OpenAI isn't selling equity — it's selling shares of profits that may never come. Investors can’t get enough.

OpenAI's weird corporate structure has investors and employees owning shares of future profit distributions instead of traditional equity.

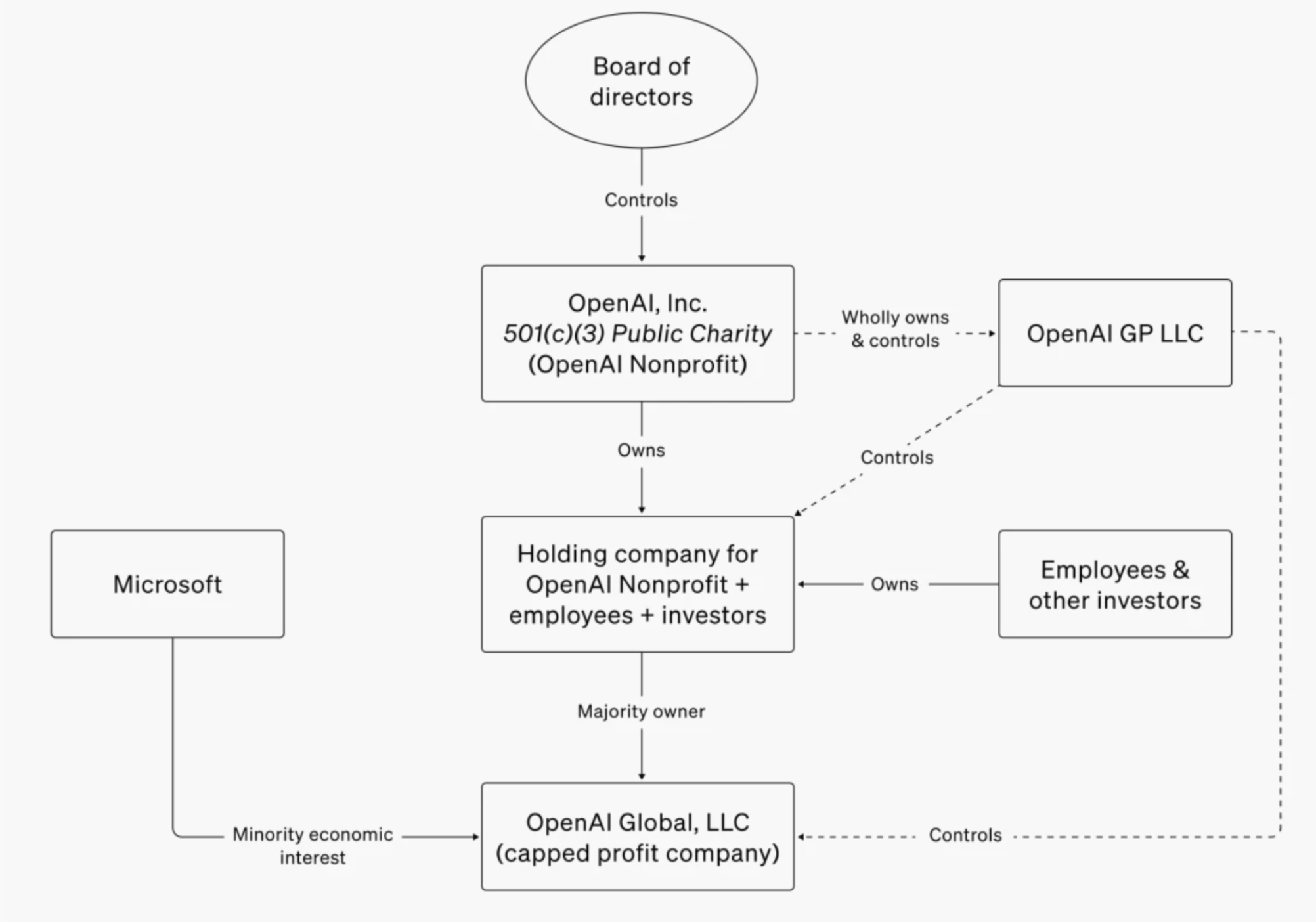

Much has been written about OpenAI’s unique corporate structure: basically, OpenAI was initially a nonprofit, and the company wanted to raise money to fuel more capital-intensive projects, but it didn’t want the pursuit of financial gains to overshadow its nonprofit mission of “safe AGI that is broadly beneficial.”

The board’s solution was to create a for-profit subsidiary that would be controlled by the nonprofit parent company through a separate manager entity, OpenAI GP LLC. The for-profit unit can raise capital from outside investors (such as Microsoft), but there are caps on the maximum financial returns for investors and employees in the company’s for-profit arm. Here’s a diagram of OpenAI’s current structure:

Despite the weird corporate structure, OpenAI has no problems raising outside capital, with the company now in talks to raise “several billion” dollars from Thrive Capital, Microsoft, and other investors in a funding round that would value it at more than $100 billion. The Wall Street Journal also noted that “one or more current OpenAI stockholders have been negotiating to sell their shares at a price that would value the company at $103 billion.”

However, due to OpenAI’s weird corporate structure, this isn’t a normal fundraise. Investors don’t actually own OpenAI equity — they instead invest money in its for-profit subsidiary, and they are “entitled to a share of the entity’s profits.”

OpenAI’s “equity” compensation for employees is structured similarly. Per employee compensation site levels.fyi, OpenAI employees are offered “profit participation units,” or PPUs, instead of traditional restricted stock units (RSUs) and stock options. These PPUs are functionally similar to “profit interest units,” or PIUs, a form of equity-like compensation sometimes offered by private companies.

Regarding PIUs, compensation platform Carta said:

There are very limited requirements for profits interest units, though a liquidation threshold is often assigned to profits interests on their grant date, meaning that the LLC has to achieve profits at or above a certain amount for the profits interest to participate in exit proceeds.

Levels.fyi also noted:

What if the company never turns a profit or is not currently turning a profit? Well, if you’ve held on to the PIU then you won’t redeem any value from it. That doesn’t mean the PIU doesn’t have any value per se. Someone that expects the company to generate a profit eventually may value the PIU and be willing to purchase it from you.

Back to OpenAI’s compensation structure. OpenAI’s PPUs entitle their holders to a percentage of the company’s future profits, not an equity stake in the company. This, of course, assumes that the company will, at some point, turn a profit.

More from Levels.fyi on OpenAI’s comp:

When giving candidates an offer, OpenAI will state what they believe to be the value of PPUs given. These PPUs vest evenly over 4 years (25% per year). Unlike stock options, employees do not need to purchase PPUs. PPUs all have the same value associated with them and, during a tender offer, investors purchase PPUs directly from employees. OpenAI makes offers and values their PPUs based on the most recent price investors have paid to purchase employee PPUs…

It’s important to reiterate that the PPUs inherently are not redeemable for value if OpenAI does not turn a profit. That said, there are investors that have been willing to pay for these PPUs and that’s where the value being told to candidates is derived from.

The Information noted in July that OpenAI is far from profitable, and it could lose as much as $5 billion this year due to heavy data processing costs for its large language models and hefty price tags to attract top talent in a competitive job market, and the company is reliant on outside capital to continue fueling its growth. But that capital isn’t buying a stake in the company, it’s buying the right to future profit distributions (of which Microsoft controls 49%) and the company is far from showing any profits.

While equity of an unprofitable startup could still have value (unprofitable companies can still IPO or be acquired. Uber IPO’d without having ever turned a profit, for example), PPUs for a company that never turns a profit have zero intrinsic value. If you own OpenAI PPUs, and the company never turns a profit and you don’t sell them to someone who thinks OpenAI eventually will turn a profit, your PPUs are worthless.

Of course, because demand for AI is so hot, and OpenAI is the market leader in generative AI, investors are still willing to invest billions via PPUs, and, as of June 2024, current and former employees can now sell some of their stakes in tender offers. If I were an OpenAI employee, and my “equity” compensation was actually profit share units, and outside investors were willing to buy those profit share units from me for a $100 billion + valuation… I would probably want to sell, no?