Even after the DeepSeek and AI meltdowns, Wall Street's still sticking with its lofty Nvidia price targets

It might only be March 17, but for Nvidia investors, the year so far might have felt like a lifetime.

Everything happens so much

First came the DeepSeek freak-out, a violent sell-off sparked by a Chinese AI model that was reportedly trained for a fraction of the cost of its Western rivals. Then came tariffs, an ongoing growth slowdown scare, and a sharp reversal in the fortunes of momentum stocks — almost all of which were heavily associated with an AI trade predicated on a continued “capex orgy” as Big Tech companies plan data centers the size of large cities.

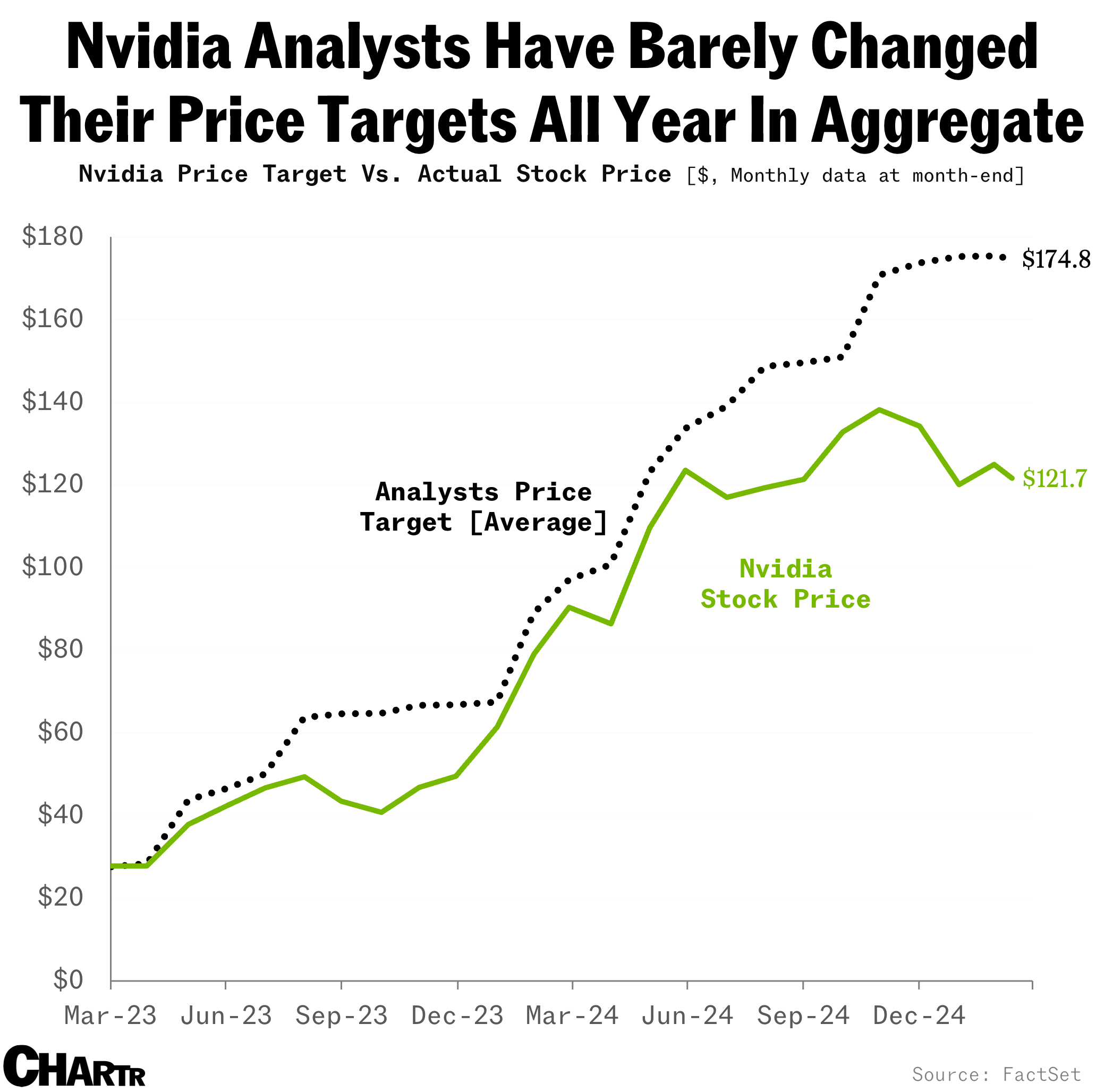

So, given all that’s happened this year, how have Wall Street analysts changed their views on Nvidia? Well... they haven’t really. At least not in the aggregate.

Data from FactSet reveals that the average (mean) price target for Nvidia at the end of last year, before any of those headlines hit the tape, was $173.81. Today it’s $174.79, or 0.6% higher.

It’s plausible, if a little embarrassing, that some analysts simply haven’t gotten around to rerunning the numbers in the wake of this latest sell-off. But clearly many of the analysts — and there are nearly 70 of them in total — believe that the fundamental equity story remains unchanged for Wall Street’s most-watched stock, even as the world around it shifts. At the company’s full-year results, Nvidia beat on both the top and bottom lines, though, with the rollout of its Blackwell GPUs progressing steadily, gross margins might compress slightly in the short term.

After a volatile last seven days or so, the next big catalyst for the stock could come quickly, as CEO Jensen Huang takes the stage tomorrow at GTC 2025, Nvidia’s biggest conference of the year. Investors will be on the lookout for mentions of 2026 demand and any updates on its next-gen chip Vera Rubin (named after the astronomer).

Related reading: 73 Wall Street analysts cover Amazon, there are 72 on Meta, and 66 write about Nvidia — how many do we need?