There’s a real math problem with MicroStrategy’s obscene valuation premium

MicroStrategy is worth around 3x as much as its bitcoin holdings. Let’s talk about the implications of that.

MicroStrategy, Michael Saylor’s software company turned bitcoin-holding vehicle, is worth $106 billion, making it one of America’s largest 100 companies by market capitalization. For context, the market value of the “world’s first Bitcoin Treasury Company” (a direct quote from its latest earnings report) is roughly the same as Boeing, America’s biggest airplane manufacturer; Nike, America’s biggest athletic-apparel provider; and Starbucks, America’s biggest coffee chain.

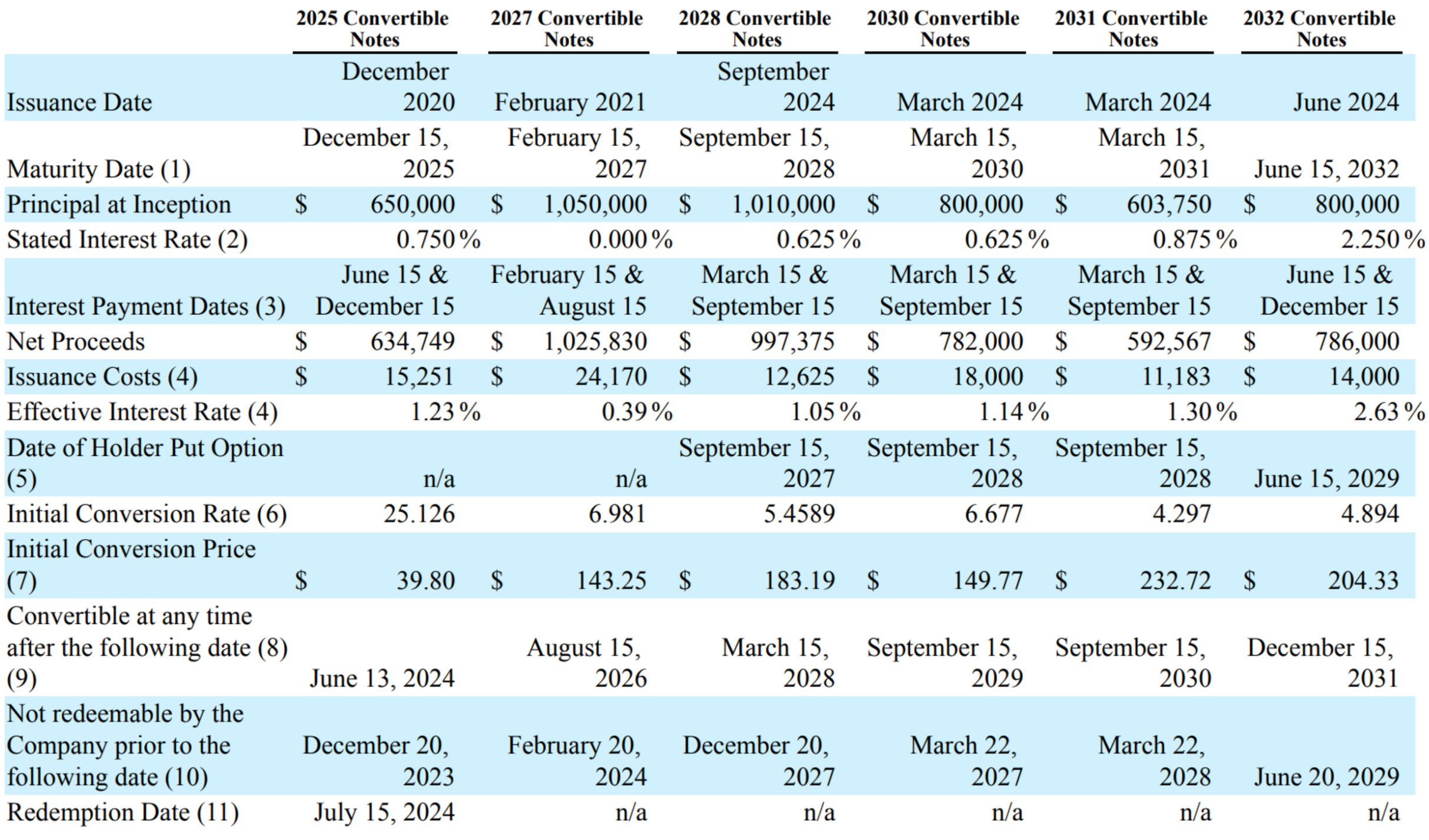

It’s a remarkable turn of events for MicroStrategy, which, from 2011 through October 2020, fluctuated between roughly $1 billion and $2 billion in market cap. The secret to its success has been bitcoin. In August 2020, founder and then CEO Saylor announced that the company had invested in bitcoin as part of its new “capital allocation strategy” in pursuit of its goal to maximize long-term value for its shareholders. Since then, MicroStrategy has doubled, tripled, and quadrupled down on bitcoin, owning 252,220 bitcoins as of September 30, according to its last earnings report, acquiring 27,200 more bitcoins between October 31 and November 10, and issuing $2.6 billion in 0% convertible bonds this week to buy even more bitcoin.

The last point, specifically, has been the key to Saylor’s bitcoin-purchasing machine: MicroStrategy issues convertible bonds to raise cash to buy more bitcoin. For a primer, convertible debt is a type of bond that can be converted into a predetermined number of shares of the issuing company’s stock at a future date. There are a few benefits of using convertible debt over selling “normal” bonds.

First, the interest rates are typically lower, making the debt easier to service. MicroStrategy’s most recent debt raise was at 0% interest, meaning it doesn’t have to make any interest payments to bondholders, and its last convertible note offering from September 2024 was 0.625% which is, again, very cheap. Proceeds from this note were actually used to pay off the company’s outstanding 6.125% senior secured notes (which, as you can see, had much higher interest), and any net proceeds were also used to — you guessed it — acquire more bitcoin.

Convertible notes also minimize cash outflows from the issuer if its stock price appreciates. These notes are redeemable for shares, typically at a stock price above the company’s current price. For example, if a company’s stock price is $100, the company issues convertible notes with a conversion price of $130, and the stock climbs to $200 before the notes are due, debtholders can exchange their notes for stock at $130 per share and sell for $200. The convertible note, in this instance, is effectively a call option for the debtholders, and while the issuing company’s stock is diluted if bondholders convert debt to equity, no cash has to leave its balance sheet.

For MicroStrategy, convertible notes have been the key to letting the company acquire more and more bitcoins with cheap leverage. However, a premium has emerged between the value of MicroStrategy and the value of its bitcoin holdings. As noted above, MicroStrategy is worth ~$106 billion, but the greatest possible value of its bitcoins is around $30 billion. (252,220 bitcoins in September 2024, 27,200 bitcoins purchased in early November, and ~27,000 bitcoins it could purchase with the $2.6 billion it just raised equals around 306,420 bitcoins.)

MicroStrategy is worth more than triple the value of its underlying bitcoins, and while, yes, it does still sell software, the company’s software business *checks notes* lost $18.5 million on $116 million in revenue last quarter. Unless we’re using Truth Social valuations, software sales don’t explain the ~$70 billion gap between MicroStrategy’s bitcoin holdings and its own valuation. I first noticed this around a month ago, and at the time, my thought was, “This looks like an arbitrage opportunity!” Why not just buy bitcoin and short MicroStrategy, right? Eventually, that premium should close, right? Probably not, as long as the bitcoin bull market keeps rolling.

When bitcoin’s price rises, the stock of “crypto” companies like MicroStrategy and Coinbase tend to rise, too. When MicroStrategy is trading at a premium to its underlying bitcoin, it can advantageously issue equity (or convertible debt) to buy more bitcoin than the equity it’s giving up.

Think about it like this: if MicroStrategy holds ~$30 billion in bitcoin and the company’s worth ~$100 billion, by issuing $1 billion in convertible debt (or equity) to buy bitcoin, its bitcoin holdings increase by ~3% while equity is only diluted by ~1%. Buying pressure sends the price of bitcoin higher, MicroStrategy’s stock continues to increase as bitcoin grows more valuable, and the cycle repeats.

In November 2021, Citrini Research published an excellent piece discussing MicroStrategy equity, convertible notes, and its premium over its bitcoin holdings, where they described this phenomenon as a “perpetual motion machine”:

“In a bitcoin bull market, it is the financial equivalent of a perpetual motion machine - reflexivity incarnate where higher bitcoin prices drive → a higher premium which → allows more equity and debt issuance by MSTR that in turn results in → more bitcoin on MSTR’s balance sheet, buying pressure which can drive higher bitcoin prices, which drives → a higher premium which… (ad infinitum, or ad “until bitcoin goes down”-itum).”

Basically, as long as bitcoin keeps going up, MicroStrategy’s convertible debt → bitcoin purchases amplify that trend. But if and when bitcoin enters a bear market, MicroStrategy could have problems. So far, because the stock has continued to climb, MicroStrategy convertible debtholders have been able to profitably convert their notes to equity, as the stock price has outpaced their conversion prices. Yet MicroStrategy’s stock price is highly correlated with bitcoin’s price (obviously). For example, when bitcoin fell from $64,000 to $16,000 in 2021, MicroStrategy, which held between 120,000 and 130,000 bitcoins, fell from $81 to $16. Now, MicroStrategy’s premium is trading at an all-time high, while its bitcoin holdings have more than doubled.

If MicroStrategy’s price falls below conversion prices, and remains below conversion levels through the notes’ maturity dates, MicroStrategy may have to sell some of its bitcoins to pay its creditors. The company had more than $4.8 billion in outstanding convertible notes as of September 2024, and it just raised another $2.6 billion due in 2029. The conversion prices for its collective $4.2 billion due between 2027 and 2032 range from $143.25 to $232.72, and the conversion price for the most recent note is $672.40.

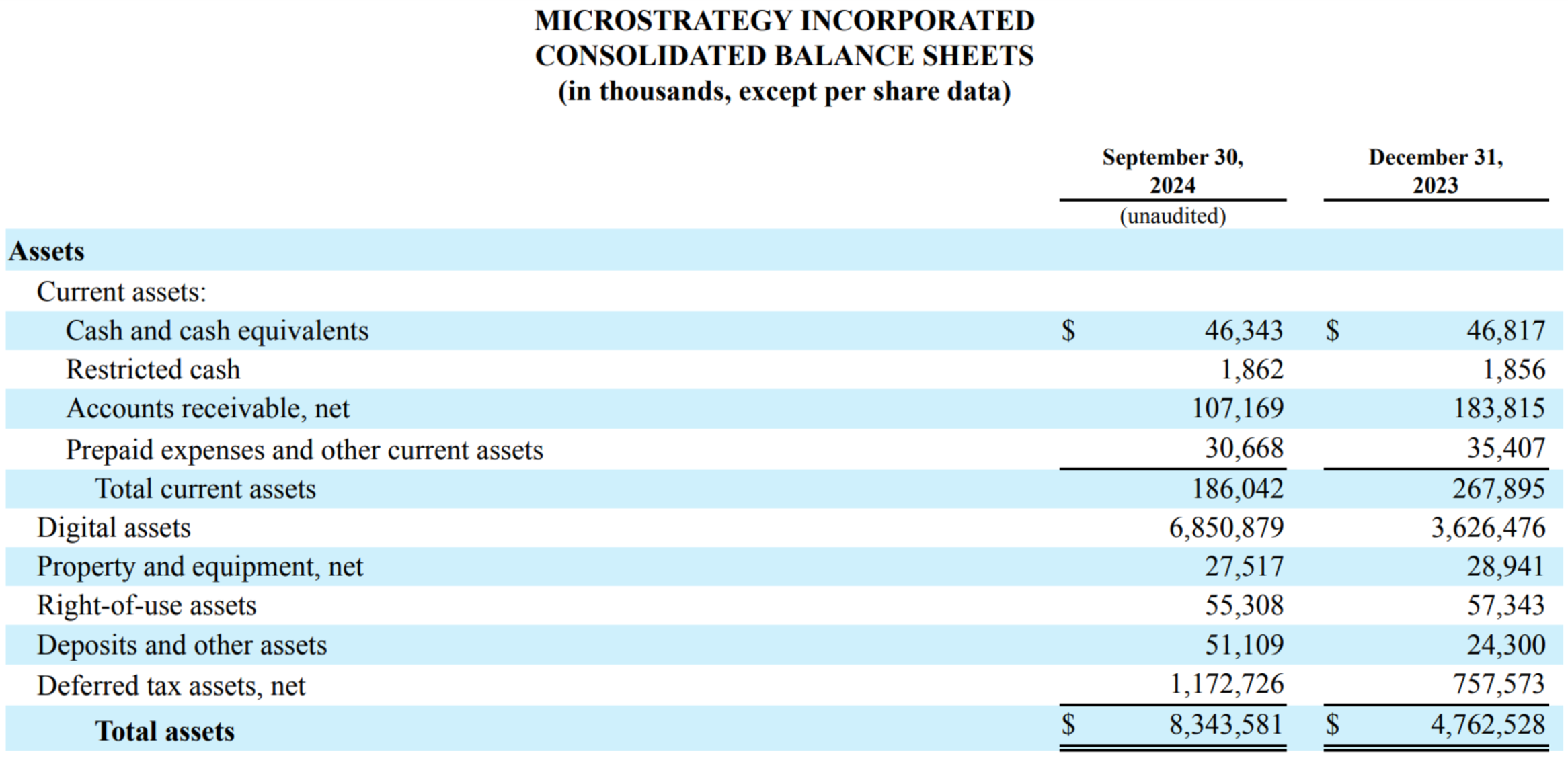

While MicroStrategy’s stock is currently around $440, well above all but the most recent conversion price, it was trading below $120 as recently as two months ago, and it hadn’t broken $200 until the recent rally. Additionally, as of September 30, MicroStrategy had $46.3 million of cash and cash equivalents.

If an extended bitcoin bear market were to drag MicroStrategy’s stock below its conversion prices, the company could be on the hook for more than $4 billion to repay convertible noteholders over the next four years. Given its lack of cash on its balance sheet, MicroStrategy would likely have to either issue more debt/equity at worse interest rates/lower prices or sell bitcoin to raise cash, effectively reversing its current “perpetual motion machine”: sell bitcoin to pay back debtholders, which would further decrease bitcoin’s price, which would lead to selling more bitcoin to pay back debtholders, etc.

So to answer the question, “Why does MicroStrategy trade at a premium?”

It’s because while bitcoin is in a bull market, MicroStrategy both benefits from and contributes to that bull market thanks to its ability to accretively raise capital to buy more bitcoin. But an extended bitcoin bear market dragging down MicroStrategy’s stock price could force it to sell some of its holdings to pay back creditors. Leverage works both ways, but so far, Michael Saylor has been winning.