BNPL loans will now count toward Americans’ credit scores

While it’s a chance to build credit for some, it might penalize those already on shaky ground.

On Monday, Fair Isaac Corp., the company behind the FICO credit scores used by 90% of US lenders, announced the fall launch of two new scoring models that, for the first time, factor in “buy now, pay later” loans. The move gives lenders a way to assess a fast-growing form of borrowing that has long operated outside the reach of traditional credit scores and reports.

Why now?

Put simply, it’s just become too big to ignore. Per eMarketer, over 86 million Americans used BNPL services last year — nearly double the number in 2021 — with shoppers now relying on it for everything from groceries to travel to dining out. And, while it may have started as a niche option for luxury splurges, today the heaviest users aren’t the most financially comfortable.

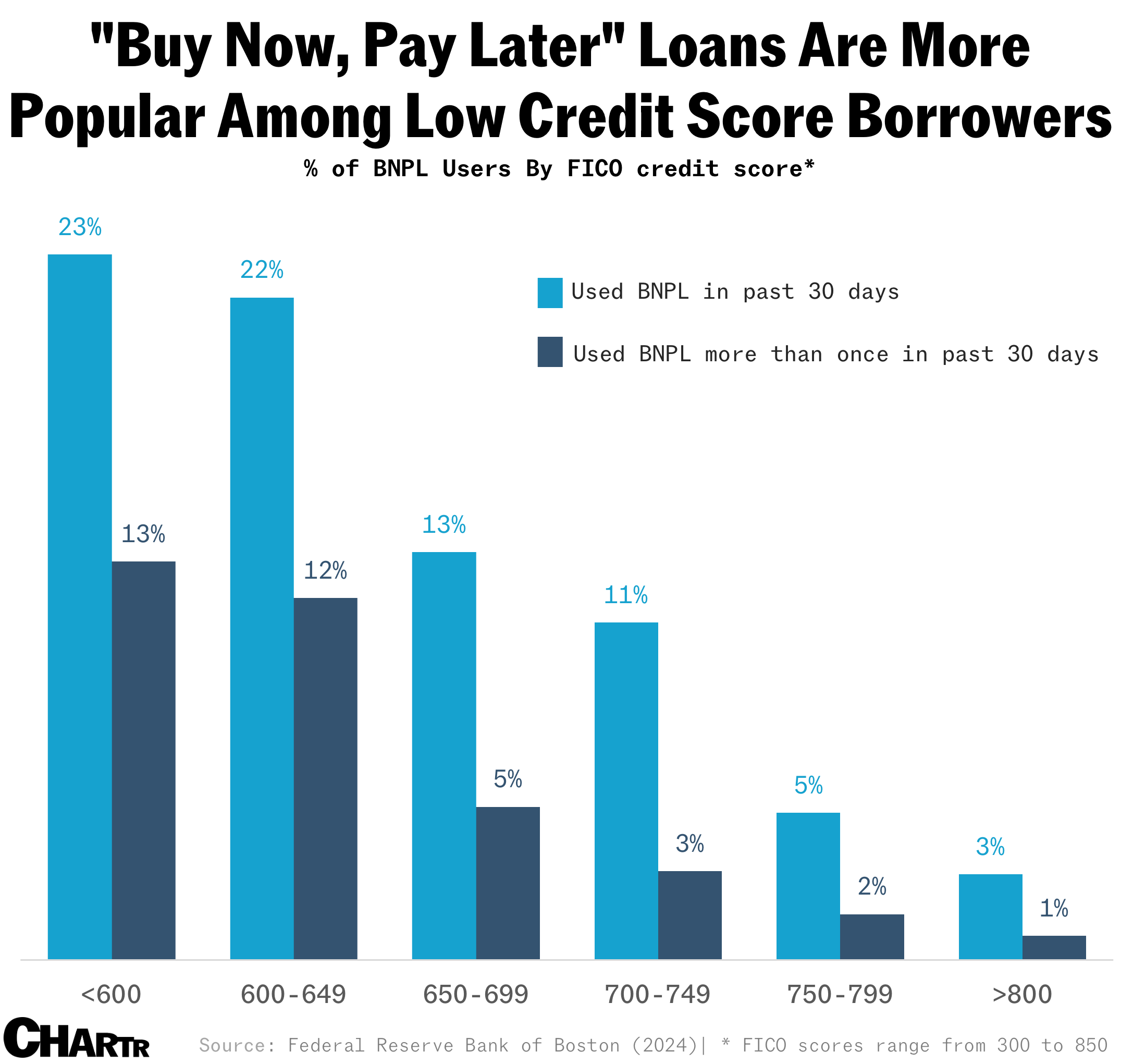

According to a 2024 analysis by the Boston Fed, nearly one in four Americans with FICO scores under 600 have used BNPL, compared to just 2.8% of the 800-plus club, those with near perfect credit. Meanwhile, a May report from the Federal Reserve found that 40% of low-income BNPL users paid late, compared to just 13% of higher-income households.

For people already on the financial edge, the new dimension to their credit scores may hurt more than help — though one FICO-Affirm study from February found that most heavy BNPL users didn’t see their FICO scores worsen once BNPL loans were taken into account.