If April was “Sell America” month, June was “Buy America” month — and it was 9x the size

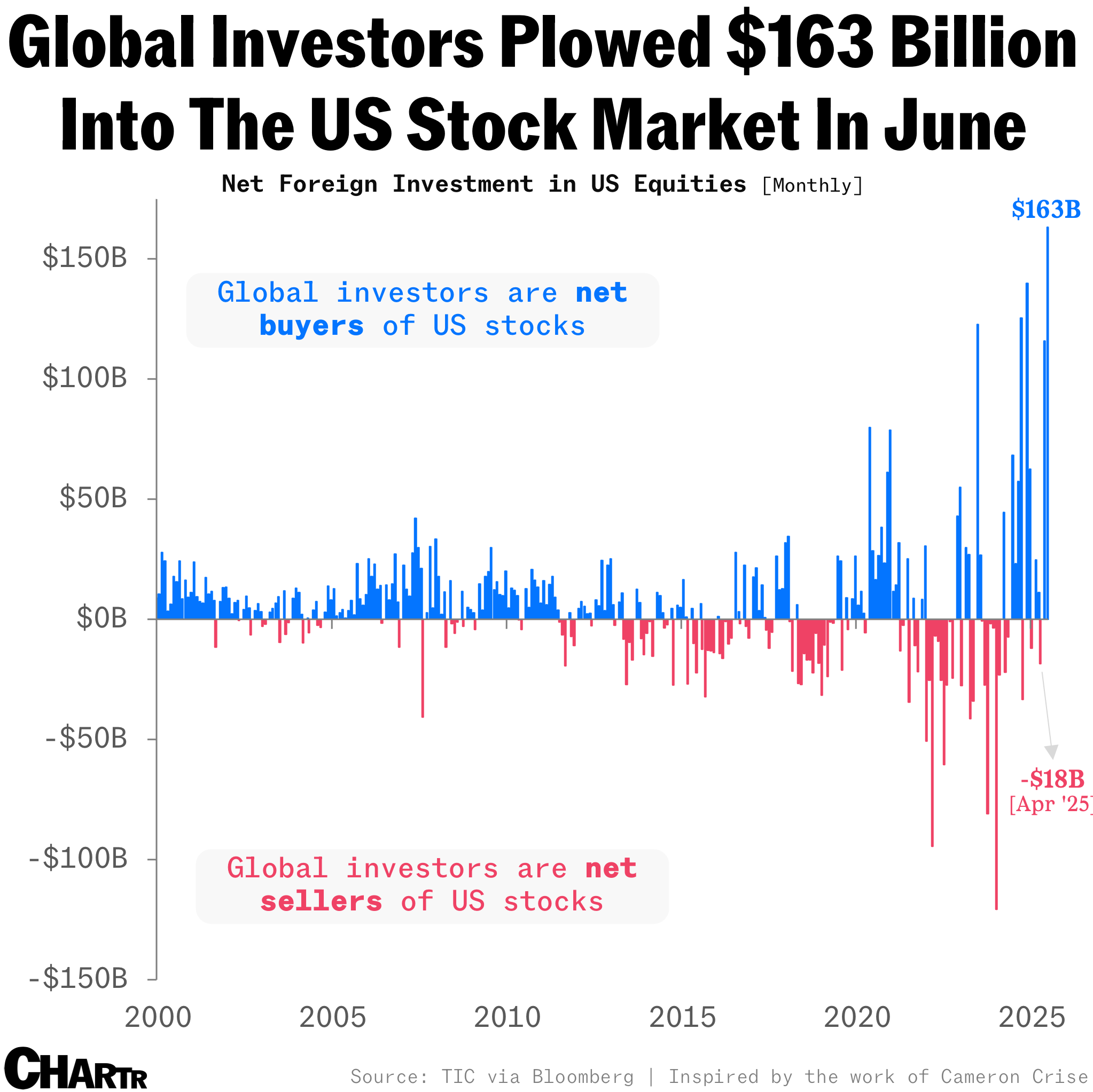

Retail traders aren’t the only ones buying the dip in this bull market, as foreign investors plowed $163 billion into US equities in June, the most on record.

Much has been made of the “Sell America” trade, as President Trump’s “Liberation Day” in early April upended notions of what global trade norms should be, sending stocks and the US dollar tumbling.

But the truth is that “Sell America” — the idea that investors were redrawing the world in their heads, reacting to a seismic shift in the global order — never really happened. Or, if it did, it was A) very brief, and B) more of a currency market phenomenon than a stock market one.

Treasury International Capital data, reported by Cameron Crise at Bloomberg on Monday, reveals that foreign investors have plowed $279 billion (net) back into US equities in the last two months, with $163 billion in June alone — the highest monthly figure ever.

For context, in April, net flows out of US equities totaled $18.4 billion; June’s buying was 8.9x that figure.

Indeed, tariffs have become old news. Recession risks have receded, the AI boom has barely blinked, and any lingering trade issues in supply chains are being lumped into the “solvable” category of jobs to be done. That’s given the green light for global investors to run the same playbook that retail traders have been employing: buy each and every dip.

No wonder the direction of travel has been so remarkable, with the S&P 500 Index rising 29% since April 8.

Sell some of America?

Interestingly, this has been more of an equity story than anything else. Treasurys continue to reflect more of a US inflation and policy uncertainty premium, with 30-year yields at 4.91%, and there have been negligible flows into US government bonds in recent months, with fiscal concerns still fresh in many minds.

Of course, the US Dollar Spot Index itself remains down roughly 10% for the year. So from the perspective of foreign buyers, the S&P 500 is roughly flat year to date.

In all, the “Sell America” story looks to have been more a case of large foreign institutions electing to hedge the ample US dollar exposure they already have rather than dump those American assets.

A recent Morgan Stanley analysis suggest that Danish pension funds and insurers, the only cohort with detailed data available post-April, shows that hedge ratios (or the share of US dollar assets that are insulated from currency fluctuations) rose since the start of the year, but “remained flat between May and June.”

As long as the US equity market contains the AI-exposed tech giants, and as long those AI names continue to power both the economy and corporate earnings, it’s hard to see the world really embracing the “Sell America” idea in US stocks en masse.

Of course, people will always look for reasons to sell — and there is nothing like looking, if you want to find something. For now, concerns about stretched valuations seem to garner the most agreement (typically just before the market hits a new, more expensive high).