The American economy in 4 charts

A lot of economic data is looking pretty good... but a lot of America doesn’t care after 3 years of inflation

Through the looking-glass

A recent Harris X Guardian poll made for some striking reading for those of us who spend our days buried in data. According to the survey, the majority of Americans believe the nation is currently in a recession (it’s not), 49% think the S&P 500 is down for the year (it’s up 11%), and the same percentage believe unemployment is at a 50-year high (again, it’s not).

It would be easy to dismiss the survey, but if a significant number of Americans feel the economy isn’t working for them, we have to ask: what’s going on?

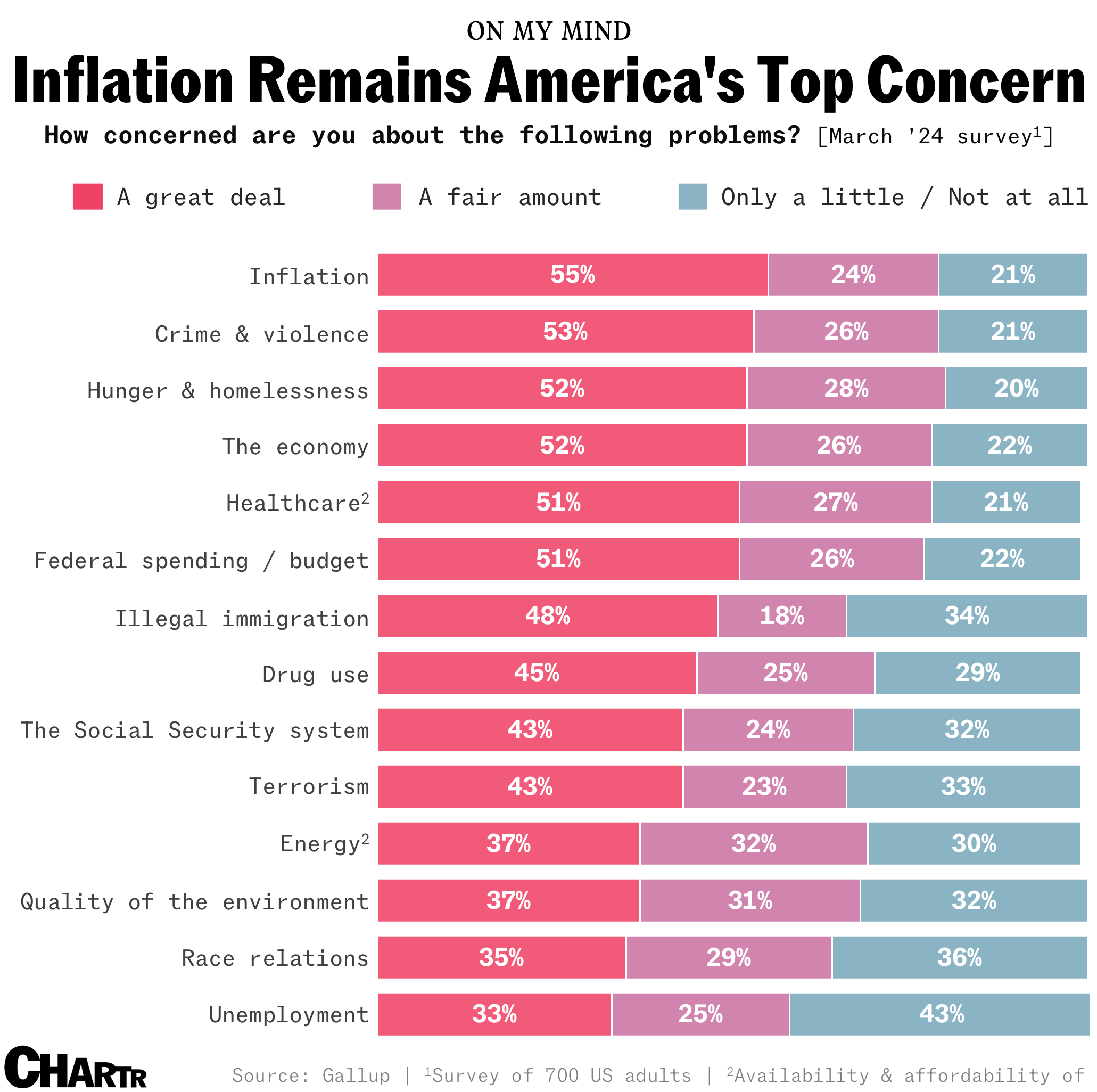

The simplest explanation is that most of us are bad at gauging how a $30 trillion economic machine is faring. So, we focus on our own financial situation — and on a personal level, many people are feeling the strain because of the one elephant in the room that just won’t go away: inflation. Indeed, a Gallup poll from March found that inflation continued to outrank crime, healthcare, terrorism, energy, the environment, drug use, and many other topics as America’s top concern.

Sticky downwards

Arguably the biggest problem is that economists tend to focus on the bleeding edge of the economic data, often looking not just at the level of inflation, but estimates of its trajectory — is it accelerating, decelerating, etc. But, as one astute investor posted on X (formerly known as Twitter)… that’s not what normal people care about.

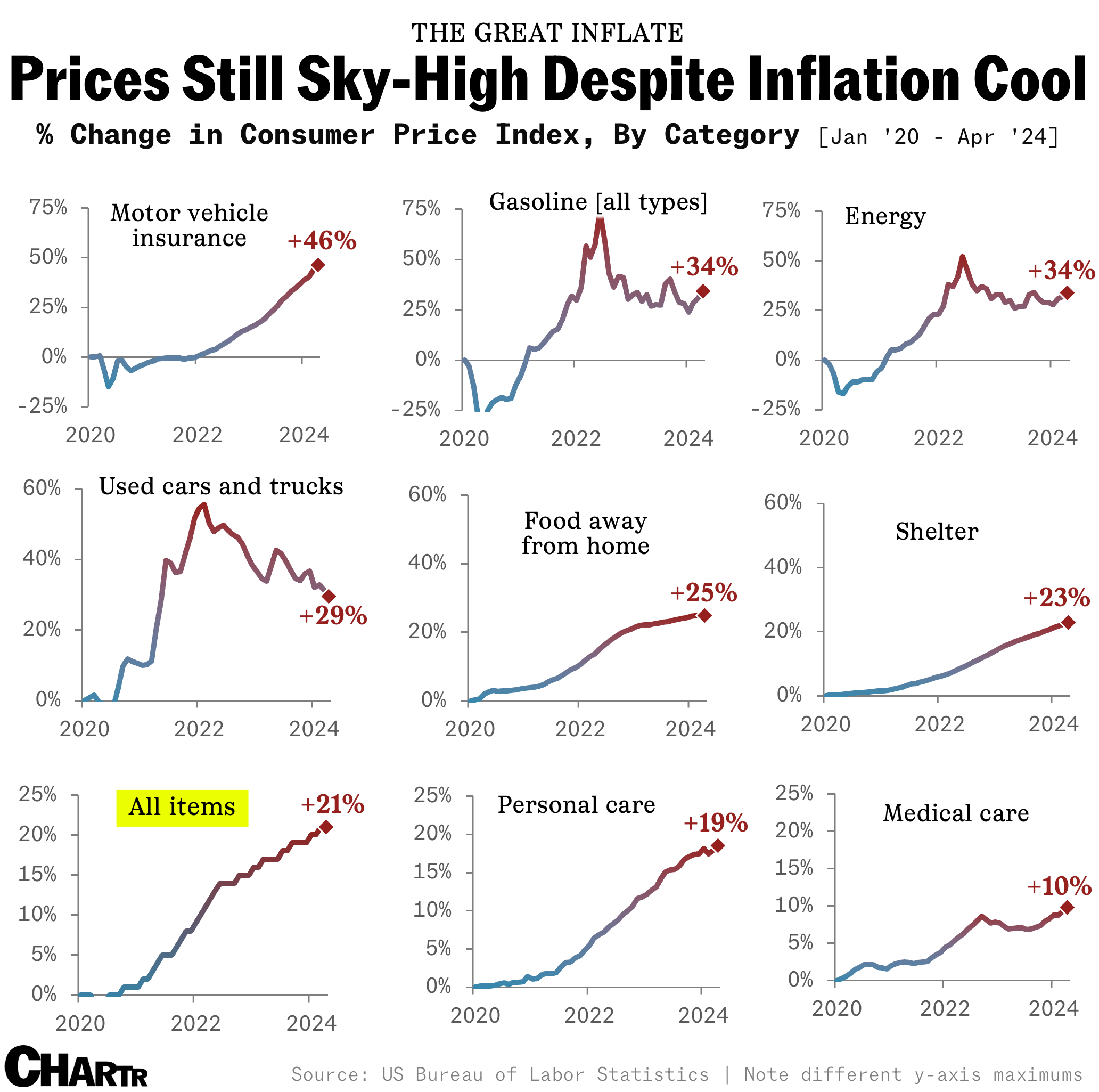

If inflation is 10% annually for 2 years, and then drops to 5% in the third year, economists and investors may rejoice at the progress, but almost no-one else will blink. That’s because the cumulative effect of that sequence of events is a 27% increase in prices over 3 years… which people notice when they buy butter, insurance, hot dogs, or gas. That example is not a million miles away from what has actually happened.

Many prices are now 20-30% higher than they were in 2020 — and, while inflation has cooled substantially, to just 3.4% as of the latest CPI report, that still means costs are rising. McDonald’s went so far as to comment directly on its own price rises, after videos of expensive Big Mac meals, including one for $18, went viral. McDonald’s says its prices are up 40% in the last 5 years, reflecting a broader rise in the cost of labor, paper, and food.

USA #1

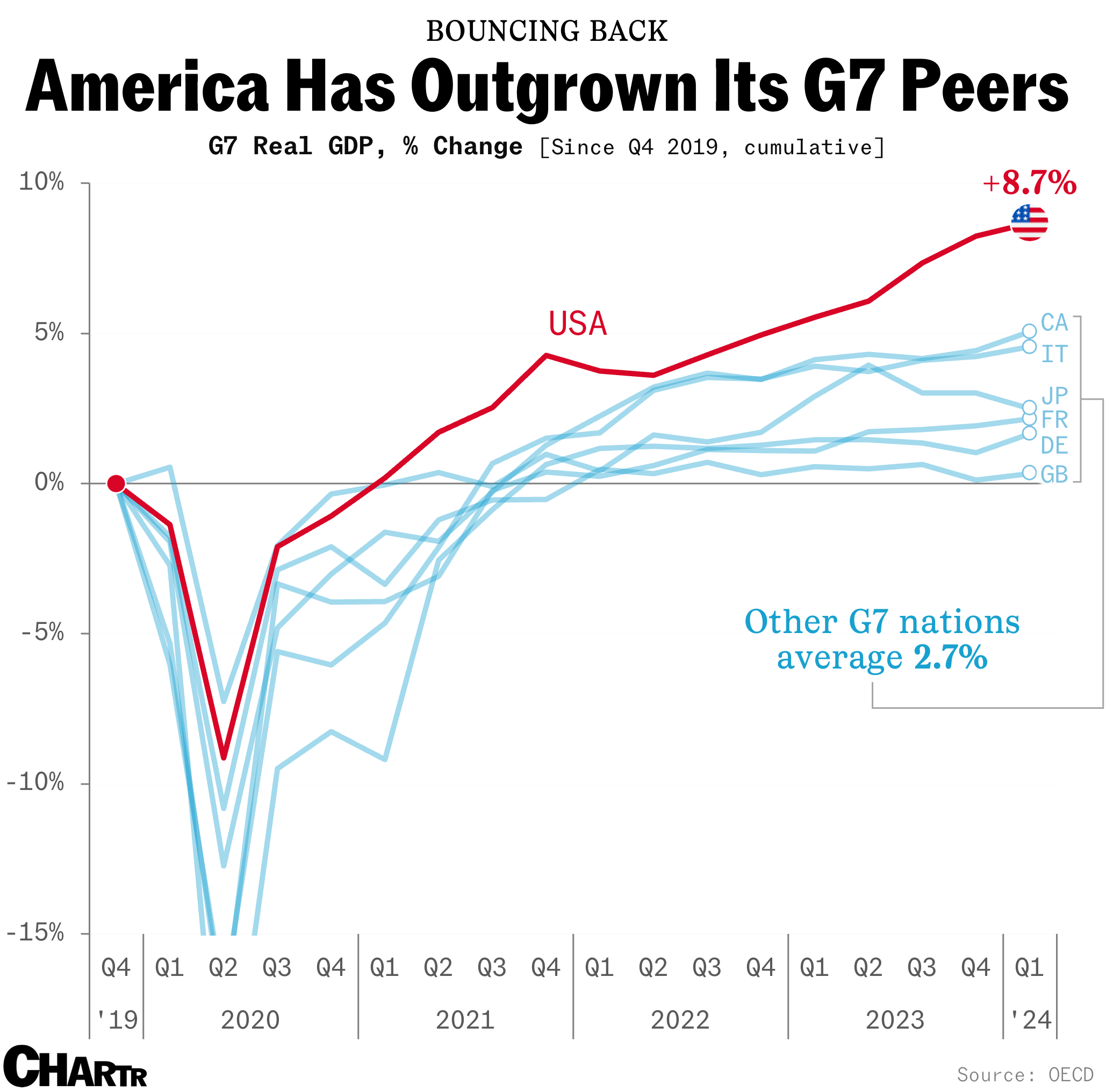

Another reason economists might have a rosier view of the American economy than the general public? A global perspective. Indeed, the US has seen real GDP grow by nearly 9% since the pandemic began, by far the strongest of any of its G7 peers, which have averaged only 2.7%. Canada’s economy has been the next best in the group of seven, growing 5%.

The hiccup in the US recovery was a brief two-quarter GDP dip at the start of 2022 — fitting the classic recession definition. But, the National Bureau of Economic Research, which makes the final decision, decided not to classify it as one. Furthermore, despite all the talk of mass layoffs and automation, US unemployment has remained below 4% since the beginning of 2022, near historically-low levels.

In contrast, the UK economy has been much weaker than America’s. Indeed, British GDP is barely larger, in real terms, than it was at the end of 2019… just as the electorate gears up for a July 4th election.

The great American consumer

Despite sky-high interest rates and inflation, good old-fashioned consumer spending – the biggest slice of the US economic pie – has been nearly unstoppable for more than 3 years, with people continuing to splurge. However, very recently, there have been signs that some consumers might be starting to crack. Retail sales growth halted abruptly in April, and recent earnings from Target and Walmart suggest that lower-income consumers are starting to struggle, with Fortune reporting “a shift from spending on wants to needs”, with similar sentiments shared by executives at other consumer companies.

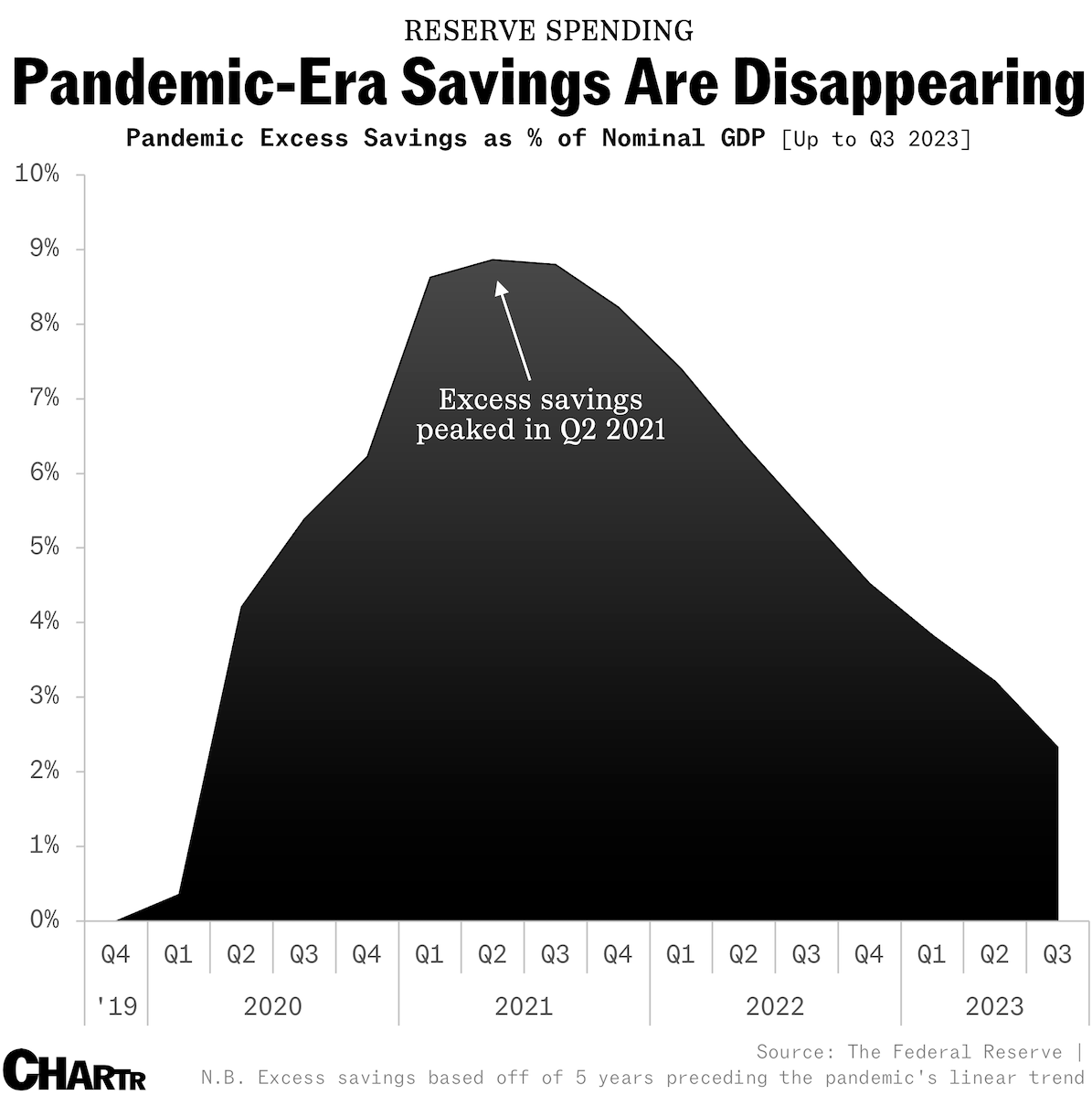

In recent years, when consumers felt the pinch, many had pandemic-era savings to dip into thanks to stimulus checks, enhanced unemployment benefits, tax credits, and the fact that there wasn’t much to spend your money on during lockdown. This influx of cash bolstered our bank accounts significantly: one economic model estimates that America banked excess savings worth a staggering ~9% of nominal GDP during 2021.

But, that buffer is now disappearing, with excess pandemic-era savings now sitting at just above 2% of nominal GDP and falling according to estimates from the Fed at the end of last year. More recent analysis from third-parties suggests that those excess savings are now all gone, leaving consumers more vulnerable.

Average Joes vs. CEOs

Interestingly, while consumers are beginning to show signs of strain, CEO confidence tells a different story. Indeed, executives remain positive about the economy, with pandemic-era supply constraints now a thing of the past and earnings continuously exceeding expectations. The positive in all this for the Average Joe, as Luke Kawa explains, is that if this corporate optimism continues to translate into more business investment, new employment opportunities are usually close behind. But, employment opportunities tomorrow, while prices rise today, is a hard slogan to sell. At least the stock market keeps going up.