Morgan Stanley: Don’t fight the rally, here’s why

Morgan Stanley’s chief US equity analyst, Mike Wilson, is out with a fresh note taking a look at one of his favorite fundamental indicators for the market.

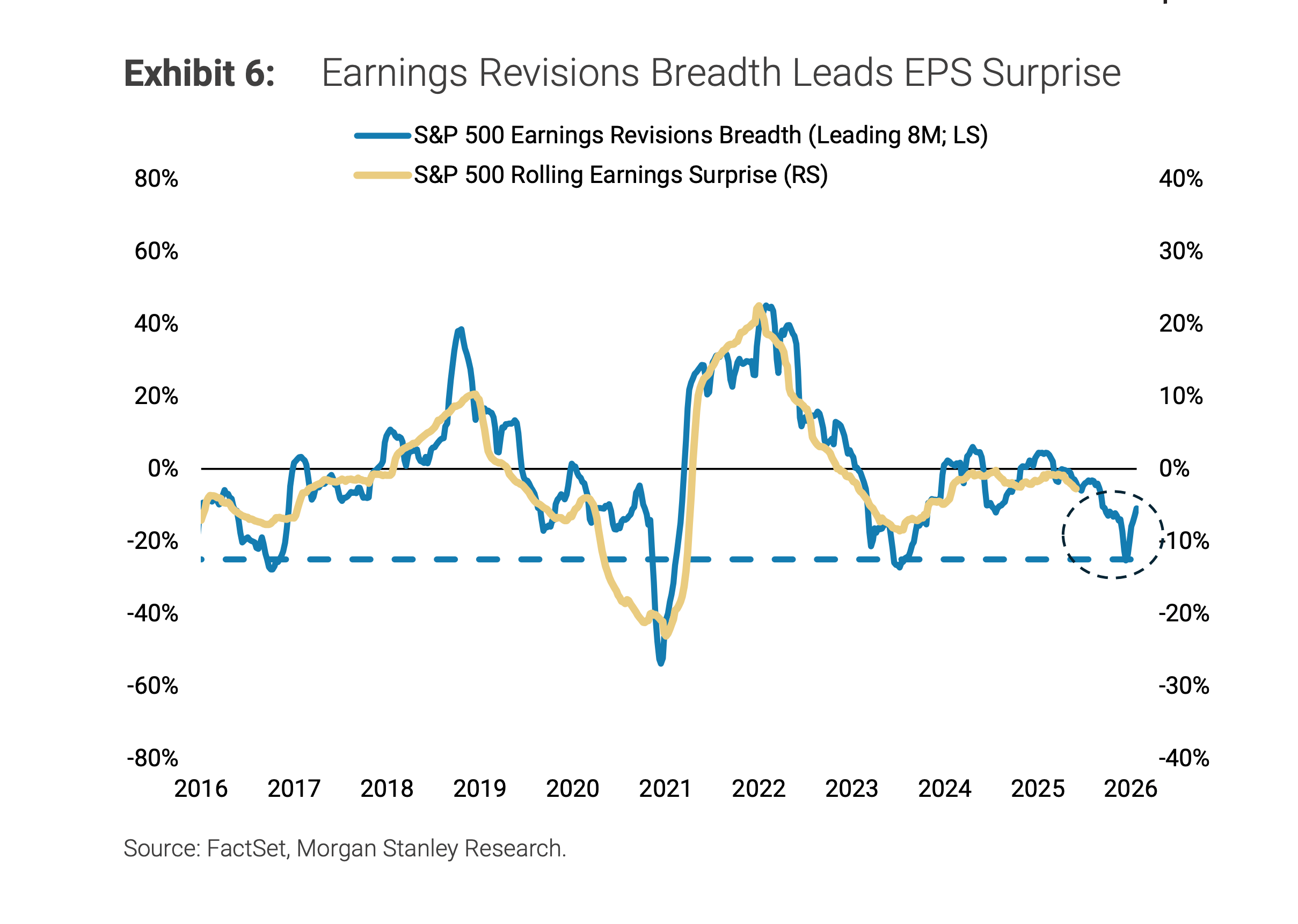

It’s the bank’s somewhat idiosyncratic measure of analyst earnings expectations for S&P 500 (SPDR S&P 500 ETF) companies.

It’s a bit of a complicated, triple bank shot, meta-derivative he calls the “rate of change on earnings revisions breadth.” But for our purposes, just think about it as the short-term trend in the share of analysts who are lifting or lowering their expectations for S&P 500 earnings per share. Here it is:

Wilson wrote:

“Earnings revisions breadth troughed two weeks after Liberation Day and the beginning of the re-acceleration in this gauge coincided with Microsoft Q1 earnings release... In our experience, when revisions breadth is accelerating in a V-shaped manner from an extreme low, equity markets typically remain supported and pullbacks remain shallow and unsatisfying (like the past 6 weeks).”

In other words, while there’s still a lot of uncertainty out there about the longer-term impact of President Trump’s tariffs on the US economy and corporate profits, the markets are increasingly looking past it, setting the stage for better-than-expected earnings results in the coming quarters.

We’re seeing some of this dynamic play out today, as companies like Boeing, Carnival, and JPMorgan Chase are all seeing analysts pencil in higher full-year 2025 EPS expectations.

Such a trend helps explain the S&P 500’s roughly 20% rally off its April bottom for the blue chips, which pulled the market to within 2% of a new all-time high for stocks.

It’s a bit of a complicated, triple bank shot, meta-derivative he calls the “rate of change on earnings revisions breadth.” But for our purposes, just think about it as the short-term trend in the share of analysts who are lifting or lowering their expectations for S&P 500 earnings per share. Here it is:

Wilson wrote:

“Earnings revisions breadth troughed two weeks after Liberation Day and the beginning of the re-acceleration in this gauge coincided with Microsoft Q1 earnings release... In our experience, when revisions breadth is accelerating in a V-shaped manner from an extreme low, equity markets typically remain supported and pullbacks remain shallow and unsatisfying (like the past 6 weeks).”

In other words, while there’s still a lot of uncertainty out there about the longer-term impact of President Trump’s tariffs on the US economy and corporate profits, the markets are increasingly looking past it, setting the stage for better-than-expected earnings results in the coming quarters.

We’re seeing some of this dynamic play out today, as companies like Boeing, Carnival, and JPMorgan Chase are all seeing analysts pencil in higher full-year 2025 EPS expectations.

Such a trend helps explain the S&P 500’s roughly 20% rally off its April bottom for the blue chips, which pulled the market to within 2% of a new all-time high for stocks.