The fastest-growing part of Tesla’s business isn’t selling cars

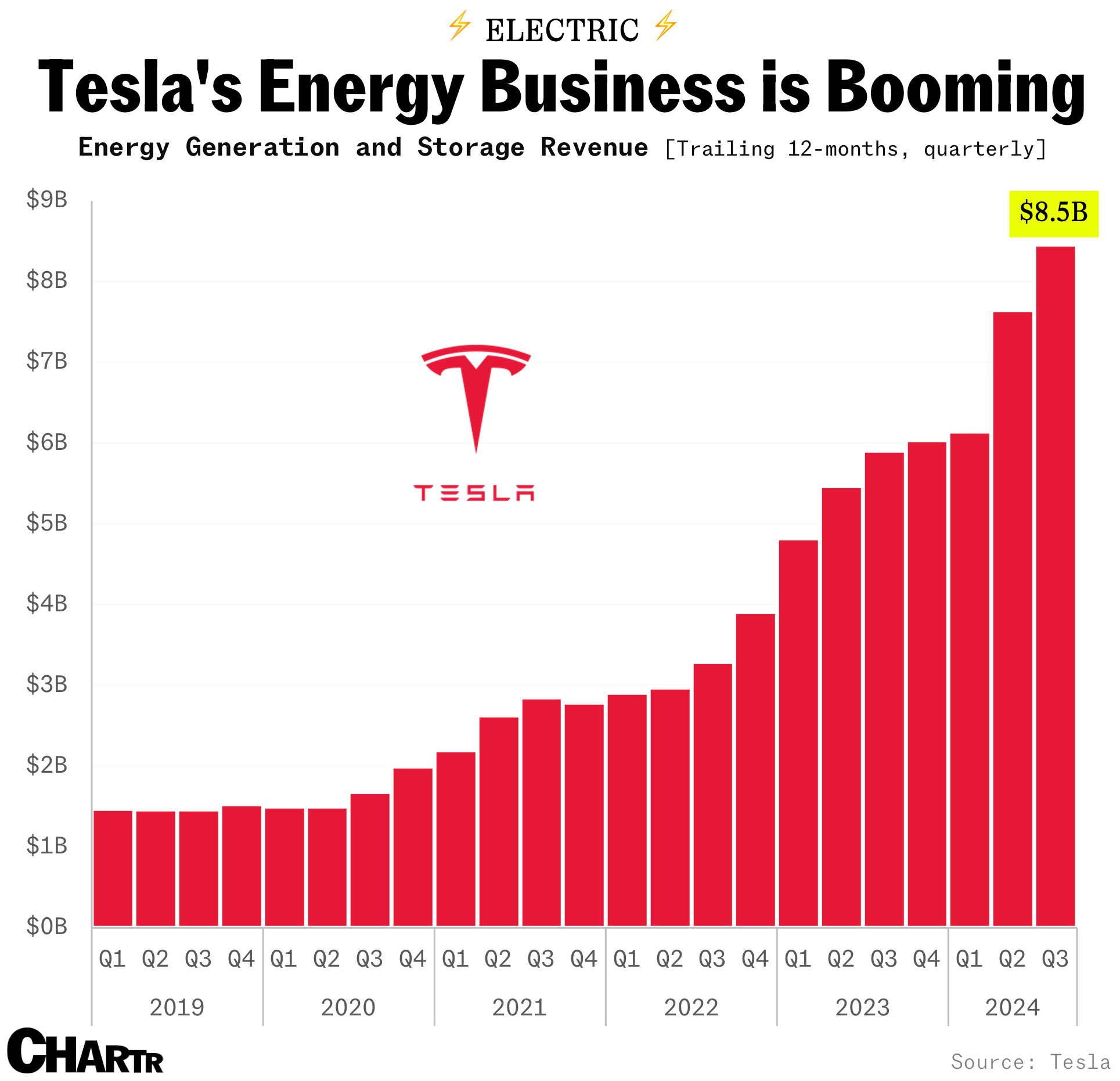

The lesser-known energy generation and storage business was juiced up in Q3, delivering a 31% gross profit margin

Elon Musk is a lot richer this morning than he was last night, as Tesla stock is soaring in early trading after reporting better-than-expected profit margins, despite a miss on revenue, in its Q3 earnings.

The closely watched gross margin came in at 19.8%, way ahead of expectations for a print of 16.8%, as investors get over the fact that revenue from actually selling cars has slipped into neutral, rising just over 1% in the last year.

Externally, the company is increasingly billing itself as anything but a car company, with robotaxis and humanoids key to its future (maybe). But, while those didn’t have any explicit impact on the company’s actual numbers this quarter, what is firing on all cylinders is the company’s energy-generation and storage business, which reported growth north of 50%, by far the best of Tesla’s divisions.

Not only is the energy-generation and storage business growing rapidly, but on a relative basis it’s also significantly more profitable for Tesla than selling cars: the company reported a 31% gross profit margin from its energy efforts, nearly double the 16% from automotive sales. It’s worth noting, of course, that nothing beats the $739 million worth of pure profit from automotive regulatory credits.

The company’s energy business ranges from Megapack, a product aimed at large-scale utilities deployment, to products geared for end customers in smaller households like the Tesla Powerwall, and it also sells and installs solar-power systems.

Demand for Tesla’s energy-storage solutions is expected to only expand, especially with growing installations of renewable-energy sources like wind and solar, which can be volatile and require battery solutions to store the excess energy when its not blowing hard enough or sunny enough. The outlook for EV charging services like Tesla’s Supercharger is also bright, with America’s EV infrastructure struggling to meet demands and the ambitious roadmap to 2030.

CEO Elon Musk also said on an earnings call that car sales would likely get back to growth next year, predicting that Tesla’s deliveries could rise 20% to 30% next year. Of course, many Elon Musk predictions haven’t come true.