Schrödinger's head of macro

A former Greenlight employee sued the hedge fund, alleging it misrepresented his employment history.

One of the funnier underlying bits in “The Office” is Dwight’s insistence on calling himself the “assistant regional manager,” which Michael always changes to “assistant to the regional manager.” A storyline that I wish the showrunners had pursued would've been Dwight suing Michael over his job title.

Lucky for us, we are in the midst of a real-life version of this plot — but in the hedge-fund community.

Last week, James Fishback, who worked at David Einhorn’s Greenlight Capital, tweeted that he'd been invited to debate his former boss on the topic of Tesla. Einhorn, who's tweeted only once in the past year, felt this was worth a reply:

Thank you for the offer. Normally, I am happy to debate and exchange views. However, in order for such a debate to be meaningful, the person on the other side needs to have some knowledge about the subject. In this case, I am not aware that you have ever spent any time analyzing…

— David Einhorn (@davidein) May 16, 2024

In response, Fishback shared a link to a defamation suit against his former employer for claiming that Fishback was never Greenlight’s “head of macro” and instead was employed as a “research analyst.” Some quotes from Mr. Fishback’s suit, which was filed in October 2023 (emphasis added):

As set forth below, Mr. Fishback was previously employed by Greenlight, beginning as a research analyst, then as a trader, and finally as its Head of Macro. Mr. Fishback excelled in his work, and generated over $100 million in profits for Greenlight from the period of February 2021 to August 2023, when Mr. Fishback resigned. Upon his resignation, Greenlight began falsely claiming, for the first time, that Mr. Fishback was never Head of Macro.

In an email dated September 28, 2023, [COO Daniel] Roitman advised Mr. Fishback that he had received an inquiry about Mr. Fishback’s work for Greenlight, and that one of the questions asked was “What were James’ responsibilities as Greenlight’s Head of Macro?” Roitman claimed that Mr. Fishback was never Head of Macro, and threatened to “have a lawyer send [Mr. Fishback] a cease and desist.” Mr. Fishback responded that he would “not be compelled to lie” and “will not comply with your unjust demand.” ... Roitman told this individual that Mr. Fishback was a “Research Analyst” and “was not Head of Macro.” These statements were false, and Greenlight knew them to be false because, as discussed above, Mr. Fishback was, in fact, Head of Macro, and, as established above, Greenlight acknowledged this fact to others in writing. Greenlight’s defamation of Mr. Fishback has caused him to suffer significant damage. For example, by being denied his true title and implicitly smeared as a liar by Greenlight, Mr. Fishback has struggled to secure investors for his new hedge fund, Azoria Partners.

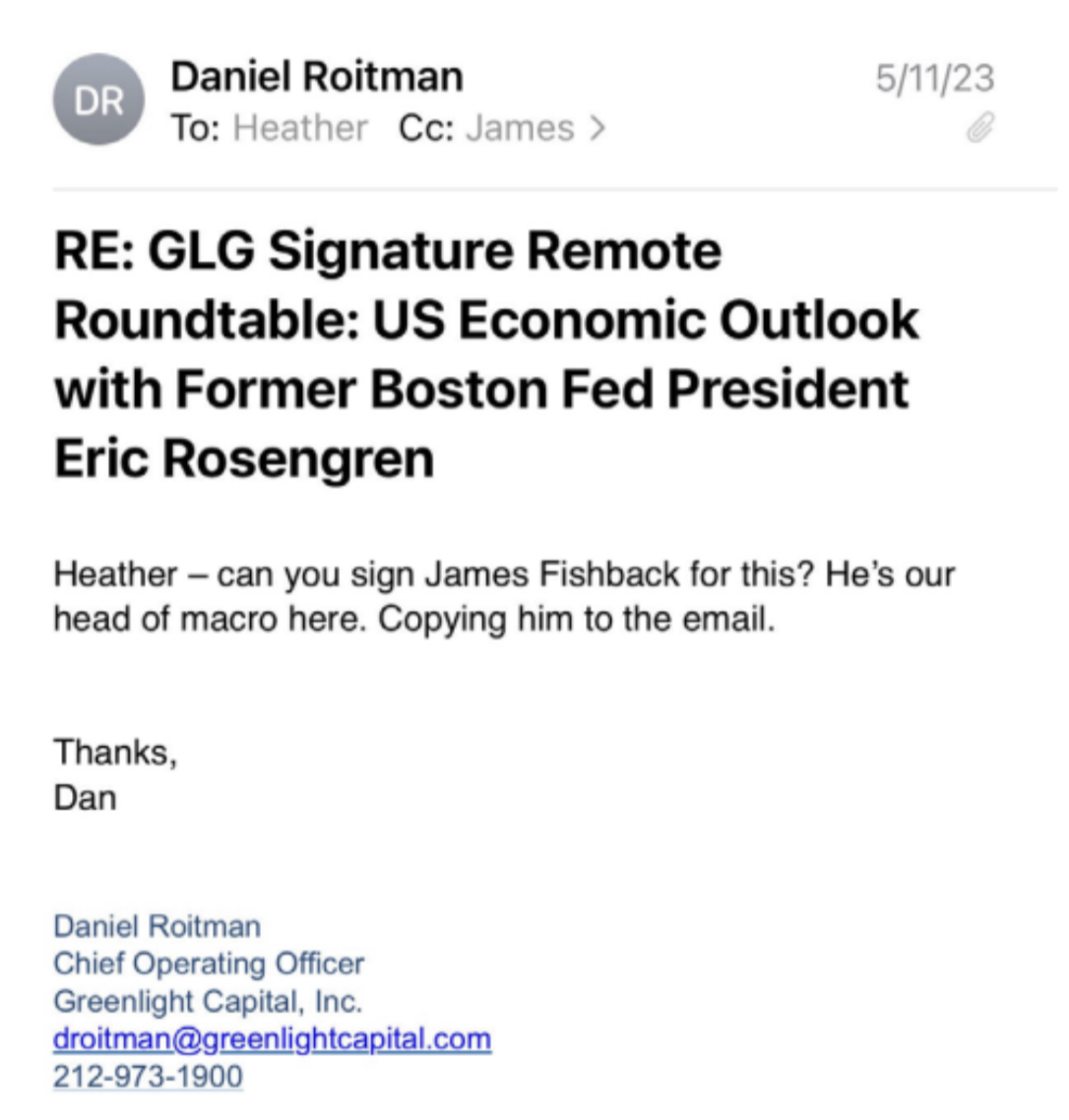

Included in his evidence was an email to financial services firm GLG in which Roitman referred to Fishman as “our head of macro.”

At first glance, I thought, “How does a disagreement over a title lead to litigation?” Yes, Greenlight probably doesn’t want a former employee profiting from misrepresenting himself, and, yes, I’m sure Fishback would be annoyed if this disagreement hindered his fundraising efforts. But a lawsuit over “head of macro”? Really?

But then again… Greenlight said it did have its "best year" in its macro portfolio in 2022, during Fishback’s tenure. In a world of scoreboards with big numbers and even bigger egos, who gets credit for this success matters. A former sales trader who covered Fishback during his time at Greenlight told Sherwood they could attest to the size and scope of the trades he had on while at the firm, as well as his increasing autonomy toward the end of his stint there.

Unless we can clearly see Fishback’s disaggregated performance during this time, the title may be the only other tell. “David needs to publicly release my detailed track record from Greenlight,” Fishback said. “It’s time for me to move on and launch my fund.”

In two letters sent to Fishback by Greenlight’s lawyers in October, they demanded he “cease and desist” from referring to himself as “head of macro.” Oftentimes, the use of that phrase is a prelude to a lawsuit. But when Greenlight sued Fishback in March 2024, the suit wasn’t about the job title. It was about money. But… it’s not not about the job title, either.

Greenlight’s complaint alleges that Fishback had borrowed $337,346.12 plus interest through two different promissory notes, with repayment due immediately if he left the firm. After resigning, on August 15, Fishback received forbearance from Greenlight on these notes. That is, Greenlight said it would delay from collecting what it was owed now until the notes’ maturity dates, as long as certain conditions were met. One of those? That Fishback would not represent himself “as anything other than a former Research Analyst at Greenlight Capital.”

The lawsuit Greenlight filed against Fishback says:

Greenlight received information suggesting that Defendant had falsely represented himself as having held certain titles during his employment with Greenlight other than “Research Analyst,” including but not limited to “Head of Macro,” ... to market himself and a hedge fund that he had founded, Azoria Partners, to potential investors. Greenlight understood that Defendant was using the “Head of Macro” title to wrongfully appropriate Greenlight’s track record and success in making investments informed by macroeconomic events (referred to as “macro” investing or trading). These representations were false because the purported “Head of Macro” title has never existed at Greenlight, and had not been given to Defendant.

Before this suit, but after judging that Fishback had violated the forbearance terms, Greenlight had sent a letter to Fishback on October 11, 2023. Their demands, in order:

“cease and desist” from referring to himself as anything other than a “Research Analyst.”

payment of the money owed

destroy any confidential information

On October 19, 2023, Greenlight sent a second letter echoing these statements. It was four days after receiving this second demand letter that Fishback filed his defamation suit.

TL;DR: James Fishback, a former Greenlight Capital employee who was accused of owing the hedge fund hundreds of thousands of dollars, filed a defamation suit against Greenlight in connection with hindering fundraising efforts for his new hedge fund by saying, in a reference check, that Fishback had never been the “head of macro” and instead was a “research analyst.” Meanwhile, among other things, Greenlight is suing Fishback in connection with a six-figure loan.

But taking a step back, what are we really doing here? If your chief complaint in your lawsuit is that your former employer’s refusal to call you “head of macro” is hindering your fundraising efforts, do you really think that hashing out your grievances on the X timeline will instill more confidence in potential investors?

On the other side, the current employees at a $2 billion hedge fund can’t feel great about seeing their employer sue a former employee over what amounts to a rounding error when it comes to top hedge-fund comp and job-title semantics.

I don’t know. It feels, like, regardless of the legal outcomes, the winner will have a Pyrrhic victory.

Representatives for Greenlight declined to comment.