CoreWeave’s attempt to buy Core Scientific is going down in flames

The last time CoreWeave tried to buy Core Scientific, management didn’t approve. This time, it looks like shareholders don’t.

CoreWeave’s last attempt to buy Core Scientific in 2024 failed because management thought the bid was too low.

Its July offer of an all-stock transaction then valued at about $9 billion was good enough to convince Core Scientific’s top brass, but doesn’t look to be enough to convince the true owners of the company: its shareholders.

Shares of Core Scientific are trading for much more than the terms of the agreement say they’re worth heading into Thursday’s shareholder vote on the transaction, strongly suggesting traders are pricing in either a rejection of this proposal or a last-minute boost to the offer.

Major shareholders and proxy advisory firms are publicly opposing the union. Two brokerages upgraded the stock to “buy” from “hold” this week, with both analysts citing the unlikelihood of this transaction going through as a cause for their rosier view.

An initial concern with this deal was the lack of a so-called collar: since the transaction would be completely in CoreWeave stock, with each Core Scientific holder poised to receive 0.1235 shares of CoreWeave, what they’d ultimately receive was down to the whims of what the market felt about CoreWeave at the time this closed (or not!). As we discussed, Core Scientific became a slave to CoreWeave’s low float, which was going up, but with no easy way for its owners to protect the value of their position because of the high cost of shorting CoreWeave, which would have been necessary for any arbitrage play.

Shares of the neocloud company are down 14% since initial reports of its renewed plan to buy Core Scientific surfaced and off 17% since the agreement was announced.

The deal premium vanished decisively as CoreWeave’s post-IPO lockup expired, which unleashed a wave of pent-up profit taking and made more shares available to be shorted, and turned starkly negative as key investors and advisory firms voiced their disapproval.

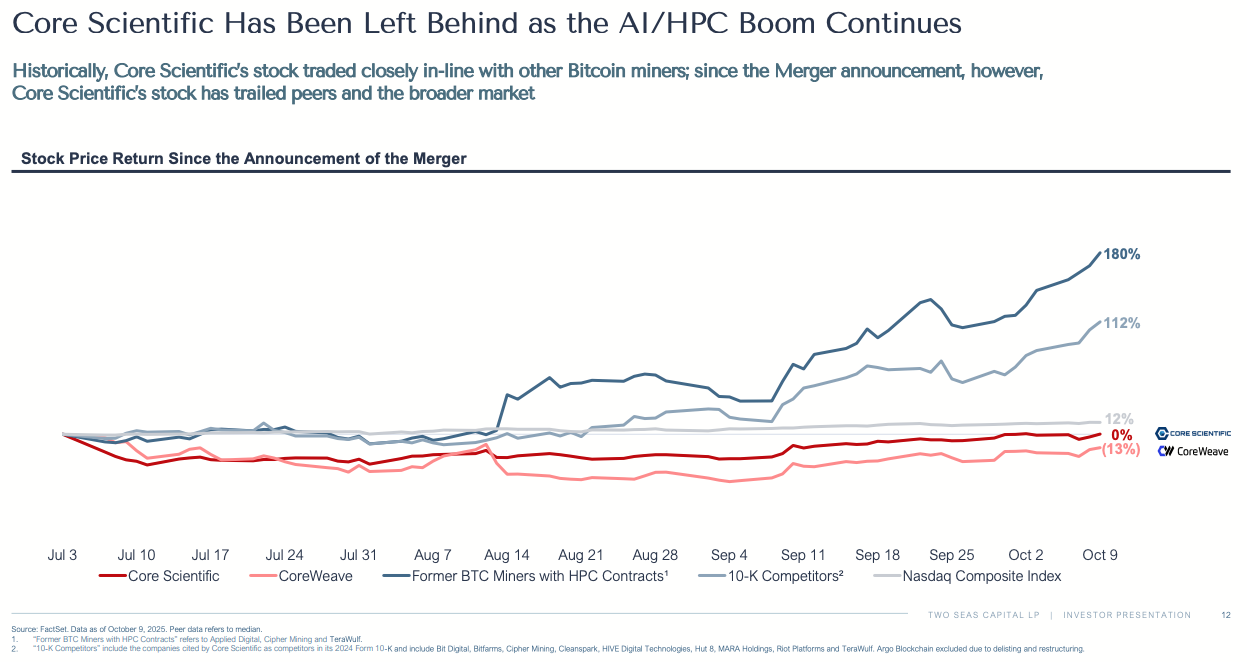

On August 7, Two Seas Capital issued a statement opposing the deal, and followed that up with a presentation earlier this month detailing its concerns. The investment fund, which is one of Core Scientific’s biggest shareholders, argued that rather than being a hot-air balloon for shares of Core Scientific, CoreWeave’s offer has actually been an anchor, causing its returns to severely lag other bitcoin miners turned data center companies that offer high-performance computing services. In the days that followed, Gullane Capital — another major Core Scientific holder — also said it would be voting no.

On October 21, two independent proxy advisory firms, Institutional Shareholder Services Inc. and Glass Lewis & Co., also came out against the proposal.

CoreWeave and Core Scientific management teams, for their part, remain strongly in favor of a tie-up. Core Scientific recommended voting in favor of the transaction, noting that it had been “unanimously determined” by its board of directors as providing “meaningful upfront premium and upside opportunity.”

CoreWeave CEO Michael Intrator has been resolute that there will be no bump to his offer, telling Bloomberg earlier this month, “Really under no circumstances will we readdress the bid that we put out,” with the company reiterating that stance in a press release last week.