.png?auto=compress%2Cformat&cs=srgb&fit=max&w=3840)

Battle of the sad desk lunches: Both Cava and Sweetgreen want to become the next Chipotle

But are we approaching peak slop bowl?

Three decades after the first Chipotle restaurant opened, the burrito chain became a 3,700-plus store giant, riding a wave of growing demand for food that ticks three boxes: delicious, nutritious, and expeditious.

Though the “nutritious” part of the equation is optional at Chipotle — it’s very easy to build a sour cream-laden 1,000-calorie burrito — the Mexican-inspired menu has since won millions of fans across the United States. Last year, the fast-casual chain sold more than $11 billion worth of burritos and bowls, and the company has a more than $77 billion market cap.

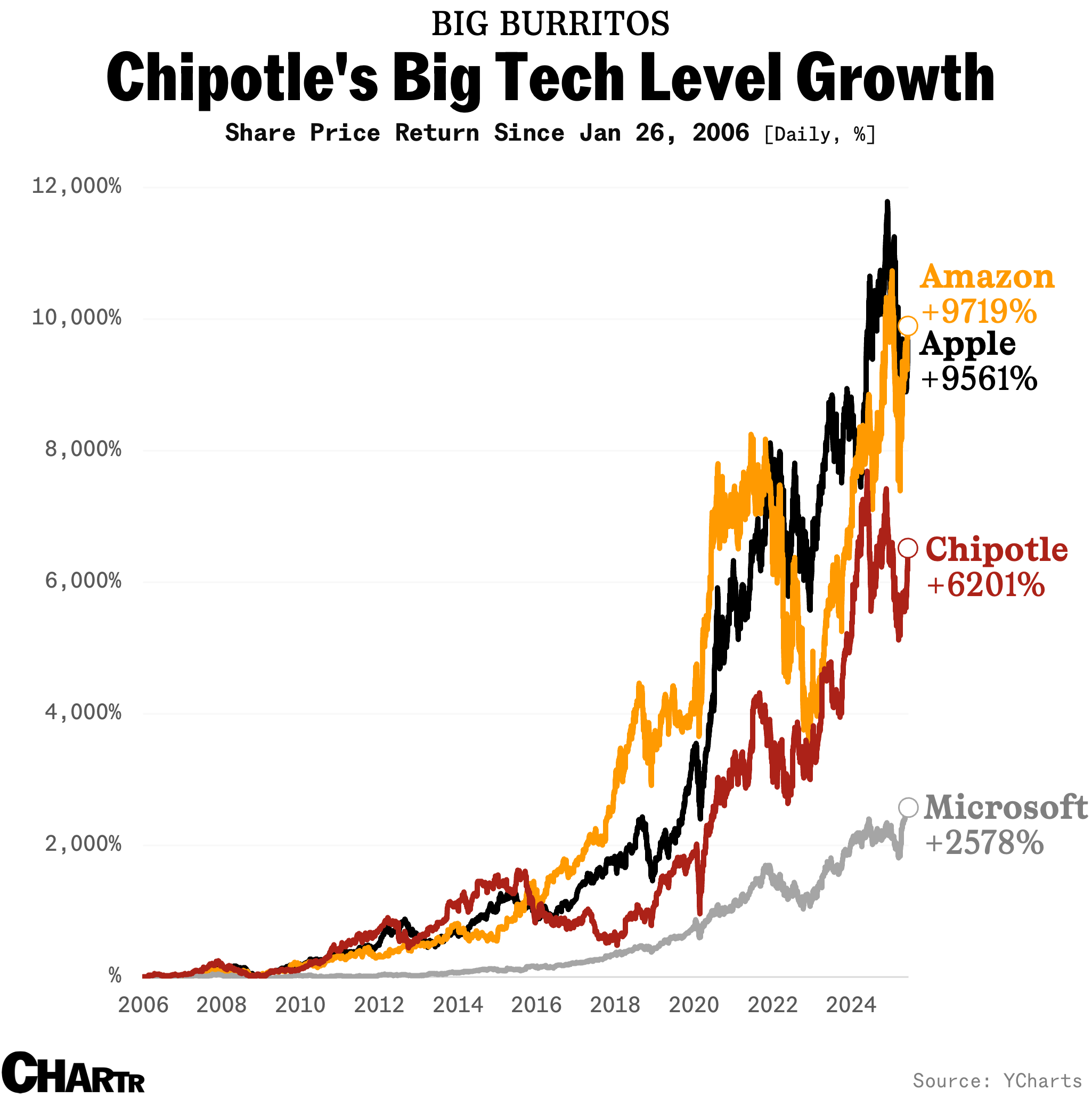

That success has attracted competitors. In the last few years, with piles of young professionals opting for a salad and even larger piles of capital willing to pour into the sector, healthy, premium chains have expanded aggressively in a bid to chase the success of Chipotle — which has seen its stock soar more than 6,000% since going public in 2009. That’s a return usually associated with tech giants like Amazon, Apple, or Microsoft.

In particular, office workers are increasingly comfortable forking over $16 or more for a salad, as Chipotle wannabes like Cava (founded in 2006) and Sweetgreen (founded in 2007) hope to become the next major success story in the space.

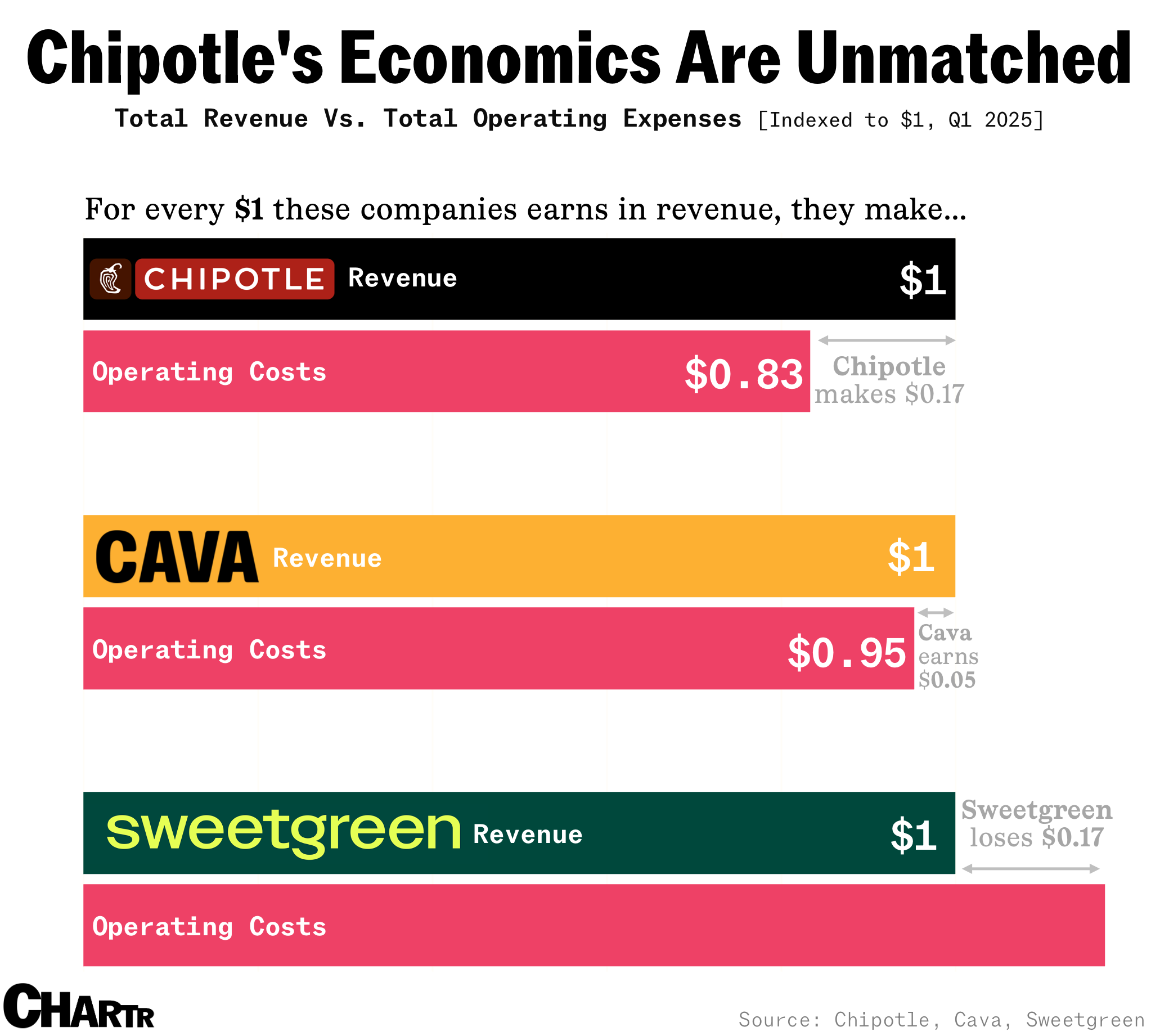

But as they enter their late teenage years, both Mediterranean-inspired Cava and salad-based Sweetgreen are struggling to fully emulate the Chipotle model. Both have eschewed the idea of franchises, just like Chipotle, choosing instead to run company-operated stores. But so far, neither have managed to match its high unit revenue, footprint, healthy profit margins, and low expansion costs.

However, of the two, Cava is undoubtedly winning the slop bowl battle so far.

Green with envy

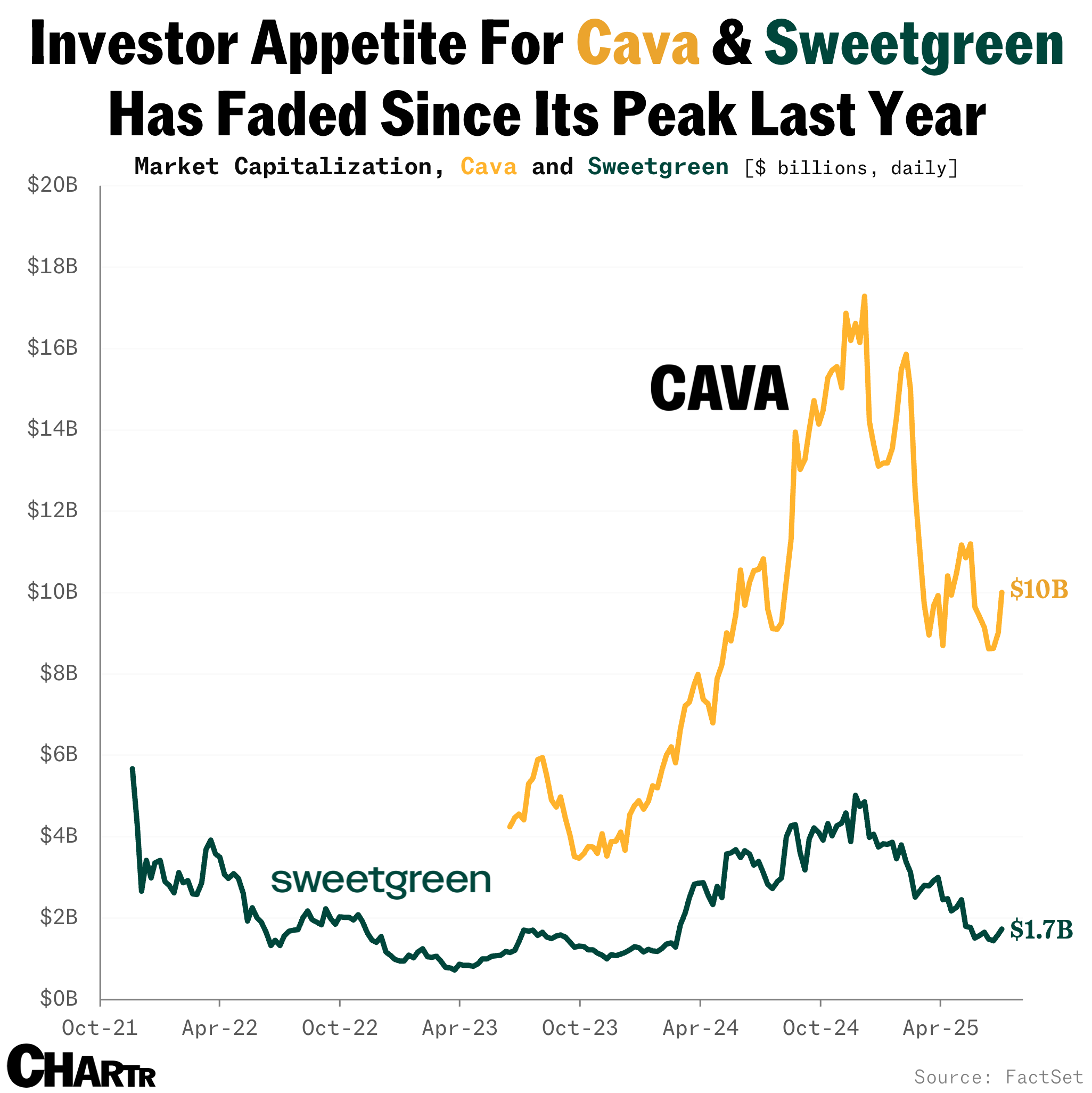

Since going public only two years ago, Cava has quickly become a fast-casual giant, with a market cap north of $10 billion, a valuation that’s only underpinned by some 382 stores. That means the market is ascribing a value of $27 million and change for every Cava restaurant. Walking into a Cava restaurant and thinking, “Yes, this one store is definitely a business worth $27 million!” is a little hard to grasp. But clearly the valuation is predicated on a lot more growth for the pita bread provider, with investors betting on its ambitious plans, which include operating 1,000 restaurants by 2032.

Wall Street isn’t shying away from making comparisons, with a clear “Cava is the next Chipotle” narrative in much of the stock’s bullish commentary — including KeyBanc, which launched its coverage of the stock at “overweight” last Wednesday, praising its “potential to define the category” of fast-casual Mediterranean food, just like Chipotle did for Mexican with its burritos and barbacoa.

But rival Sweetgreen hasn’t yet made it out of the red. Indeed, despite selling $15, $16, or even $17 premium salads, Sweetgreen remains a money loser. In its most recent quarter, the company racked up a $28.5 million operating loss, equivalent to a -17% operating margin — a considerable distance off from its rival Cava, which may not be stuffing Chipotle-sized profits but is at least ekeing out some kind of margin.

Peak slop bowl?

More recently, enthusiasm for premium fast-casual options, which are usually more expensive than fast food, has waned as some cash-strapped consumers have opted for value options.

That’s been reflected in the appetite of investors, too. The valuations of both Cava and Sweetgreen have come under pressure since their peak last year, falling 21% and 58% since the start of 2025, respectively. Sweetgreen actually reported that same-store sales had fallen 3.1% in its most recent quarter — a worrying decline for a stock that’s meant to be in growth mode.

So, without the raw economies of scale that a company like Chipotle can afford — which has nearly 10x as many stores as Cava and ~15x as many as Sweetgreen — how do you make your slop bowl company as efficient as possible?

You get the robots involved, of course.

Both companies are exploring robot chefs in hopes of slimming down costs. From automated pita bread and onion slicers to a salad assembly line that can churn out 500 bowls in an hour, which Sweetgreen execs have dubbed “Infinite Kitchen,” each company is experimenting with automation to boost their margins. One automated Sweetgreen location reportedly reached a 31% restaurant-level profit margin, way above the ~18% that the group reported most recently. That’s great on paper, but such a result also requires serious up-front investment, with the Infinite Kitchen system reportedly costing some $450,000 to $500,000 per unit.

The sad desk lunch brands have also been dipping their toes into the dinner business. They’ve both introduced steak to their lineup, Cava has diversified its menu with pita “Peter” chips, and Sweetgreen launched fries in March in a bid to widen its appeal beyond salad-obsessed professionals.

Steak, fries, robots — and, of course, keep growing your store base at all counts. Maybe that will be the formula to emulate Chipotle-like success.