Everyone thinks stocks are overvalued and no one cares

The summary of Bank of America’s monthly survey of fund managers with nearly half a trillion in assets under management:

Portfolio managers are fully invested, as cash as a share of assets stayed near historical lows at 3.9%.

“Long Magnificent 7” — that is, the cohort of Nvidia, Meta, Tesla, Alphabet, Microsoft, Amazon, and Apple — is once again judged to be the most crowded trade.

More investors say AI stocks are not in a bubble (52%) versus those who think they are (41%), though the gap has narrowed over the past month.

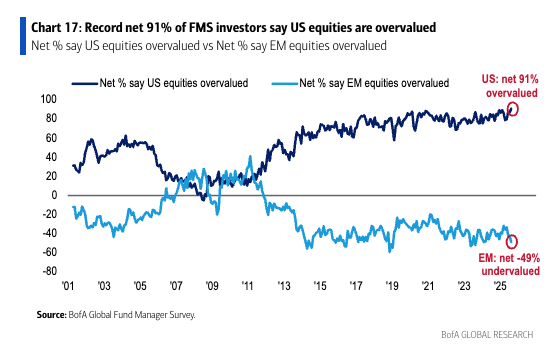

A record 91% of those surveyed said US equities are overvalued.

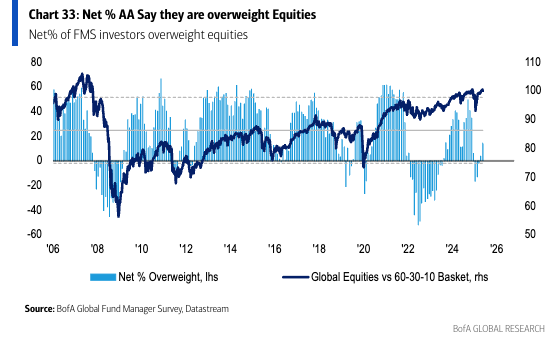

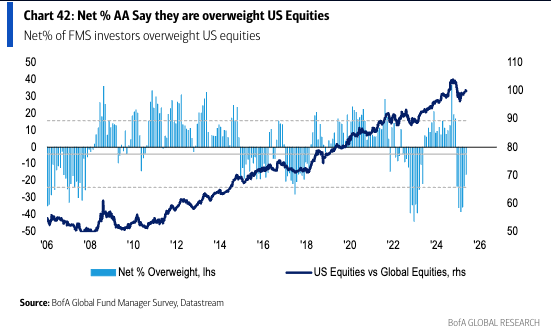

Fund managers are the most overweight global equities they’ve been since February 2025...

...and that’s recently coincided with a reduction in their underweight position in US equities relative to benchmark (i.e. buying more US stocks).

Putting this together, US stocks are expensive, but not expensive enough to sell. In fact, judging by what portfolio managers are saying, it looks like it’s riskier not to own them.

“Bottom Line: not a clear and obvious inflection point in our survey but most bullish FMS since Feb’25, with probability of hard landing lowest since Jan’25, cash as % AUM at historically low 3.9%, equity allocations on rise but not at extreme levels,” Bank of America Chief Investment Strategist Michael Hartnett wrote.

To quote the exceptional market technician Helene Meisler, there’s nothing like price to change sentiment.

In March, this survey showed the “biggest drop in US equity allocation ever” with the lion’s share of respondents saying that “US exceptionalism” was past its peak as a market theme.