The American Express money machine keeps on rolling

Eat, sleep, swipe, repeat. Should we be worried about mounting credit card debt?

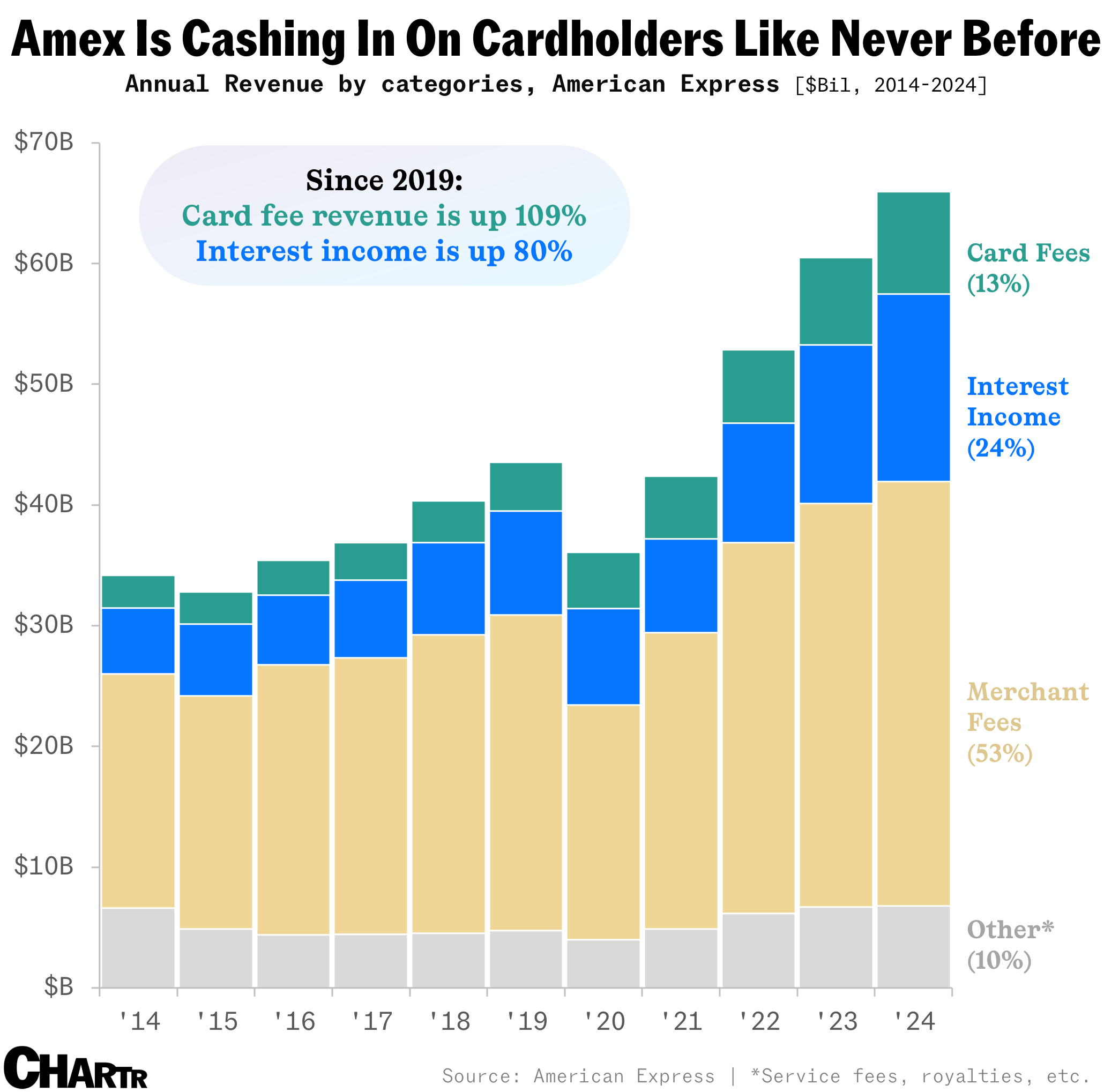

America’s love affair with credit cards is paying off — at least for American Express. Last Friday, the payments giant revealed that 2024 was its best-ever year, with revenue jumping 9% to $65.9 billion, translating to a cool $10.1 billion in net profit, up 21% year on year.

As usual, American Express made a large fortune from merchant fees, a source of income which grows nicely for the company as customers spend more. Those remained Amex’s largest revenue source. However, its recent growth isn’t just about people swiping; it’s more about signing up cards and stacking debt.

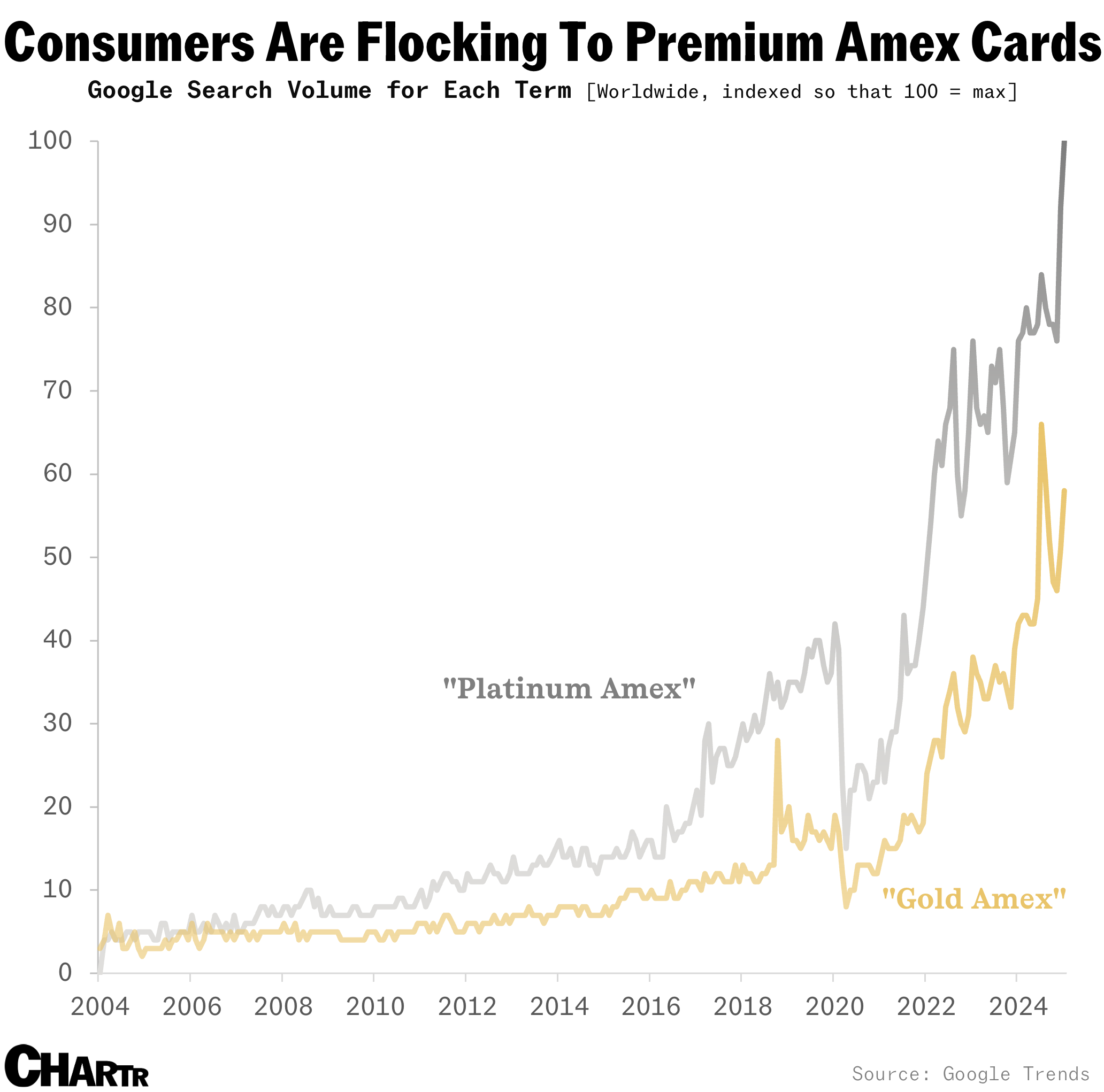

Last year, the company raked in a record $8.4 billion in card membership fees, a 16% rise from the previous year and more than double what it made in 2019, as customers forked out hundreds of dollars for the ability to produce an Amex Gold, Platinum, or — if you’re a serious high roller — Centurion (Black) card. Indeed, despite repeated fee hikes, Amex saw a record 13 million new card acquisitions last year.

And those weren’t all baby boomers looking to spend the kids’ inheritance: 75% of new Platinum and Gold accounts were opened by Gen Zers and millennials in 2023, as the flashy metal cards became something of a status symbol, allowing cardholders to flex their ability to afford the steep $695 and $325 annual fees and enjoy lifestyle perks like dining credits, lounge access, and first-class flights.

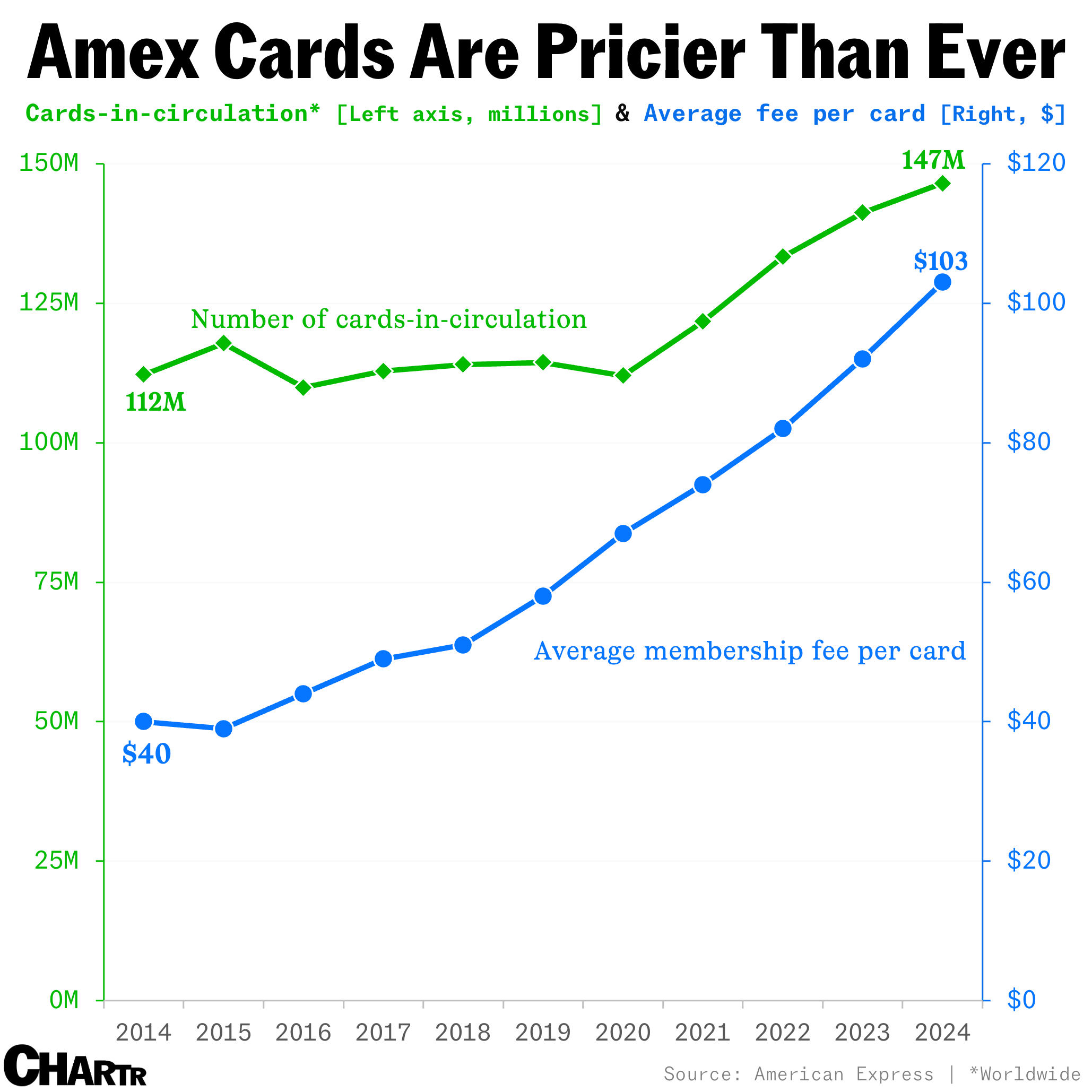

These young, affluent cardholders are paying more than ever.

Over the past decade, the average fee per card has more than doubled, from $40 in 2014 to as much as $103 in 2024, alongside the rising number of cards in circulation. With its cards getting pricier — and more customers flocking to pay these fees — it’s no surprise the 174-year-old company is hitting new financial heights, with its stock up 59% in the last 12 months.

Yes, strings attached

Customers with fat wallets are great for Amex, but, interestingly, what’s driving Amex’s top line even more than these wealthy customers are those falling behind on zeroing out their monthly balances. The company pulled in $15.5 billion in net interest income last year — up 18% from 2023 — as cardholders carried higher revolving loan balances (unpaid credit card debt that rolls over month to month).

Indeed, net interest income has been Amex’s fastest-growing revenue source since 2022, outpacing other categories with year-over-year increases of 28%, 33%, and 18%, respectively. It’s not just Amex that’s cashed in on higher interest rates, either: JPMorgan Chase, Capital One, and Discover all reported rising interest income fueled by swelling credit card debt, according to The Wall Street Journal.

But, while charging more interest is generally good for American Express, it also reflects a concerning reality: Americans aren’t just spending more — they’re paying off less.

Interest never sleeps

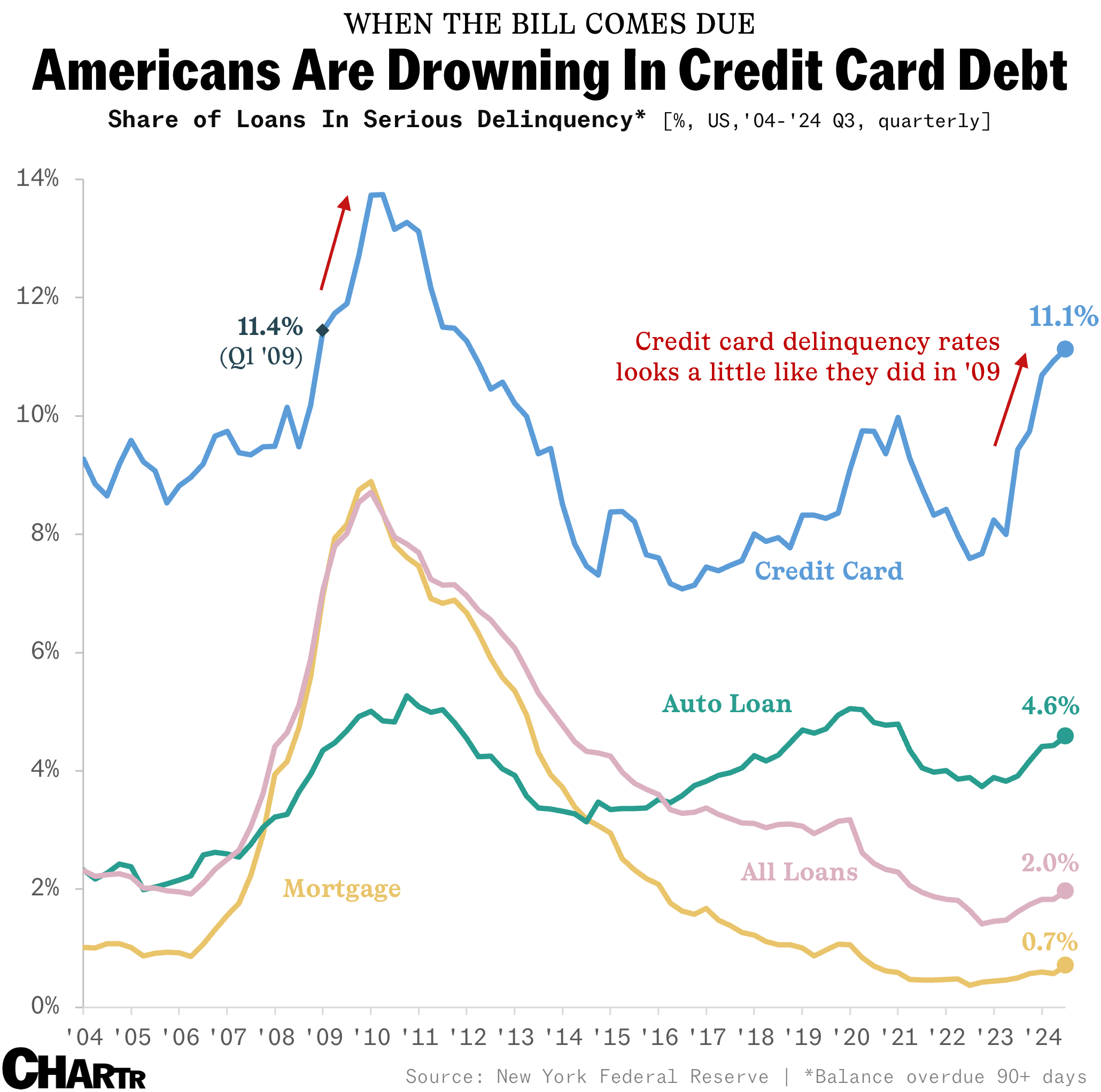

It’s generally not good news when you look at a financial chart and think “oh, that looks a bit like 2009,” but, according to data from the New York Fed, serious delinquencies (90-plus days overdue) are rising faster for credit cards than for any other loan type, including car loans and mortgages. As of Q3, 11.1% of credit card balances were delinquent, exceeding the 8.3% prepandemic level and edging closer to the ~12% seen during the 2009 financial crisis.

At the same time, data from the Philadelphia Fed reveals that the share of credit card accounts making only the minimum payment reached a 12-year high in Q3 2024. Furthermore, revolving credit balances have surged more than 50% since mid-2021.

Why are Americans struggling to pay?

Of course, we can blame the “i” word. Persistent inflation cornered the Federal Reserve into raising rates to try and cool price rises. That is, of course, the natural thing to do, but it doesn’t stop the cost of borrowing from going up at a time when some households are already struggling — and some people had nowhere to turn but credit cards to get by.

According to consumer polling firm CivicScience, more than 40% of Americans used credit cards to cover basic necessities like groceries and utility bills in October. With average credit card interest rates hovering around 20%, many are falling deeper into debt — which, ironically, has been a boon for companies like American Express.

So, are we strapping in for the 2008-09 crisis part 2, when mounting debt threatened the entire economy?

The good news is that a huge credit bill just doesn’t threaten the economy in the same way mortgages do. While hitting a record $1.17 trillion in Q3, credit cards still make up only 6.5% of total US household debt, per New York Fed’s data, a relatively small slice compared to auto loans (9%) or mortgages (70%). Meanwhile, Americans’ net worth is at an all-time high, buoyed by strong stock market gains and rising home values.

As for Amex, its own delinquency rates remain stable and below prepandemic levels, per last week’s earnings call. And with its premium-focused customer base, the company is largely insulated from the worst of the credit crisis.

But here’s the catch: the swipe-and-struggle dynamic isn’t going anywhere for those at the lower end, whose “credit reliance is up and savings rates are down,” according to Wells Fargo’s January report. This “disheartening truth” will only deepen this year — no matter how much it milks the plastic-and-metal credit empire.