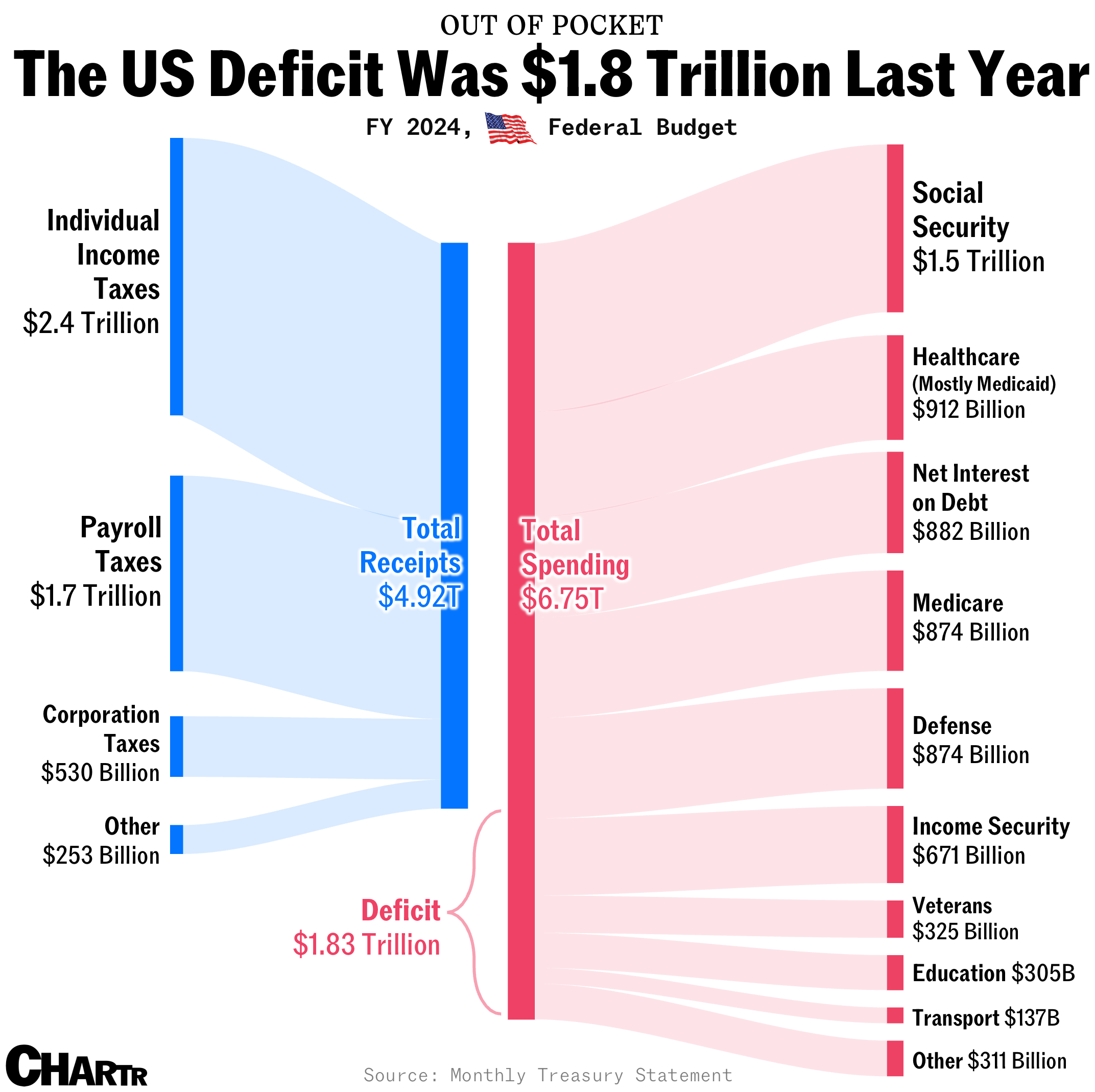

America spent more than $880 billion just on interest on its debt last year

No wonder Moody’s stripped the US of its last AAA rating.

America’s perfect credit era is officially over — marking the end of a century-long run.

On Friday, Moody’s downgraded the US credit rating from its highest AAA grade to Aa1, citing “large annual fiscal deficits and growing interest costs.” The move follows earlier cuts from S&P in 2011 and Fitch in 2023, driven by rising debt concerns and political gridlock.

Now, for the first time since 1917, the US no longer holds top-tier ratings from any of the major agencies — trailing the 11 countries that still boast the highest grading from all three, a group that includes Australia, Denmark, Germany, and Canada.

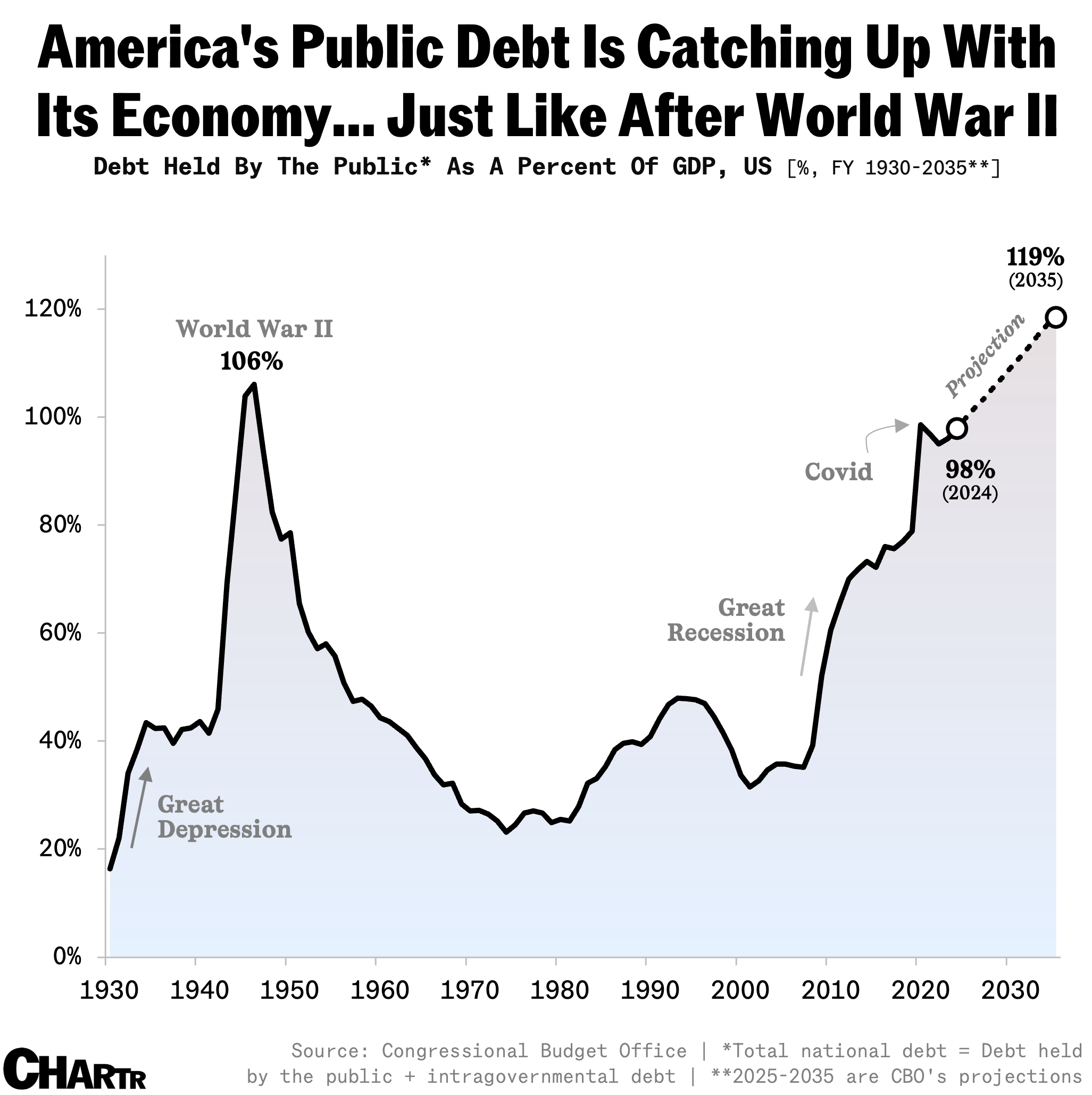

With the clock ticking on America’s $36 trillion debt ceiling (which could be breached as soon as August) the national debt continues to climb, as it has done for decades. According to the Congressional Budget Office, the US public debt stood at 98% of GDP last year, and is set to surpass the WWII peak by 2029, hitting 119% by 2035.

What might be of particular concern to the number crunchers at Moody’s is not just the current level of federal debt, but how quickly it’s growing. Last year, the deficit was $1.8 trillion, more than 6% of GDP. The interest payments on debt alone were some $882 billion, greater than the defense and Medicare budgets.

The latest tax cuts and spending push — or, as President Trump calls it, “the big, beautiful bill” — could add another ~$4 trillion to the federal deficit over the next decade, with Moody’s now projecting that the debt-to-GDP ratio could surge to 134% by 2035.

In an interview with NBC yesterday, Treasury Secretary Scott Bessent shrugged off the downgrade, calling Moody’s a “lagging indicator.” But the markets took note, with the 30-year Treasury yield topping 5% this morning, a level last seen in late 2023.