Costco is having its Netflix moment

A fresh defense against membership moochers

A friend of mine lost their wallet yesterday, but was relatively unfazed. Credit cards, drivers’ licenses – those can be easily replaced or worked around with other touchless digital solutions. Most agonizing? His old roommate’s Costco membership card he’d been gifted was now gone – and with it, his side-door into a land of cheap food in high quantities. But lost wallet or not, that access was vanishing anyways. Just this week, his nearest Costco in Colorado installed new scanners at entry to verify that the people entering were actually members.

Costco recently said these new point-of-entry devices would be rolled out “in the coming months” following a pilot program put in place earlier this year.

This attempt to stem the tide of barbarians at the checkout counters means Costco is effectively following in the footsteps of a market leader in a completely different industry: Netflix.

The streaming giant, which plans to stop releasing subscriber numbers next year, initiated a password-sharing crackdown in 2023 that drove an acceleration in subscriber growth. It may have been a bit of a sugar high for the company, but the move was still heralded as enough of a success to be mimicked by the likes of Disney – and now, Costco.

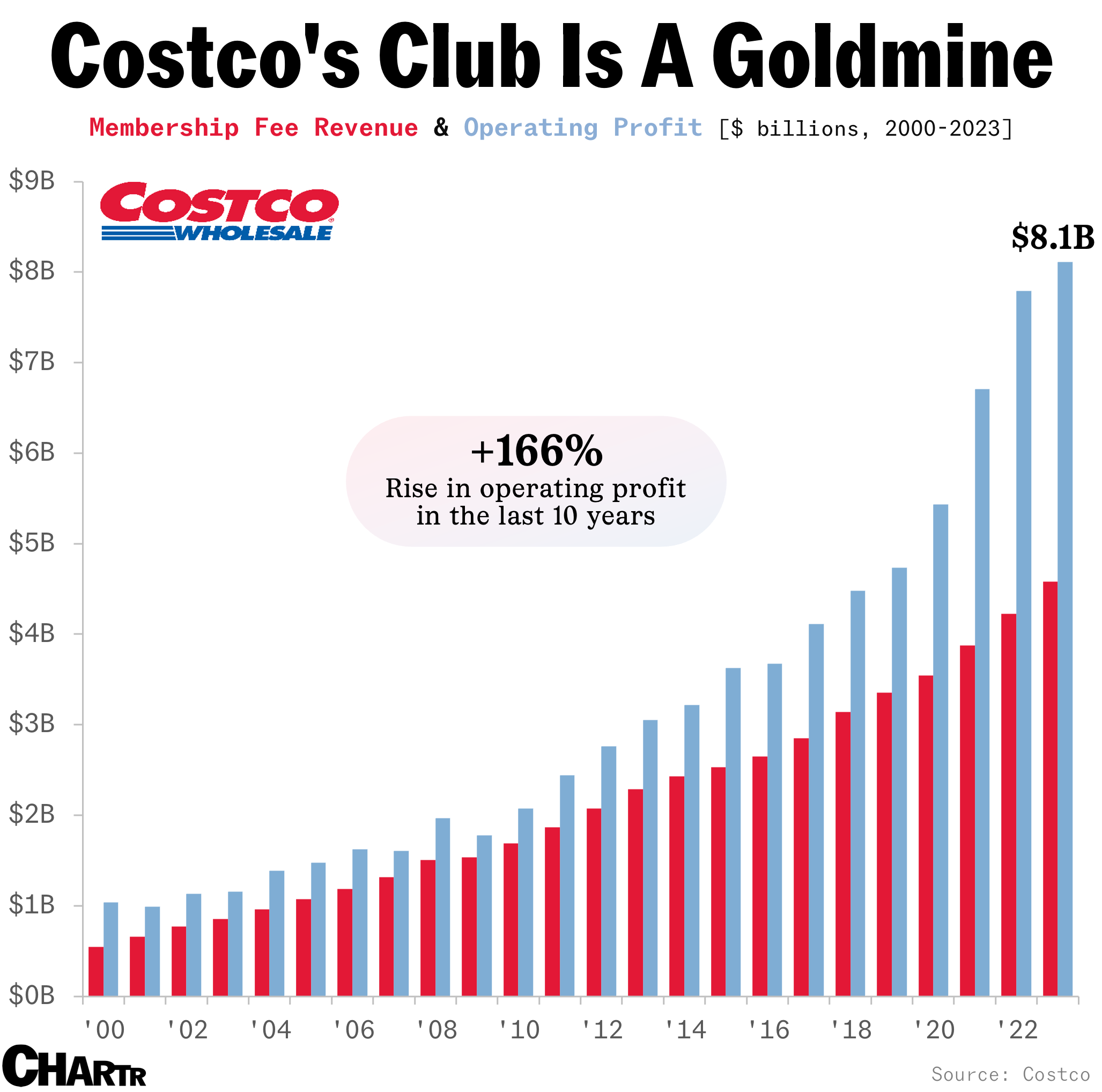

The wholesale club operator has good reason to protect this cash cow: membership fee revenues amount to about 50% of its total operating profits, and this aspect of its business model is particularly enticing to investors.

The forward price-to-earnings ratio for Costco is a whopping 47.5x, versus less than 20x for the S&P 500 as a whole. Investors are willing to pay up for perceived security in profit growth driven by the firm’s sticky, growing membership base.