The money is flooding in, but what are prediction markets truly telling us?

We did a Q&A with Kalshi to learn more about the disparity between prediction markets and traditional polls.

Since the summer, prediction markets have been having their moment in the limelight.

In July, prediction-market platform Polymarket hit the mainstream with The Wall Street Journal covering Joe Biden’s dropout odds. Once Biden dropped out of the race on July 21, Polymarket gained even more momentum, with Bloomberg incorporating Polymarket’s election odds into its Terminal service in late August. Despite its growing notoriety in the US, however, Polymarket only operates overseas due to the CFTC ruling in 2022 that Polymarket didn’t comply with federal regulations.

However, another prediction-market platform, Kalshi, does operate in the US. While the CFTC initially rejected Kalshi’s proposal for prediction markets on election outcomes, the US Court of Appeals for the District of Columbia ruled in Kalshi’s favor earlier this month, allowing the exchange to launch prediction markets for this year’s US elections. In the weeks since this ruling, in favor of Kalshi, more than $100 million has been wagered on the winner of the presidential election.

With prediction markets now mainstream, a new question has emerged: what are these markets actually predicting?

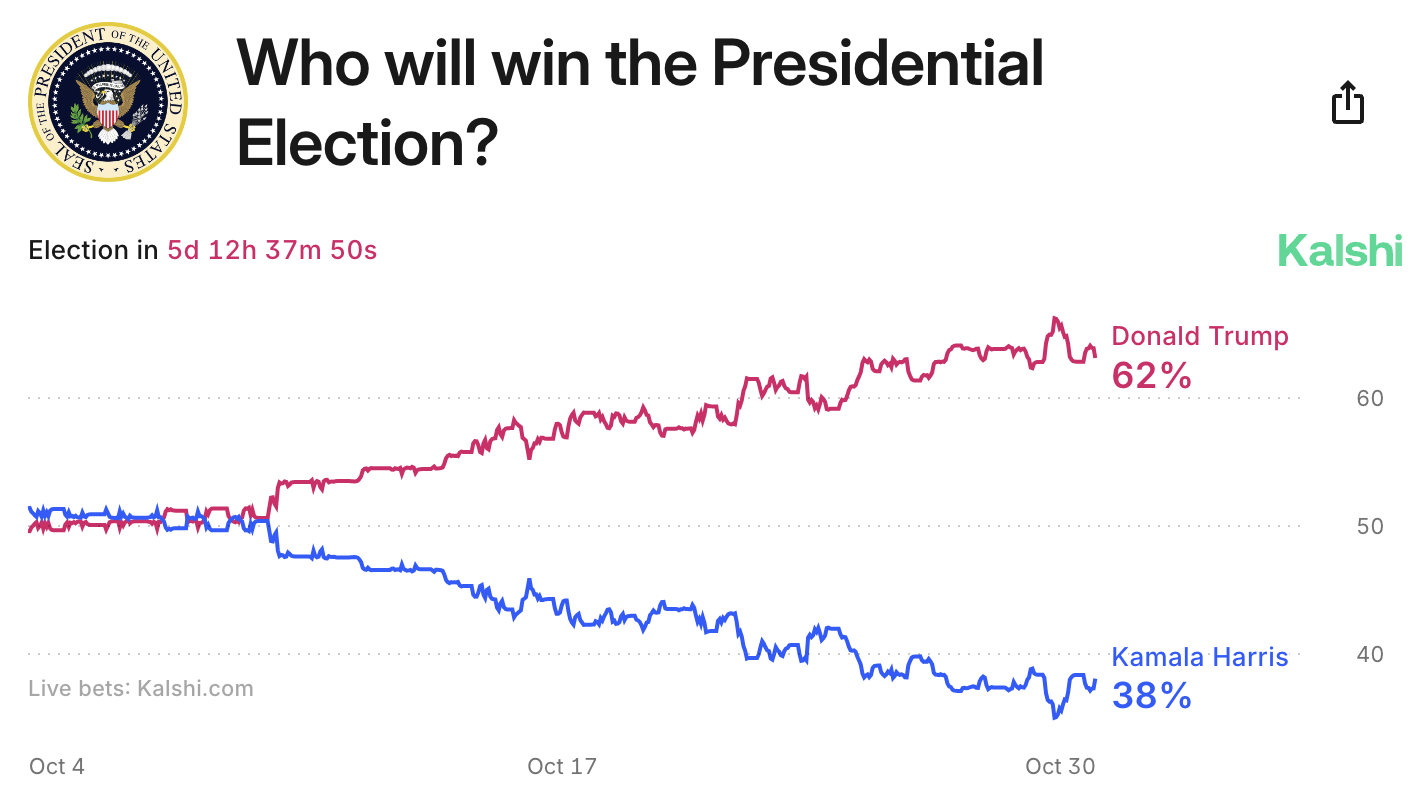

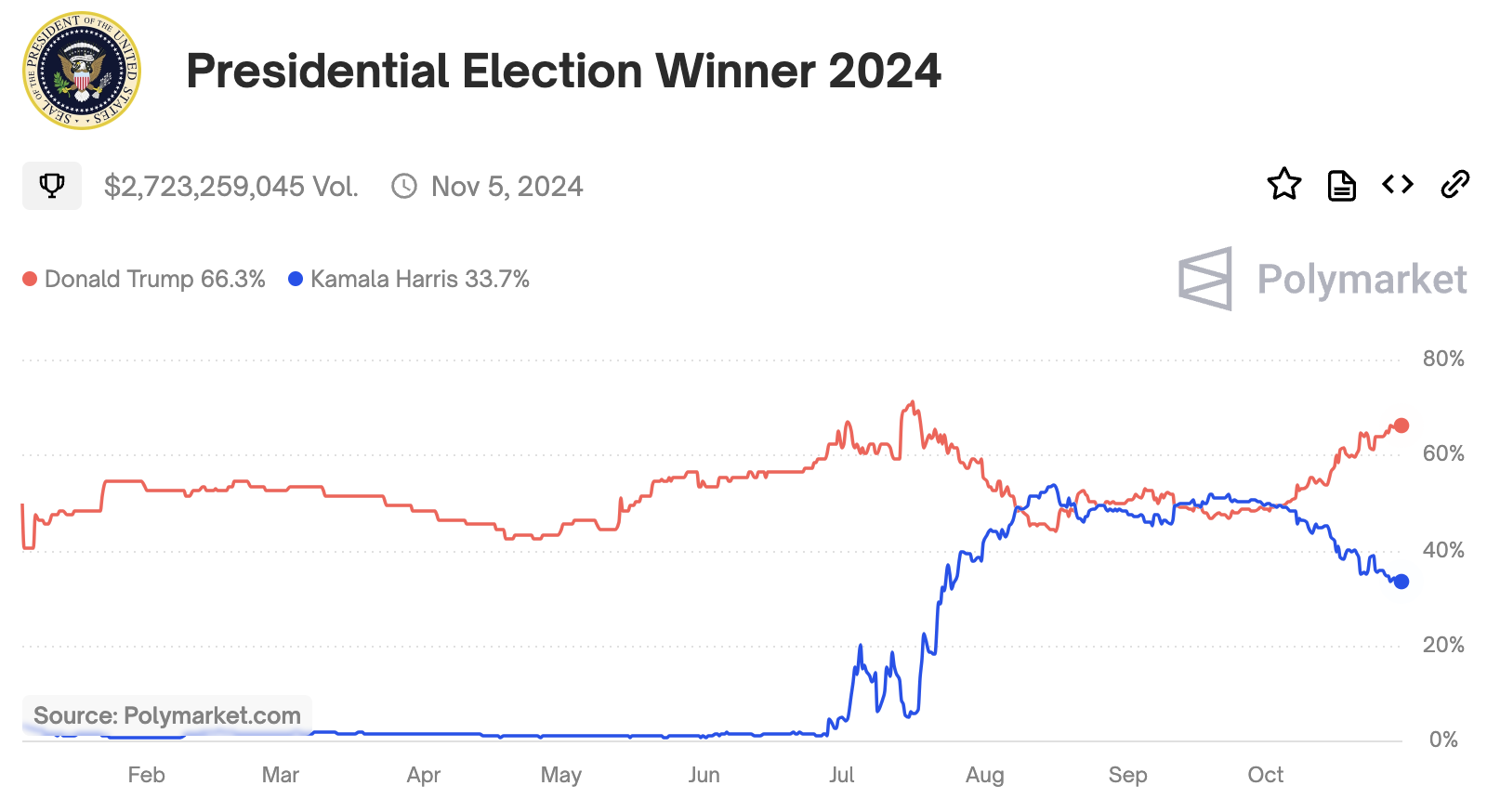

As of October 29, Trump is favored 61 - 39 on Kalshi and 66 - 34 on Polymarket:

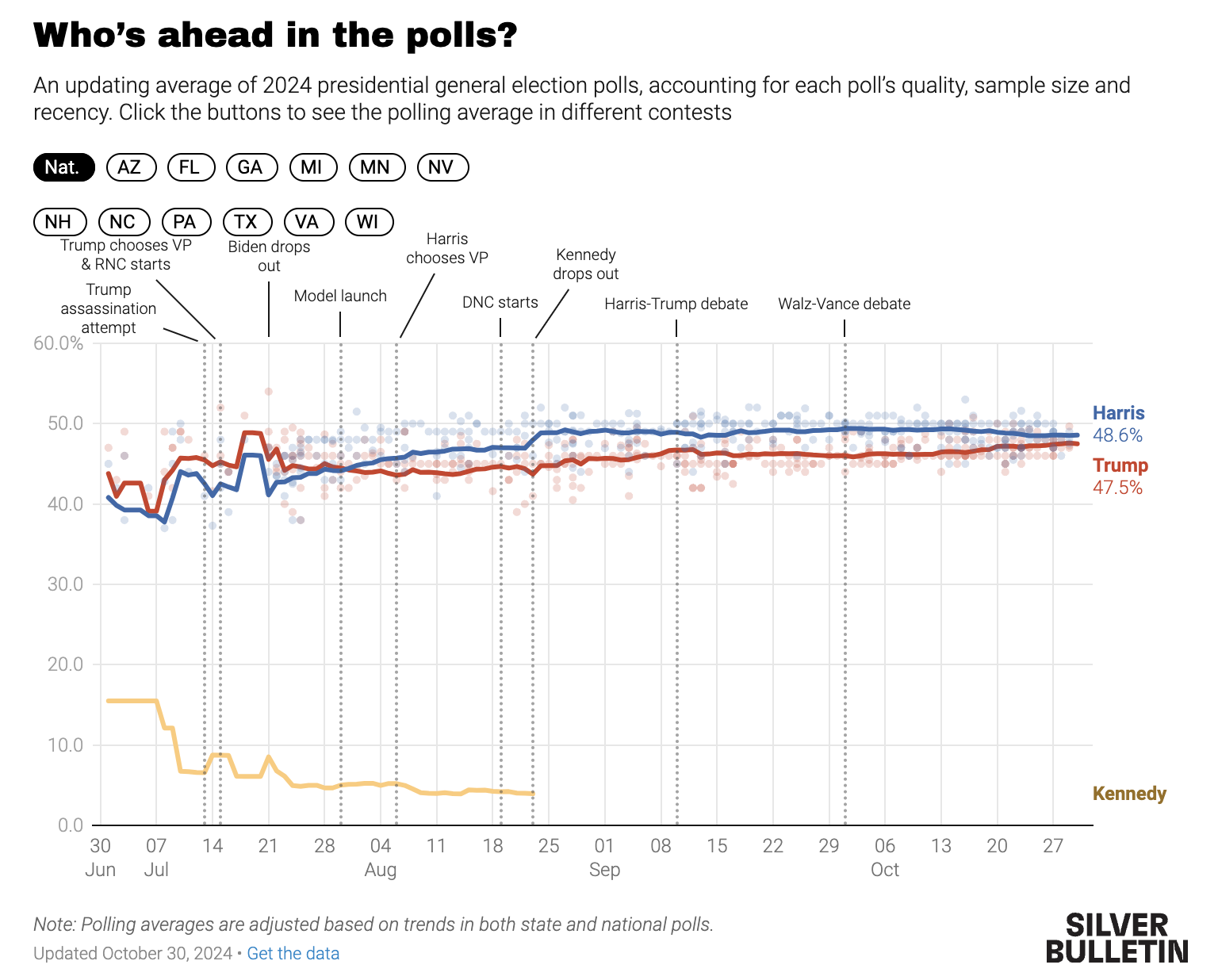

Meanwhile, polls on 538, The New York Times, and Nate Silver’s Silver Bulletin all show tight races with Harris leading by 1% to 1.5%. Additionally, because the polling in all seven battleground states is within a couple of points, Silver gave the election 50-50 odds.

Like many of you, I was curious about the discrepancy between prediction markets and polls. Do prediction markets skew conservative, with bettors’ personal interests moving the markets? Is a whale (or whales) moving the market due to low liquidity? Are prediction markets wrong? Are the polls wrong? To learn more, I spoke with someone from Kalshi to learn more about what prediction markets are, and aren’t, telling us. The following is a Q&A I had with Jack Such from Kalshi’s strategic partnerships team, edited for clarity.

Jack Raines: Right now, Kalshi is pricing 60-40 odds toward Trump, but Nate Silver’s model is showing 52-48 in Harris’s favor. My initial thought is that when people put money behind their election predictions, their personal conviction could cause them to pay above “market odds” for their candidate. For example, if they, personally, have 80% conviction on a bet that’s priced at 55% to 60%, they’ll make that bet, even if the polls say a candidates’ odds are lower. But is there anything else going on here? Why are Kalshi’s election odds priced so differently from the polls right now?

Jack Such, Kalshi: You're correct that some people will bet with emotional conviction regardless of what the prediction-market odds and polling numbers say. However, since it's a market, and we have large traders and institutions in this market, there is a self-correcting mechanism where those odds will get balanced out back down to equilibrium.

One big difference between prediction markets and polls is the speed at which prediction markets aggregate information: markets are much quicker. There’s been a long-running academic debate about whether prediction markets are more accurate than polls and/or how much more accurate they are, but they are certainly faster.

For example, 538 aggregates several polls. It takes time for each of those polls to get sent out, answered, and recorded before 538 can aggregate the results. Meanwhile, markets react instantly to news and sentiment shifts. We’ve seen this over the past few weeks as Trump’s odds on Kalshi have risen from around 50-50 to 60%. Meanwhile, we are now starting to see the polls, including on 538, show that Trump’s odds are rising. Not to the extent that we have seen in prediction markets, but the polls are now reflecting Trump momentum, which the market reflected instantly.

Jack Raines: Something else that I was thinking was that if a candidate has a slight polling advantage, like going from 50-50 odds to, say, 52-48, the prediction market would likely show an amplified move because bettors’ payouts are based on binary outcomes.

Jack Such, Kalshi: That's 100% correct. Because payouts in a market like this are binary, a small polling advantage or a shift in momentum is accompanied by a much larger move in prediction markets. We have seen examples of this in Senate race markets. When Tammy Baldwin had a 4% to 5% polling advantage, her prediction-market odds were around 75% because a five-point polling advantage is huge.

Jack Raines: I feel like once we’re through multiple election cycles, and assuming liquidity and trading volume continue to increase, we’ll be able to look back and more effectively measure how polling numbers relate to prediction markets. With prediction markets so nascent, there just aren’t many data points yet, but four years from now, that’s a different story.

Jack Such, Kalshi: That’s something we’re excited about with the legalization of election markets. In the past, the only real data point to compare polling to prediction markets was PredictIt in 2016 and 2020, but PredictIt is a project led by a New Zealand University, and it caps betting sizes at $850.

If we look back further, predicted election markets were actually legal in the US from the 1800s to 1924, and historical data shows that they were accurate. There’s a New York Times story of Andrew Carnegie noting how surprisingly accurate the election betting markets were at predicting outcomes. They were actually more accurate before the introduction of polling as a concept, which implies that the introduction of polling diluted the accuracy of the market, rather than the opposite. But yes, we’re excited to see more liquidity and high-volume markets this cycle, and in future cycles, because then we’ll be able to get some real answers on this polling vs. markets debate.

Jack Raines: Are you seeing examples of large bettors coming in and singlehandedly moving the market? The way I’m thinking about this is if you’re buying a stock, and you want to take a big position, if you don’t enter that position slowly, you could buy up the entire bid, sending the price higher. Have you seen any examples of this in election markets, where a few big purchases essentially eat the entire bid and spike the price, or is the liquidity deep enough now to where that isn’t an issue?

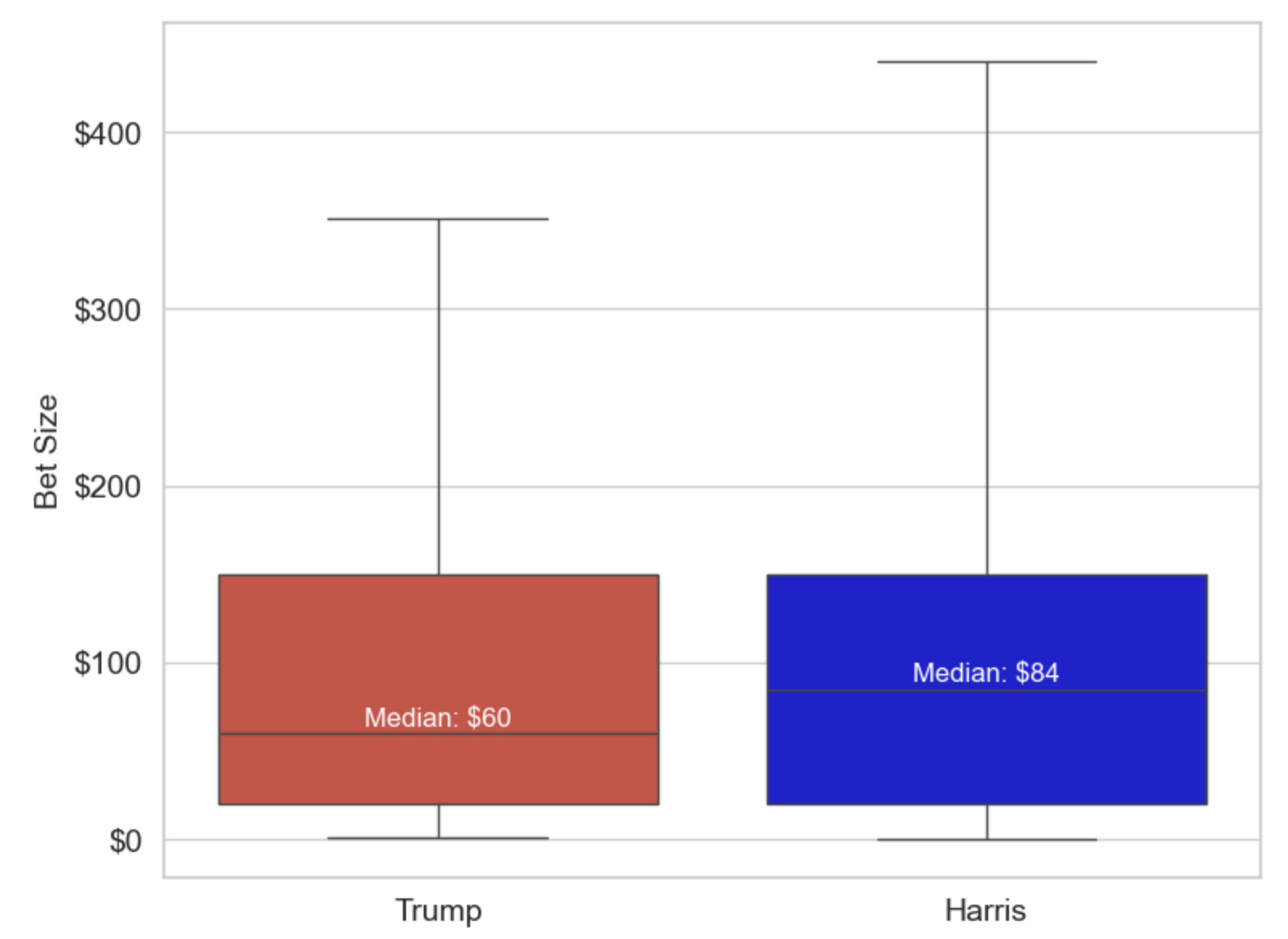

Jack Such, Kalshi: Our liquidity is deep enough to where that’s not a problem, but, regardless, we haven’t really been seeing examples of this anyway. But we do have some interesting data regarding big trades. A lot of people are claiming that Trump’s prediction-market odds have risen so much because Trump supporters are simply driving up the price to impact public sentiment. But our internal data shows that our larger traders, by position size, actually skew toward Harris. From our data, Trump’s momentum comes from smaller bettors.

Jack Raines: Interesting. Compared to Harris bettors, a higher proportion of Trump bettors are smaller accounts?

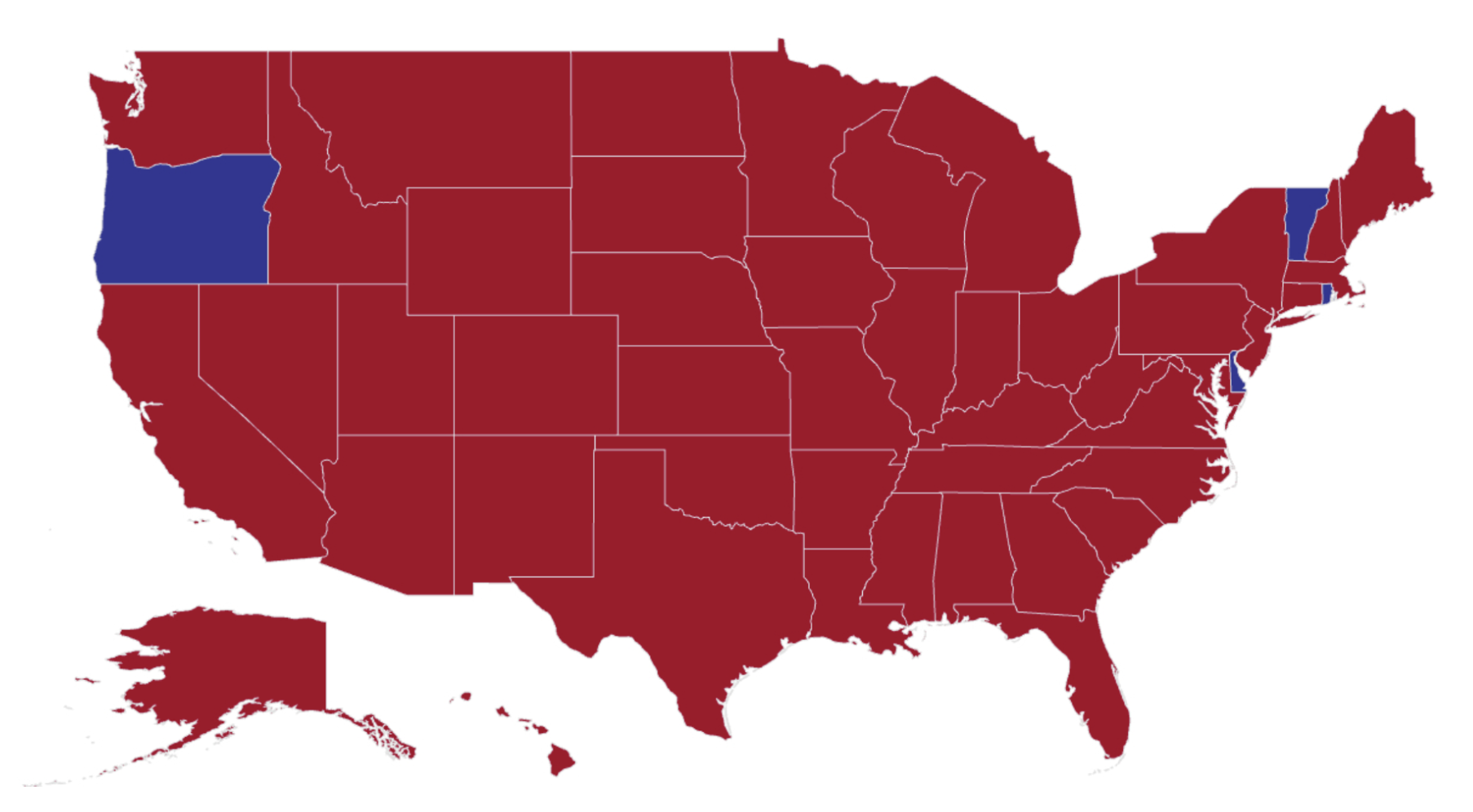

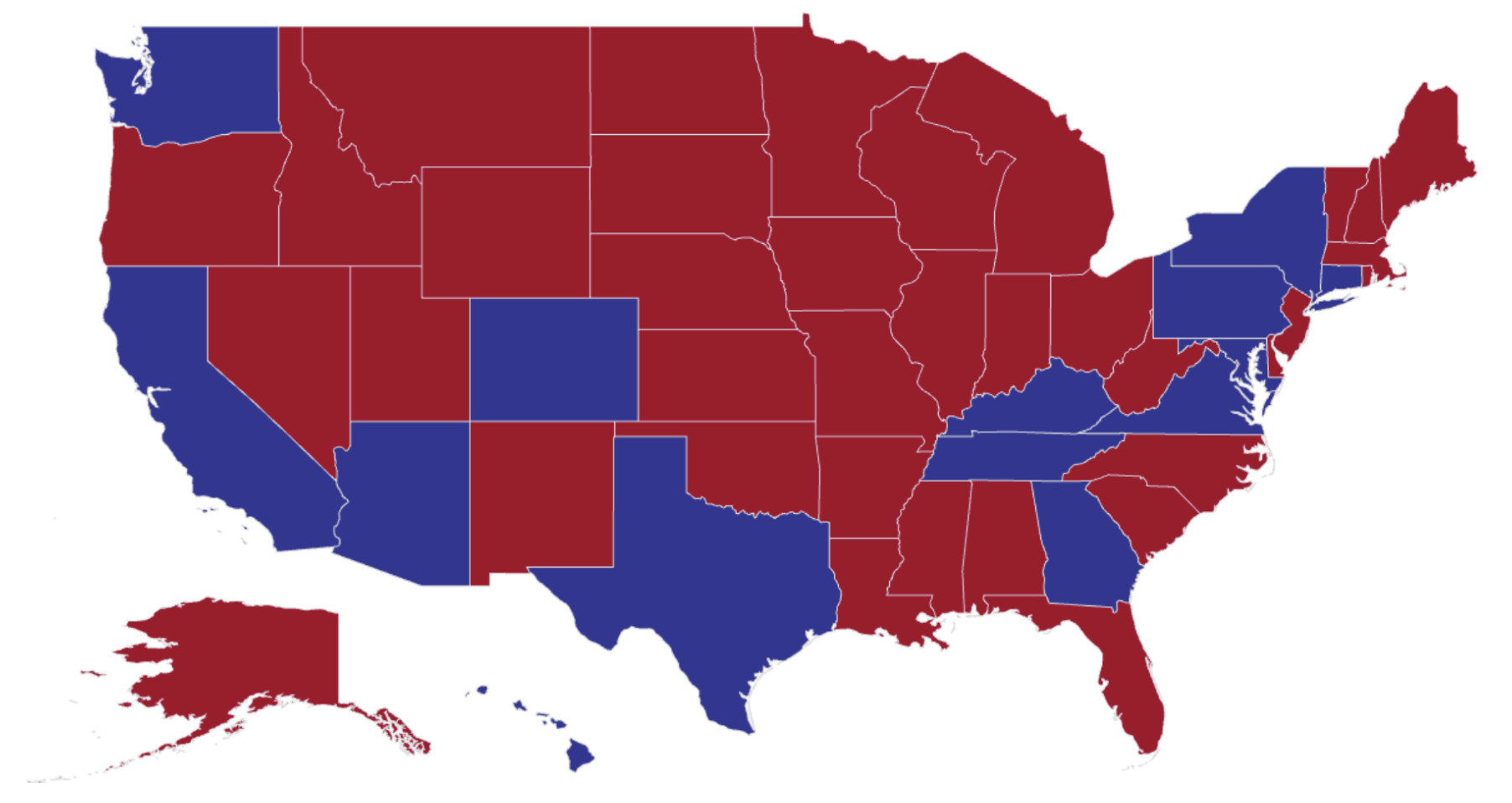

Jack Such, Kalshi: Yes, it’s actually incredible. Our state-by-state map view of small bettors is mostly red, like 48 out of 50 states, and, for context, 60% of election-market bettors on Kalshi are betting on Trump. But when you adjust the map to look at larger positions, it becomes much more blue. So we’re seeing this dynamic where small bettors are pro-Trump, and that’s what’s really driving the markets. Larger bettors, which could be institutions or sharp traders, are bidding it back in the other direction.

Jack Raines: Election markets are your biggest market now, correct?

Jack Such, Kalshi: Yes.

Jack Raines: What do you see Kalshi’s main markets being in nonelection years?

Jack Such, Kalshi: In nonpresidential election years, we still plan to offer prediction markets for international elections, as well as midterms, so we’re definitely not abandoning election markets. But outside of that, one of our more popular markets is Federal Reserve activity, like rate cuts and the size of rate cuts, because it’s an important financial hedge. Outside of that, our weather markets, believe it or not, are popular. We also have a lot of activity in our culture markets, like who will win the Oscars. But our highest volume markets, outside of elections, are Fed and weather markets.

Jack Raines: Is there an insider-trading risk with prediction markets? Like, for example, if someone who works at Tesla knows that Tesla will miss its delivery numbers for the quarter, and there is a Kalshi market for Tesla deliveries, are there safeguards in place to prevent them from making a $50,000 bet on that insider knowledge?

Jack Such, Kalshi: Yeah, we extensively screen for insider trading. We’re regulated by the CFTC. Our compliance team regularly blocks and bans users for any slightly suspicious activity, and we do detailed background checks. You have to pass a pretty extensive verification process to get on Kalshi and trade.

Jack Raines: Are there any new markets you’re excited about in Q4 or early in 2025?

Jack Such, Kalshi: Yes.

The continued release of interesting/important markets on domestic politics (e.g., will Trump raise tariffs? Will crypto get regulated? Etc.)

International elections

The success and progress of artificial intelligence

Jack Raines: Are there any misconceptions that you've seen in the media or online when people compare Kalshi to regular polls?

Jack Such, Kalshi: In terms of comparing us to polls, I think the media does a good job of noting that we’re separate. Usually it's in the context of, “You can trust polls, but not Kalshi.”

Jack Raines: Lol.

Jack Such, Kalshi: But to their credit, they do separate us. I think the biggest misconception is comparing us to other prediction-market sites — in particular, Polymarket. We're the two largest prediction markets, so it makes sense to lump us into the same paragraphs, but from an investor perspective, we’re quite different. Polymarket only operates overseas; it isn’t licensed in the US. Kalshi only operates in the US, not overseas. People call us “competitors,” but our customer bases are, by definition, entirely different. Beyond that, Kalshi’s trades settle in-house, while Polymarket uses the blockchain for its transactions.

Some critics have also claimed that prediction-market odds can’t be accurate if Kalshi and Polymarket’s odds are different. “If the markets are efficient and accurate, why are the odds so different? Why aren’t people arbitraging them?” But you can’t “arbitrage” the markets because no one can sign up for both Kalshi and Polymarket given where they operate geographically. Additionally, the settlement dates of our election markets are different: Polymarket’s presidential-election market settles when the election is called in November, but ours settles in January at inauguration. That being said, we like our data because it comes from American citizens, on the ground, voting in this election.

Jack Raines: There has to be a hypothetical arbitrage opportunity though, right? I’m looking at Polymarket’s election odds now, and they show Trump leading 67-33, while Kalshi shows 62-38. I feel like, hypothetically, someone could access Polymarket via VPN, or, even better, just have a friend in Spain or wherever take the other side of the bet.

Jack Such, Kalshi: I guess if you’re using a VPN, you can do whatever, but even then any “arb” would have a lot of friction. The last misconception that we’ve been seeing, in addition to, “The markets are being manipulated by large Trump bettors,” is, “The markets are being manipulated by foreign bettors.” Again, Kalshi doesn’t have any foreign users because we only operate in the US.

Jack Raines: Any closing thoughts on the prediction markets vs. polls debate?

Jack Such, Kalshi: Again, a big reason that polls differ from prediction markets is that the latter just reacts to information quicker. People make all sorts of arguments about manipulation or foreign entities affecting pricing, but sometimes the simplest explanation is the correct one: prediction markets, especially liquid, regulated markets, just work.