Andrew Left should have taken his own advice

A backtest of Andrew Left's stock picks shows that investing in his recommendations would have made you a lot of money.

Earlier today, The Wall Street Journal reported that federal prosecutors had charged short seller Andrew Left with fraud, alleging that Left made $16 million in illegal profits through misleading and exaggerated statements issued from his firm, Citron Research.

The indictment, which you can read here, doesn’t look great for Left, as text records and communications with other investors allege that Left lied about not receiving payments from third-parties to publish research, and he regularly stated that he continued to hold various positions long after selling.

If convicted, Left could face more than 25 years in prison. I’m not going to speculate on whether or not Left will ultimately be convicted, but, considering that fraud cases typically involve other investors losing money, I was curious how Left’s stock picks cited in his indictment performed over the long run.

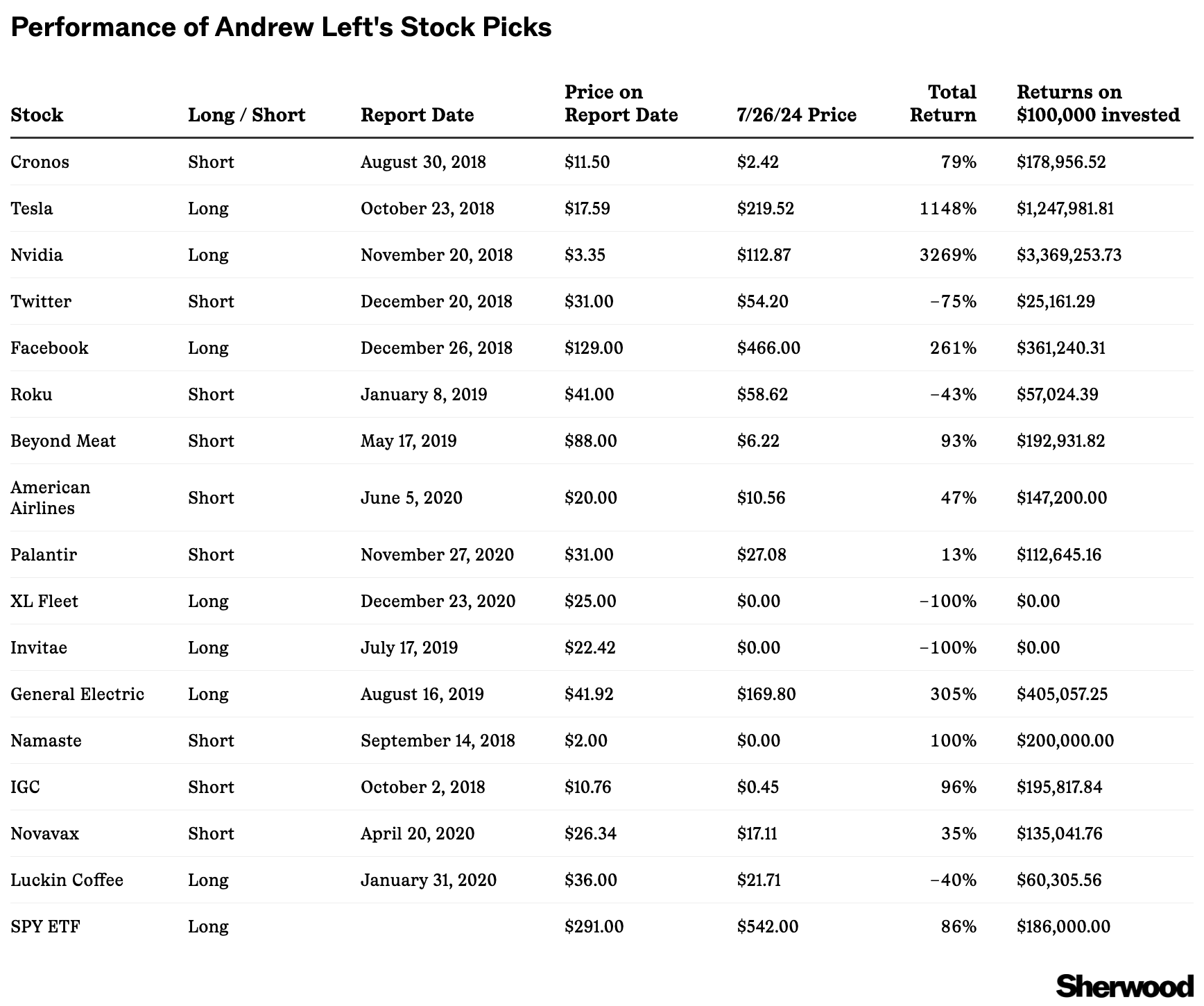

The indictment accused Left of manipulating 17 stocks (page 35), and it provided details, including the date of Left’s reports/tweets and whether Left was “long” or “short,” for 16 out of 17 of the stocks. I tested Left’s recommendations to see what would have happened if you had bought or shorted each of the 16 stocks the day their reports were published, and the results are… impressive.

If you had purchased or shorted $100,000 of each of Left’s 16 recommendations described in the indictment the day he published his report and never closed your position, you would have turned $1,600,000 into $6,688,617.44 (excluding borrow fees) for a 318% return since making the first trade in August 2018.

If you had invested that same $1,600,000 in the S&P 500 in August 2018, you would be up ~86% right now. The “long Left” portfolio would have outperformed the S&P 500 by 3.7x since August 2018.

Maybe Left should have just trusted his own reports, because his picks turned out to be pretty accurate.