Investors have a “particularly enhanced buying opportunity” in Apple, says Bank of America

Bank of America is pounding the table on Apple’s attractive risk-reward profile after the stock’s massive tariff-induced plunge.

“In our view, the pullback presents a particularly enhanced buying opportunity for investors to own a high-quality name,” a team led by Wamsi Mohan wrote.

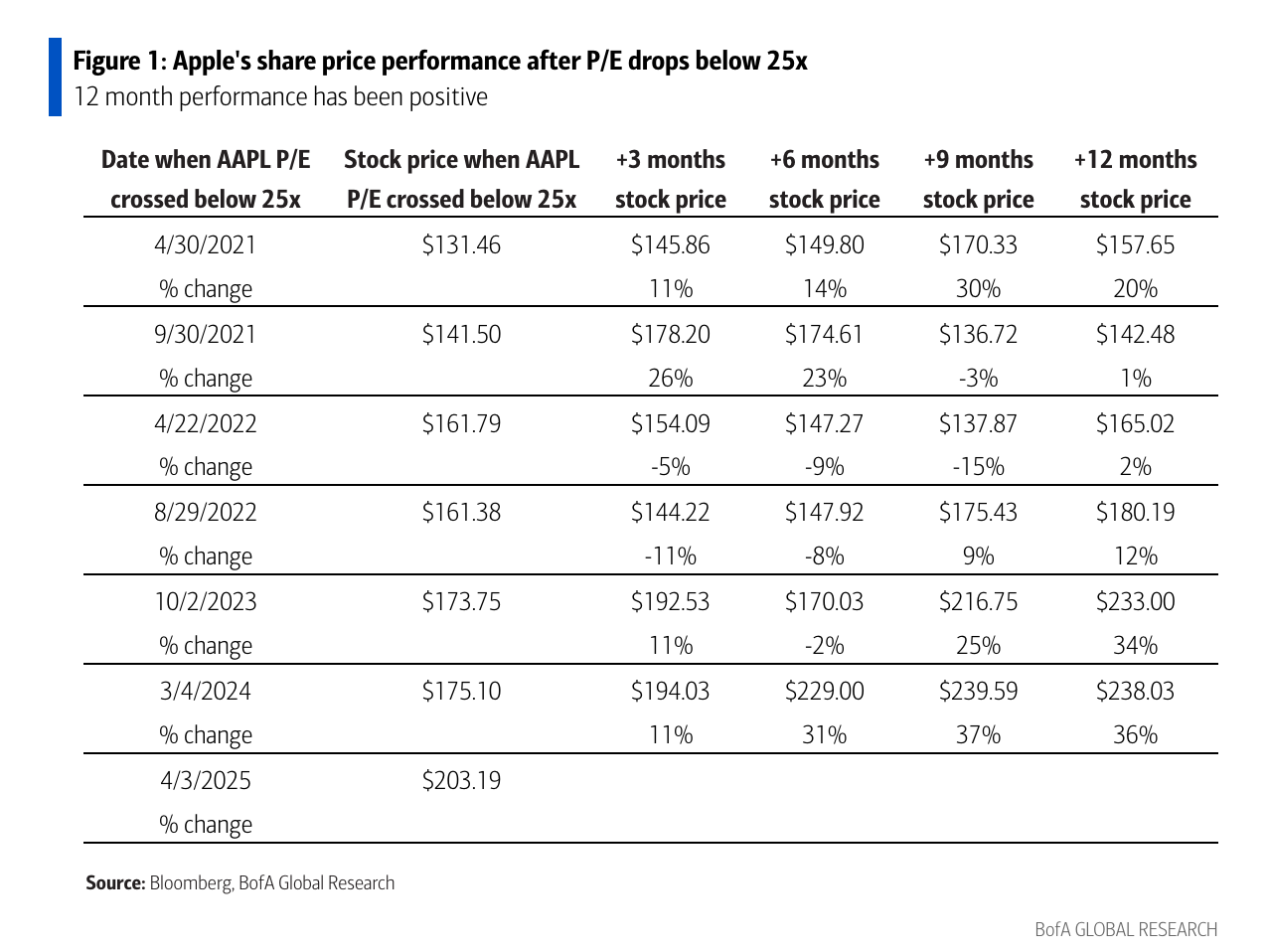

While acknowledging that “history is not a guide,” Mohan examined times when the iPhone maker’s 12-month forward price-to-earnings ratio has fallen below 25x, a threshold it breached recently.

The forward returns are encouraging:

Bank of America has a “buy” rating and $250 price target on the shares.

Management has some options at its disposal to blunt the potential impact of tariffs, according to Mohan, such as moving production to India, raising selling prices, or squeezing its suppliers.

Taken plainly, this note is a resounding endorsement of one of America’s leading companies. But I think it’s also revealing as to the challenges investors have in trying to assess what constitutes “value” in the current market environment.

First, a forward price-to-earnings ratio below 25x doesn’t exactly scream “cheap.” Second, all these periods of multiple compression examined by BofA have come since the end of 2020. So, we’re really only looking at a valuation cushion that’s seemingly existed for the company during a time in which the US stock market as a whole has been very richly valued. The sample size is understandably small, and I have thoughts about the folly of low-n analysis.