions of dollars as part of the freshly inked deal with Oracle, which runs for five years and only starts in 2027.

We’re going to need a bigger cap table

Just a few years ago, the idea of raising that amount on the deeply liquid public markets would have been remarkable; the biggest IPO ever was 2014’s Alibaba, which raised $25 billion — a figure that might not cover even a single year of OpenAI’s peak cash burn. Doing it in private markets would have been near unthinkable. Doing it as a complicated entity controlled by a “not-for-profit” entity? Insane.

Last week, the company revealed it had made progress on that last point. The Financial Times reported that OpenAI and Microsoft had signed a “non-binding memorandum of understanding” marking “a significant step forward in the start-up’s effort to convert to a more investor-friendly, for-profit structure.” That could unlock a potential IPO, giving institutional and retail investors the ability to invest directly in the company.

But in August, CEO Sam Altman said that an IPO was not a priority, suggesting there’s a very good chance that OpenAI continues to fund its runway via the private scene.

If the company pulls it off — raises all that money and finds a way to make the unit economics of its chatbot work along the way — it will raise a major question: is the stock market doing its primary job? If the most capital-hungry business of all time doesn’t need to raise on the public markets, we may need to rethink our textbook definitions of the stock market. The capital-allocating conduit that’s been the bedrock of American capitalism for more than a century is increasingly about price discovery, liquidity, and risk transfer, and less about capital formation.

What’s most remarkable, though, is that this might be quite an easy feat for OpenAI. Given the pervasive AI mania that we find ourselves experiencing in 2025, it’s hard to imagine that the world’s leading consumer-facing AI company will struggle to find investors for its cap table in the private markets, even at a nosebleed valuation of $500 billion and even with evidence that AI adoption might be cooling.

Related reading: Where did all the stocks go?