Air taxi Blade is actually an organ transport business in disguise

How the helicopter fleet quietly became America's biggest airborne ambulance.

Every Manhattan resident flying into JFK has considered booking a Blade helicopter flight back to the city. After five hours on a red-eye from LAX, nothing sounds worse than spending an hour and a half in a $120 Uber, especially when a $195 helicopter can get you there in minutes.

While most of us, myself included, usually stick with Uber, Blade’s business of eliminating inconvenience has proved to be lucrative: the air-transit company made $225M in revenue in 2023 — up more than 580% since 2019.

But you may be surprised to learn that only $99M, or 44%, of that revenue came from carrying passengers through the sky. The other 56% stems from transporting hearts, livers, and lungs around the country. Today, Blade is the largest dedicated air transporter of human organs in the US. Blade’s brand might be a first-class transportation solution, but its business is an ambulance in disguise.

Blade never intended to make its name in the organ-transplant business.

In 2014, Rob Wiesenthal, an investment banker turned media exec who at the time was Warner Music Group’s COO, started Blade with a simple goal: “to figure out how to fly to the Hamptons without working for a hedge fund.” For $575, Blade offered those who dreaded the idea of three hours on the Long Island Rail Road a 35-minute flight out east.

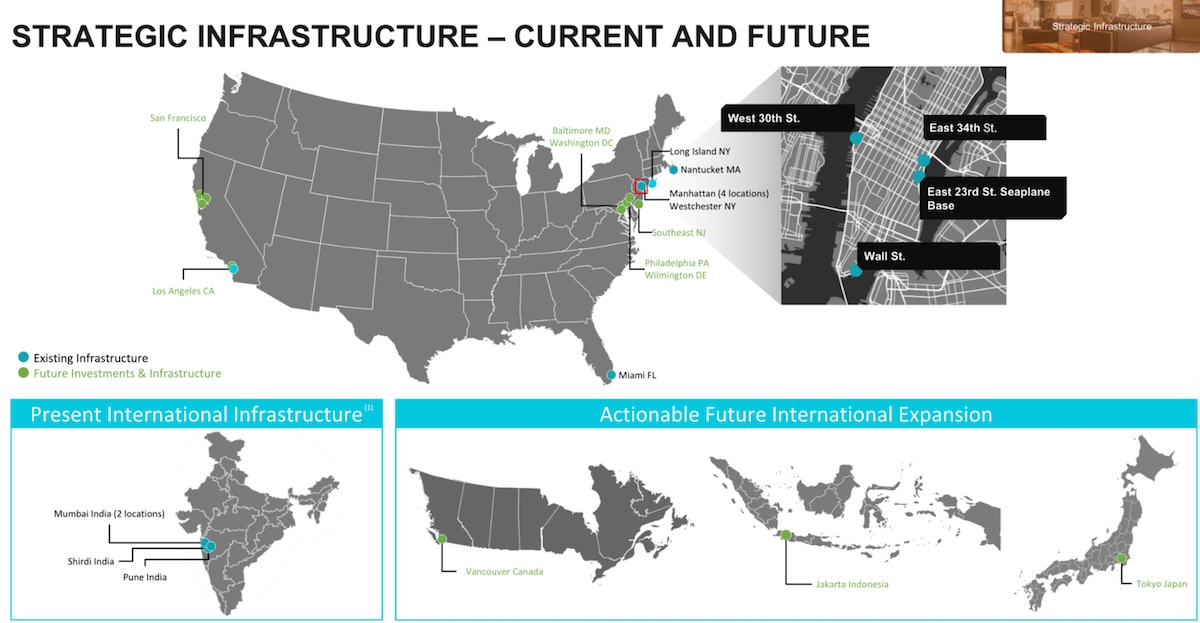

Five years later, in March 2019, Blade launched its JFK-to-Manhattan service, offering flights between 7 a.m. and 7 p.m. every weekday to and from its helipad near Hudson Yards. It kept expanding, opening new markets in LA and Mumbai, as well as a pilot program in San Francisco and chartered flights from New York to Miami.

Then, on December 15, 2020, Blade announced it was going public through a reverse merger with Experience Investment Corp., a special purpose acquisition company, giving the public its first look at the company’s ambitious plans.

Blade’s investor deck revealed plans to expand in the broader Northeast corridor from New York to Boston, Philadelphia, and DC, as well as Northern and Southern California, Vancouver, Jakarta, and Tokyo.

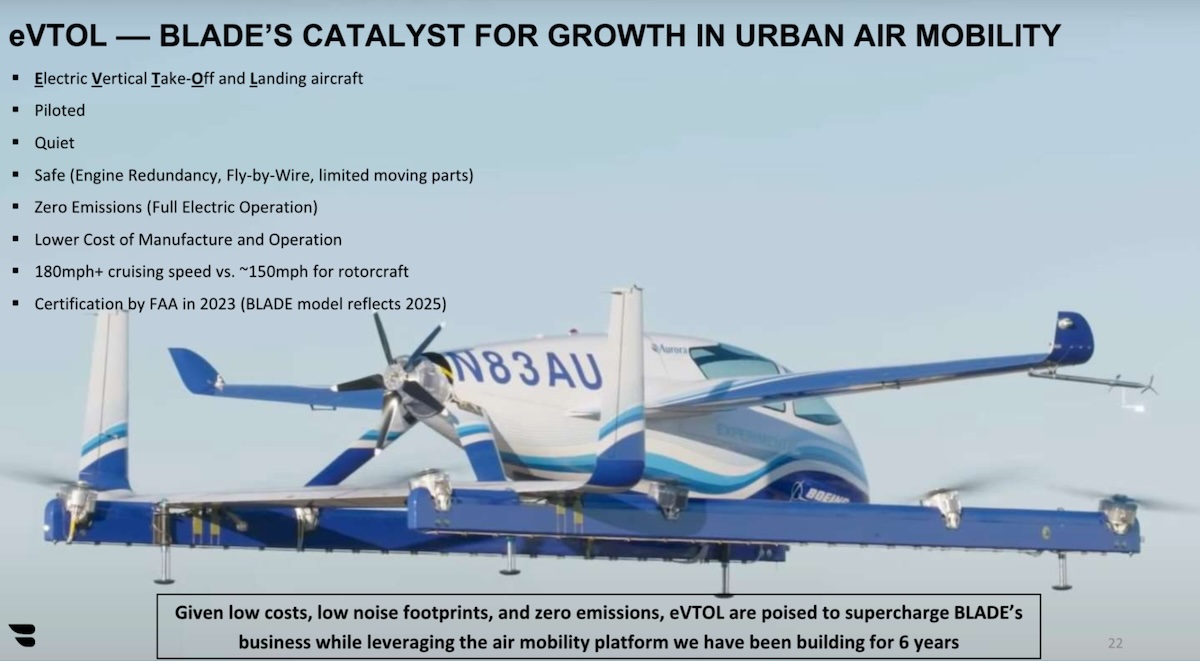

Blade’s catalyst for growth across these markets? The widespread adoption of electric vertical takeoff and landing aircraft, or eVTOLs.

“eVTOL” was mentioned 33 times in Blade’s December 2020 investor deck, and the company believed these new vehicles would address three problems facing Blade’s fleet: emissions, safety, and noise pollution.

Noise pollution has long been a point of contention between cities and helicopter operators. In 2016, for example, Stop the Chop NY/NJ and other advocates negotiated with New York to reduce the number of annual tourist flights allowed from the downtown Manhattan Heliport from 60,000 to 30,000. And, according to Bloomberg, complaints about helicopter noise in NYC soared from 3,332 in 2019 to 22,800 in 2022 (through the first 11 months of the year). Increased nonessential helicopter traffic would also increase friction with cities’ residents, but eVTOLs provided a solution.

Blade, at the time, paid aircraft operators for airtime, but didn’t own any vehicles itself. The transit company’s rationale for an asset-light model was that, besides keeping cost down, it would help Blade more quickly transition to an eVTOL-based fleet once these new vehicles were approved for commercial use.

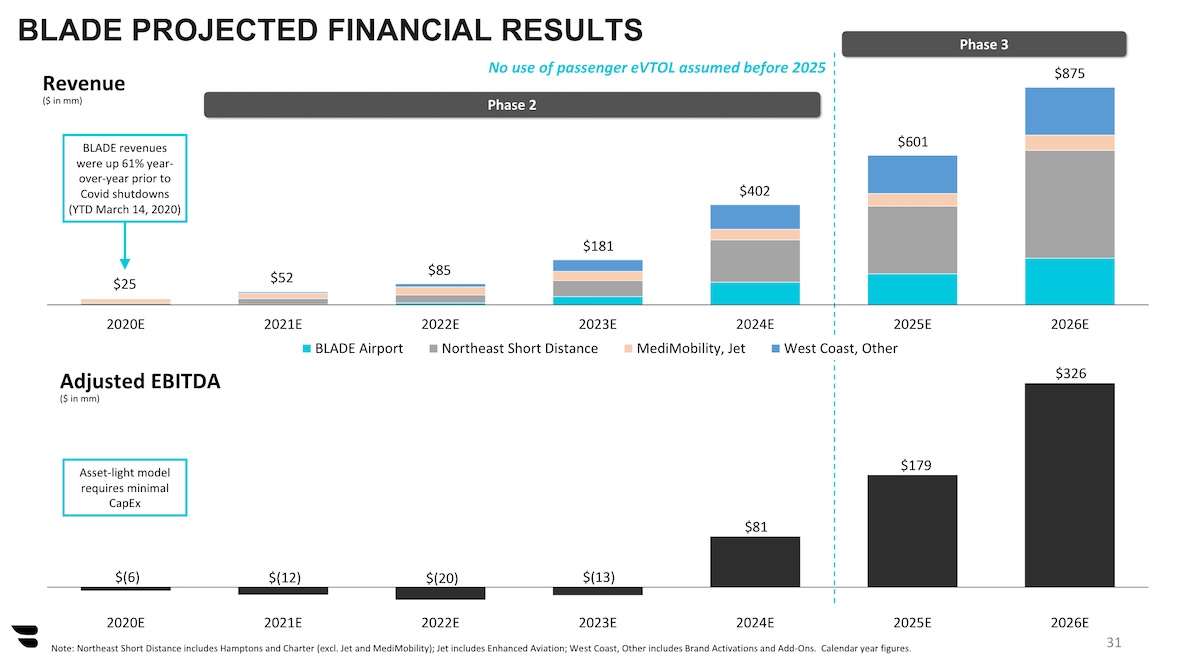

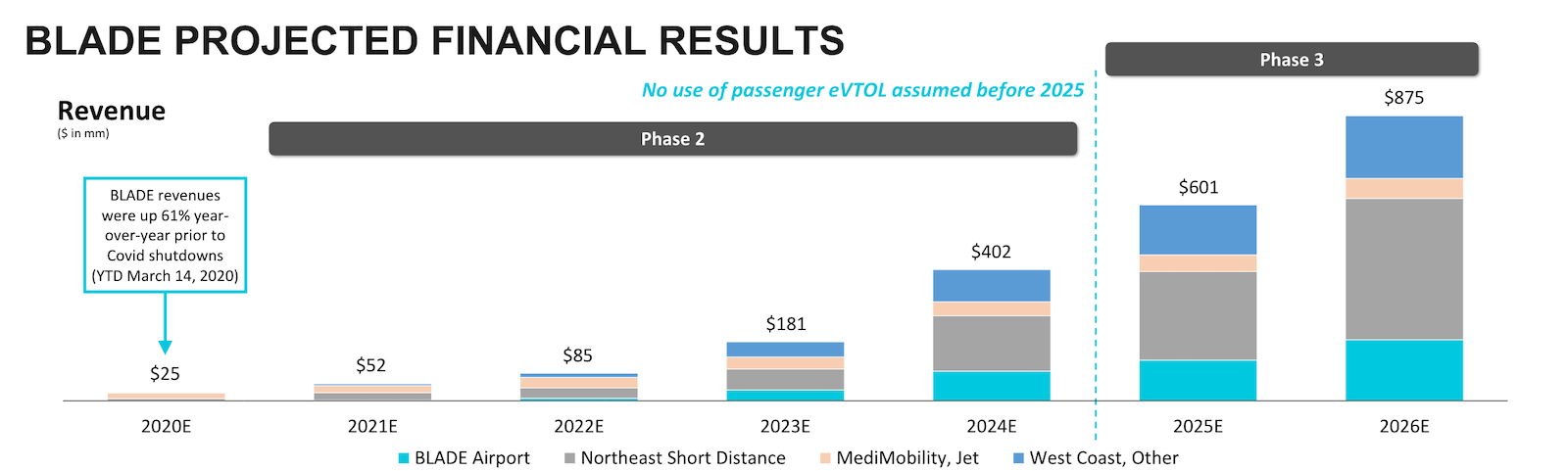

By Blade’s own projections, the company would begin phasing in eVTOLs for short-distance travel in 2025, and for longer flights, such as NYC to DC, in 2026. The company also predicted that by 2026, almost all its projected $875M of revenue would come from a combination of airport shuttles, Northeast short-distance flights, and West Coast and other expansion markets.

In the 17 months after Blade’s reverse-merger announcement, the company executed on its international growth strategy. In December 2021, it entered the Vancouver market by acquiring Helijet, and in May 2022 it acquired three urban air-mobility operators in Europe: Monacair SAM, Héli Sécurité, and another unnamed operator in the south of France.

In discussing the acquisition, Blade’s president, Melissa Tomkiel, said: “Blade continues to cement its position as the world’s leader in urban air mobility with the addition of these routes in Southern France, Monaco, Italy and Switzerland, which, given the geography, short distances and large addressable markets serve as the perfect first-use cases for quiet and emission-free EVA (electric vertical aircraft).”

Will Heyburn, the company’s CFO, added: “These acquisitions should contribute free cash flow on day one, accelerating our timeline to profitability while generating a great return on investment today that will only be enhanced by the future introduction of Electric Vertical Aircraft.”

There was one problem: EVA adoption was slower than anticipated.

In 2022, Lilium and Joby Aviation, two leading EVA startups, delayed their projections for certification and commercial service launch, respectively, from 2024 to 2025. In 2023, startups Volocopter and Vertical Aerospace, as well as legacy jet manufacturer Airbus, suffered similar setbacks with their EVA timelines.

Delayed EVA adoption affected Blade, with the transportation company taking a $20M impairment charge on its European acquisitions. From Blade’s 2023 10-K:

“During the year ended December 31, 2023, the Company recognized an impairment charge for the exclusive rights to air transportation services associated with the acquisition of Blade Europe in the amount of $20,753, which was included in intangible impairment expense within general and administrative expenses in the consolidated statements of operations and is part of the Passenger segment. The impairment was a result of adjustments made to the near term projections for revenue, expenses and expected EVA introduction, to reflect our experience operating Blade Europe since September 2022 as well as expected delays in the commercialization of EVA.”

EVAs were supposed to be Blade’s safer, quieter, cleaner helicopter replacements that fueled the company’s growth, and they were falling behind schedule. Fortunately, the organ-transport business made for an excellent contingency plan.

Blade launched its organ-transportation business, MediMobility, in August 2019, when it partnered with NYU Langone and other hospitals up to 400 miles from NYC to help facilitate organ transportation.

16 months later, MediMobility was still an ancillary business. Blade’s 2020 investor deck mentioned MediMobility only eight times, compared to 33 eVTOL references. And MediMobility’s revenues, which Blade didn’t separate from jet charters, were projected to be the company’s smallest revenue stream.

But everything changed after Blade acquired Trinity Air Medical, a multimodal organ logistics and transportation company, in September 2021. The pandemic had wreaked havoc on Blade’s passenger-transit business, with the company’s YTD revenue through October 2020 dropping 31% from the year before, despite increasing 61% year over year through mid-March. MediMobility, on the other hand, suffered no setbacks from Covid-19.

Excluding the pandemic, Blade’s core business also faced a seasonality problem: as noted in its 2023 investor presentation, Blade’s passenger revenue and flight margins peaked in summer months. MediMobility demand doesn’t fluctuate with the weather.

MediMobility created an excellent hedge for Blade’s passenger business. The Trinity acquisition made sense for both businesses. Trinity already had partnerships with transplant centers in 16 states, but it relied on ambulances for final transport to and from hospitals. Blade’s helicopter network would immediately accelerate delivery times. Discussing the acquisition, Blade’s CEO, Rob Wiesenthal said: “Trinity’s end-to-end services integrate air missions with ground transport. Given the existence of landing pads at most hospitals today, we have the ability to immediately replace Trinity’s ambulances with helicopters on certain hospital-to-hospital missions.”

Doubling down on organ transport had a secondary benefit: it provided a lower-risk opportunity for EVA introduction. In response to the Trinity acquisition, Wisenthal told Vertical Magazine, “There’s so many things we don’t know about how pilots and passengers are going to react to EVA.” As with self-driving cars, consumers are initially apprehensive about trying nascent technology. Blade can now test EVAs within its organ-transportation business before passengers ever set foot on the new aircraft.

MediMobility also faces less regulatory pressure from cities than Blade’s passenger business. Last week, Melissa Elstein, the board chair of Stop the Chop NY/NJ, rallied with others at New York’s City Hall before a hearing about legislation that would limit nonessential, fossil-fuel based chopper flights in Manhattan. Further EVA delays could threaten Blade’s passenger business if officials passed new legislation, but organ transportation would be protected as “essential” travel.

Since acquiring Trinity in 2021, Blade’s organ-transportation business has exploded from $2.2M in 3Q21 revenue to $32M in 4Q23 revenue. In that time, MediMobility expanded from 11.1% of Blade’s total revenue to 67.4%.

Blade’s organ-transplant business is also growing much faster than the rest of the business: MediMobility revenue increased by 48% year over year in 4Q23, versus a 14% increase in short-distance passenger flights and a 32% decline in jet/other revenue.

Blade says it is now the largest dedicated air transporter of human organs in America, and that it transports the majority of hearts, livers, and lungs, as these organs’ short survival windows outside the human body often require air travel. Last year, Blade broke the record for the farthest a human heart has traveled for a transplant: 2,506 miles from Juneau, Alaska to Boston.

In total, Blade delivered about 8,000 organs in 2022, according to CFO Will Heyburn, compared to a total 42,887 organ transplants, and 16,331 heart, liver, and lung transplants, specifically, nationwide that year.

And this year Blade made a notable pivot from its asset-light model, purchasing eight Hawker 800 jets dedicated to medical flights, in a move that Wiesenthal said would “provide us with fixed cost leverage.”

Blade declined to comment to Sherwood as it is in a pre-earnings quiet period.

If you visit Blade’s website, you’ll see options to charter helicopters around British Columbia and images of eVTOLs that the company hopes to fly customers around the world’s busiest cities, but if you review Blade’s earnings reports, you’ll see that it is no longer a luxury transportation company. It’s an ambulance in disguise. And that’s not a bad thing.