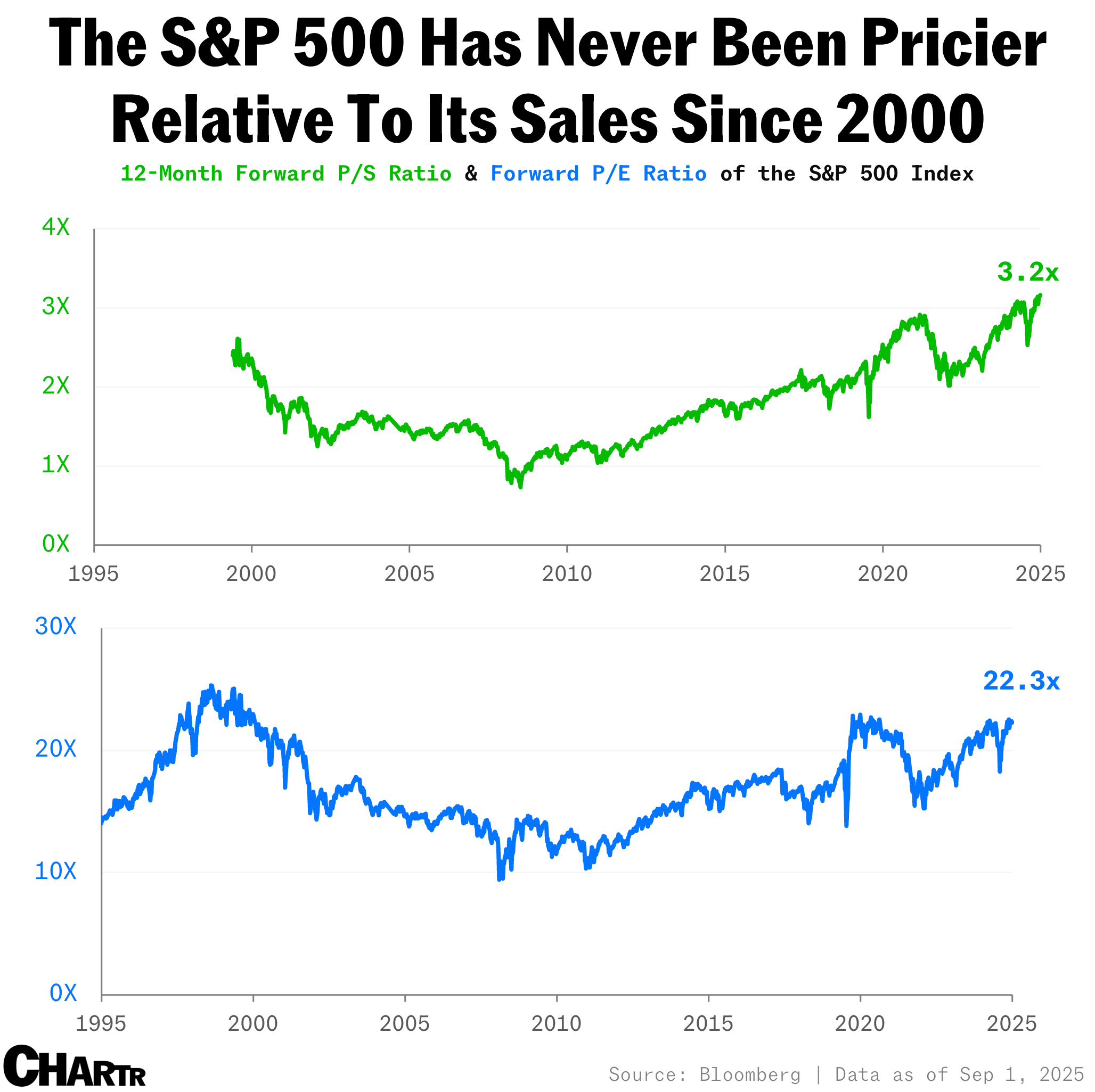

Investors are paying record prices for every dollar of future S&P 500 revenue

The current market is a Rorschach test; do you see a golden age of corporate profitability ushered in by AI, or irrational exuberance gone mad?

US stocks may be breaking new ground, but with every fresh high, the chorus of people asking “are stocks overvalued?” gets a little bit louder.

According to The Wall Street Journal, the S&P 500 now trades at about 22.5x projected earnings for the next year, well above the three-decade average of 17.1x and inching closer to the dot-com peak of over 25x in 1999.

Things look even more stretched on a price-to-sales basis: the index is now at a record 3.2x forward revenue — meaning investors are paying more than ever for every dollar of sales the S&P 500 companies are expected to generate over the coming 12 months.

All eggs in tech

In fact, the split between the two ratios shows a deeper issue in today’s market: its reliance on Big Tech. The 10 largest companies of the S&P 500 now make up nearly 40% of the index’s total value, and most of them are uber profitable megacap tech stocks, their tasty margins keeping a lid on the P/E ratio.

Nvidia, for example, has an operating profit margin near 60%, and it alone represents more than 7% of the index, dominating the S&P 500 more than any company has for 44 years. Back in 1990, by contrast, the top 10 companies were less dominant and came from a more varied mix of sectors, including names like Exxon, IBM, Walmart, and Coca-Cola.

Put simply: stocks are undeniably expensive, whether measured on profits or sales. Whether you think that’s a problem depends a lot on whether you think the BATMMAAN stocks are about to collectively stumble.