Morgan Stanley counts Amazon’s data center square footage to explain why its cloud business will boom

The second-quarter reporting period showed that competitors have been making up ground on Amazon in a key AI battleground among tech giants: their cloud businesses.

Amazon Web Services’ revenues rose 17.5% year on year in Q2, trailing growth of 31% for Alphabet’s Google Cloud and 39% from Microsoft’s Azure. Granted, AWS is still the leader in the cloud, but its slow growth versus rivals was a sore spot for investors after earnings — especially after CEO Andy Jassy fumbled his way through an answer on the subject.

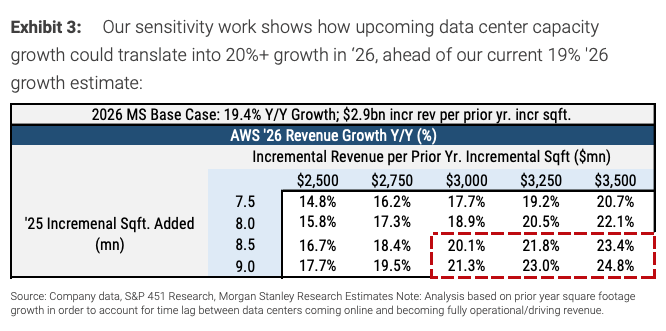

Amazon Web Services had a $195 billion backlog as of June 30, and turning those would-be orders into actual cash requires time and/or increased capacity. Morgan Stanley analysts led by Brian Nowak have a framework for assessing how Amazon aims to maintain its dominant footprint in the cloud business: by literally counting up expected data center square footage.

“Our analysis of AWS expected forward square footage (analyzing S&P 451 Research DataCenter KnowledgeBase and company filings) speaks to how AWS potentially has ~8.5 million/~10 million of data center square feet coming online in ’25/’26. This would be similar to annual square footage added in ’24 and ahead (in some cases significantly ahead) of prior periods,” they wrote. “This expected square footage growth combined with AWS’s ~$3.5 billion historical median incremental revenue per prior year incremental square foot leads to our sensitivity below showing how upcoming data center capacity growth could translate into 20%+ AWS revenue growth in ’26.”

However, this analysis also comes with a large caveat attached:

“We acknowledge there are sources of volatility and (ongoing) constraints around incremental revenue per incremental square feet analyses — component supply constraints like chips, racks, cables, boards, power, and demand differences like client readiness and products to drive adoption, product pricing, and yield per foot, etc. — but we think this framework is helpful in showcasing how AWS is investing to match demand and drive accelerating growth in the early innings of the GenAI era.”

Nowak has an “overweight” rating and $300 price target on Amazon.