Goldman Sachs: Megacap tech stocks’ relative valuations are near their 2022 lows

With Microsoft and Meta jump-starting the megacap tech reporting period this Wednesday, Goldman Sachs equity derivatives and flows specialist Cullen Morgan commented on a relative rarity for the cohort of behemoths: they’re not really that expensively priced. He wrote:

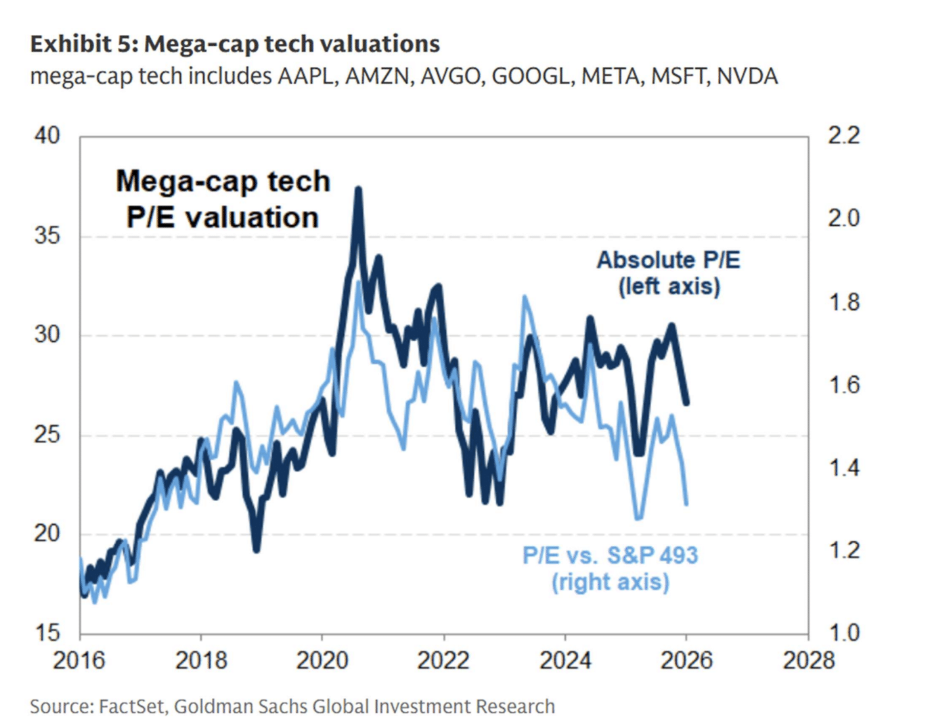

“Valuations of the mega-cap tech stocks have declined substantially in recent months. The group now trades at a forward P/E of 27x, which ranks in the 59th percentile relative to the past decade. Relative to the rest of the S&P 500, the 31% P/E premium ranks in the 24th percentile during the past 10 years...

While elevated FCF multiples leave room for further de-rating, the current PEG ratio of 1.4x nearly matches the trough from late 2022.”

This is exactly why we suggested keeping an eye on hyperscaler valuations coming into this year, particularly this divergence between price-to-earnings ratios and price-to-free cash flow ratios, as a way to monitor whether profit expectations surrounding the transformative potential of AI were getting extrapolative or not:

“One way to square this circle between elevated, not crazy forward valuations based on one metric and sky-high ones based on another is to conclude that the lack of runaway forward price-to-earnings ratios suggests that the market does continue to have some skepticism about the long-term earnings power associated with all these capital outlays.

Less doubt would equal higher valuations and higher stock prices. No doubt and unbridled optimism about how much these first movers in AI will reap rewards for years if not decades to come… that’s how we really get a bubble.”

So far in 2026, the market has been squarely focused on rewarding companies that are poised to benefit from near-term shortages and excess profit opportunities brought about by the AI boom, rather than its potential long-term winners. We’ll see if that changes as megacap tech leaders start to step up to the plate this week.